ARLINGTON, Va., May 6, 2009 - Interstate Hotels & Resorts

(OTC Bulletin Board: IHRI), a leading hotel real estate investor and the

nation's largest independent hotel management company, today reported operating

results for the first quarter ended March 31, 2009. The company's

performance for the first quarter includes the following (in millions,

except per share amounts):

First Quarter

2009(4) 2008(5)

------------- -------------

Total revenue(1)

$30.5 $38.9

Net loss

$(12.5) $(0.3)

Diluted loss per share

$(0.39) $(0.01)

Adjusted EBITDA(2)(3)

$5.9 $7.7

Adjusted net loss (2)

$(2.0) $(1.1)

Adjusted diluted EPS (2)

$(0.06) $(0.03)

(1) Total revenue excludes other revenue from managed

properties

(reimbursable costs).

(2) Adjusted EBITDA, Adjusted net loss and Adjusted

diluted EPS are non-

GAAP financial measures

and should not be considered as an alternative

to any measures of operating

results under GAAP. See the definition

and further discussion of

non-GAAP financial measures and

reconciliation to net loss

later in this press release.

(3) Includes the company's share of adjusted EBITDA

from investments in

unconsolidated entities

in the amounts of $1.2 million and $1.6

million in the first quarter

of 2009 and 2008, respectively.

(4) The first quarter 2009 results include a $0.8

million charge for

restructuring primarily

related to severance costs as a part of the

company's 2009 cost reduction

program, and $8.9 million of tax expense

relating to the company's

global tax planning strategy. These charges

are excluded from the calculation

of Adjusted EBITDA, Adjusted net

loss and Adjusted diluted

EPS.

(5) The first quarter 2008 results include (i) a

$2.4 million gain on the

sale of the Doral Tesoro

Hotel & Golf Club, and (ii) $1.1 million of

write-offs of intangible

assets related to the sale of certain hotels

in 2008. Each of these

items has been excluded from the calculation

of Adjusted EBITDA, Adjusted

net loss and Adjusted diluted EPS.

"The first quarter was an extremely difficult operating period, a trend

that we anticipate will continue through most of 2009, and possibly into

2010," said Thomas F. Hewitt, chief executive officer. "While our visibility

remains limited, we expect to see the decline in RevPAR begin to moderate

in the second half of the year."

Hotel Management

Same-store(6) RevPAR for all managed hotels in the first quarter declined

19.1 percent to $74.25. Average daily rate (ADR) was $123.01, down 9.8

percent, and occupancy fell 10.3 percent to 60.4 percent.

Same-store RevPAR for all full-service managed hotels declined 19.7

percent to $84.94. ADR was off 9.9 percent to $134.57, while occupancy

decreased 10.9 percent to 63.1 percent.

Same-store RevPAR for all select-service managed hotels declined 17.2

percent to $54.01, led by a 9.2 percent decline in occupancy to 55.1 percent

and an 8.9 percent drop in ADR to $97.98.

"The severe condition of the economy continues to present challenges

to the hotel industry," Hewitt said. "However, we remain focused on optimizing

returns for our owners and shareholders. As lodging demand weakened in

the first quarter, we adapted our cost reduction programs to make every

effort to optimize our owners' and shareholders' returns.

"In addition to the cost reduction plans at the property level, we implemented

an extensive corporate cost savings program in January, which resulted

in a decrease of $4.6 million in corporate G&A expense in the first

quarter, a reduction of 29 percent from last year.

"Our portfolio count remained steady in the 2009 first quarter," Hewitt

added. "We continue to focus on growing our managed portfolio and have

several properties scheduled to come on line in the second quarter. We

also have reached out to lenders and loan servicers to offer our expertise

in taking over distressed assets. There has not been much movement in this

area to date, but we expect activity to pick up later this year and next

year, and we are well positioned to respond quickly when opportunities

arise."

.

.

.

Wholly Owned Hotel Results

EBITDA from the company's seven owned hotels was $4.5 million in the

2009 first quarter as outlined below (in millions):

Owned Hotels

First Quarter

2009 2008

---- ----

Net income (loss)

$(1.3) $0.1

Interest expense, net

$2.9 $3.6

Depreciation and amortization.

$2.9 $3.2

---- ----

EBITDA

$4.5 $6.9

==== ====

"RevPAR for the owned portfolio decreased 16.0 percent, stemming from

an 8.7 percent slide in occupancy and an 8.1 percent decrease in rate,"

Hewitt said. "Our newly renovated Sheraton Columbia (Md.) hotel performed

exceptionally well during the quarter with a 5.2 percent RevPAR increase

over last year.

"Our newly renovated Westin Atlanta Airport hotel performed well compared

to its competitive set and the overall industry with a RevPAR decline of

13.1 percent. Both of these properties have received an overwhelmingly

positive response from customers that are now returning to the hotels following

their comprehensive renovations.

"We saw significant weakness in Arlington, Texas, and Concord, Calif.,

as our hotels in those markets suffered RevPAR declines in excess of our

portfolio average due to local market conditions. While total revenue for

our owned hotels decreased $4.9 million, we were able to control expenses,

leading to an overall expense reduction of $2.4 million."

Balance Sheet

On March 31, 2009, Interstate had:

-- Total unrestricted cash of $13.0 million.

-- Total debt of $244.0 million, consisting of $161.5 million

of senior debt and $82.5 million of non-recourse mortgage debt.

"We have engaged Bank of America to be the lead arranger for the extension

of our credit facility, which has a March 2010 maturity," said Bruce Riggins,

chief financial officer. "We continue to have productive discussions with

our bank group regarding this extension, and our goal is to have this extension

in place by June 30.

"In late March, we received a waiver from our bank group related to

our potential NYSE delisting, pending an appeal process with the Exchange,"

said Riggins. "As part of the waiver agreement, the facility size was permanently

reduced to $173.3 million from $198.0 million and the interest rate was

increased to LIBOR plus 350 basis points from LIBOR plus 275 basis points.

The new facility size provides for $10 million of borrowing capacity, of

which $6 million is available through June 30. We do not expect that we

will need to draw on our revolving facility during the waiver period."

Outlook and Guidance

The company has updated its 2009 guidance to reflect a RevPAR decline

scenario of 17 percent for all managed properties and 14 percent for owned

hotels:

-- Total Adjusted EBITDA of $37 million which includes the following:

-- EBITDA from wholly owned hotels of $19 million;

-- The company's share of EBITDA from unconsolidated joint ventures

of $6 million; and

-- EBITDA from the hotel management business of $12 million.

-- Adjusted net loss of $(1.9) million or $(0.06) per share.

Interstate Hotels & Resorts, Inc.

Consolidated Statements of Operations

(Unaudited, in thousands except per share amounts)

Three Months Ended

March 31,

-------------------

2009 2008

---- ----

Revenue:

Lodging

$19,036 $23,918

Management fees

8,351 9,909

Termination fees (1)

1,246 3,010

Other

1,884 2,099

----- -----

30,517 38,936

Other revenue from managed properties

132,089 151,014

------- -------

Total

revenue

162,606 189,950

Expenses:

Lodging

14,582 17,025

Administrative and general

11,238 15,829

Depreciation and amortization

3,841 4,274

Restructuring costs (2)

831 -

Asset impairments and write-offs

(3)

- 1,112

--- -----

30,492 38,240

Other expenses from managed properties

132,089 151,014

------- -------

Total

operating expenses

162,581 189,254

------- -------

OPERATING INCOME

25 696

Interest income

100 319

Interest expense (4)

(2,907) (3,815)

Equity in (losses) earnings of

unconsolidated entities (5)(6)

(798) 2,361

Gain on sale of investments

13 -

-- -

LOSS BEFORE INCOME TAXES

(3,567) (439)

Income tax (expense) benefit (7)

(8,916) 151

------ ---

NET LOSS

(12,483) (288)

Add: Net loss attributable to noncontrolling

interest

6 2

- -

NET LOSS ATTRIBUTABLE TO INTERSTATE

STOCKHOLDERS

$(12,477) $(286)

======== =====

Basic and diluted loss per share

attributable to Interstate stockholders

$(0.39) $(0.01)

====== ======

Weighted-average basic and diluted shares

outstanding (in thousands)(8)

31,925 31,714

====== ======

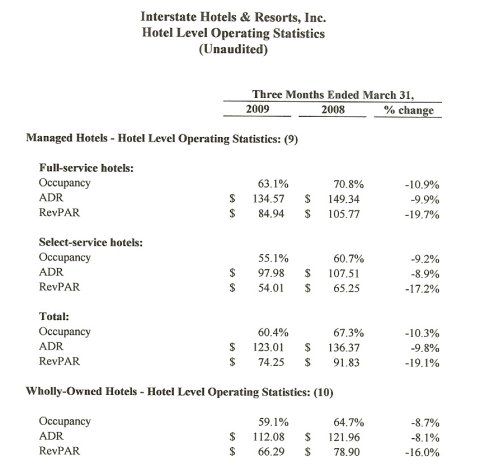

Interstate Hotels & Resorts, Inc.

Hotel Level Operating Statistics

(Unaudited)

Three Months Ended March

31,

-------------------------

2009 2008 % change

---- ---- --------

Managed Hotels - Hotel Level Operating Statistics:

(9)

Full-service hotels:

Occupancy

63.1% 70.8% -10.9%

ADR

$134.57 $149.34 -9.9%

RevPAR

$84.94 $105.77 -19.7%

Select-service hotels:

Occupancy

55.1% 60.7% -9.2%

ADR

$97.98 $107.51 -8.9%

RevPAR

$54.01 $65.25 -17.2%

Total:

Occupancy

60.4% 67.3% -10.3%

ADR

$123.01 $136.37 -9.8%

RevPAR

$74.25 $91.83 -19.1%

Wholly-Owned Hotels - Hotel Level Operating

Statistics: (10)

Occupancy

59.1% 64.7% -8.7%

ADR

$112.08 $121.96 -8.1%

RevPAR

$66.29 $78.90 -16.0%

Interstate Hotels & Resorts, Inc.

Reconciliations of Non-GAAP Financial Measures (11)

(Unaudited, in thousands except per share amounts)

Three Months Ended

March 31,

-------------

2009 2008

---- ----

Net loss

$(12,483) $(288)

Adjustments:

Depreciation and amortization

3,841 4,274

Interest expense, net

2,807 3,496

Depreciation and amortization

from unconsolidated

entities

952 701

Interest expense, net from unconsolidated

entities

962 963

Income tax benefit

8,916 (151)

----- ----

EBITDA

4,995 8,995

Restructuring costs (2)

831 -

Asset impairments and write-offs

(3)

- 1,112

Gain on sale of investments

(13) -

Equity interest in the sale

of unconsolidated

entities (5)

- (2,392)

Foreign currency loss from unconsolidated

entities (6)

129 -

------ ------

Adjusted EBITDA

$5,942 $7,715

====== ======

Three Months Ended

March 31,

-------------

2009 2008

---- ----

Net loss

$(12,483) $(288)

Adjustments:

Restructuring costs (2)

831 -

Asset impairments and write-offs

(3)

- 1,112

Gain on sale of investments

(13) -

Deferred financing costs write-off

(4)

119 -

Equity interest in the sale

of unconsolidated

entities (5)

- (2,392)

Foreign currency loss from unconsolidated

entities (6)

129 -

Income tax rate adjustment (7)(12)

9,466 442

----- ---

Adjusted net loss

$(1,951) $(1,126)

======= =======

Adjusted diluted loss per share

$(0.06) $(0.03)

====== ======

Weighted average number of diluted shares

outstanding (in thousands) (8):

31,925 31,714

Interstate Hotels & Resorts, Inc.

Outlook Reconciliation (11)

(Unaudited, in

thousands)

Forecast

----------

Year Ending

December 31, 2009

-------------------

Net loss

$(9,200)

Adjustments:

Depreciation and amortization

17,000

Interest expense, net

14,100

Depreciation and amortization

from

unconsolidated entities

4,300

Interest expense, net from unconsolidated

entities

4,100

Income tax expense

5,700

-----

EBITDA

36,000

Restructuring costs (2)

800

Gain on sale of investments

-

Deferred financing costs write-off

(4)

100

Foreign currency loss from unconsolidated

entities (6)

100

---

Adjusted EBITDA

$37,000

=======

Forecast

----------

Year Ending

December 31, 2009

-------------------

Net Loss

$(9,200)

Adjustments:

Restructuring costs (2)

800

Gain on sale of investments

-

Deferred financing costs write-off

(4)

100

Foreign currency loss from unconsolidated

entities (6)

100

Income tax rate adjustment (7)(12)

6,300

-----

Adjusted Net Loss

$(1,900)

=======

Adjusted diluted loss per share (8)

$(0.06)

======

Interstate Hotels & Resorts, Inc.

Notes to Financial Tables

(Unaudited)

(1) We record termination fees as revenue

when all contingencies related

to the termination

fees have been removed.

(2) In the first quarter of 2009, we recognized

$0.8 million in

restructuring charges,

consisting of severance payments and other

benefits for terminated

employees, associated with our cost-savings

program implemented

in January 2009.

(3) This amount represents losses recorded

for intangible assets

associated with

terminated management contracts and other asset

impairments.

(4) For the first quarter of 2009, interest

expense includes a $0.1

million write-off

of deferred financing costs as a result of the

permanent reduction

in capacity of our credit facility associated

with the waiver

and amendment obtained in March 2009.

(5) In the first quarter of 2008, one of

our joint ventures sold the

Doral Tesoro Hotel

& Golf Club and we recorded a gain of $2.4

million.

(6) One of our international joint ventures

has debt that is denominated

in a currency other

than its functional currency. Each period, the

debt obligation

is translated and the resulting gain or loss is

recognized in our

consolidated statement of operations, although it

is a non-cash event.

(7) In the first quarter of 2009, we created

a foreign subsidiary which

in turn purchased

the rights to license our U.S. parent company's

intellectual property.

This transaction generated U.S. tax expense in

the quarter. This

strategy allows Interstate to shift tax exposure

from foreign subsidiaries

to the U.S. where Interstate can utilize

tax attributes in

the form of net operating loss carryforwards and

tax credits to minimize

our cash taxes paid. The effect of this event

has been excluded

from our adjusted net loss as it is a non-recurring

and non-cash item.

Exclusive of this event, our effective tax rate on

recurring operations

for 2009 is 22.0%.

(8) Our diluted earnings per share assumes

the issuance of common stock

for all potentially

dilutive common stock equivalents outstanding.

Potentially dilutive

shares include unvested restricted stock and

stock options granted

under our comprehensive stock plan and

operating partnership

units held by minority partners. No effect is

shown for any securities

that are anti-dilutive.

(9) We present certain operating statistics

(i.e. occupancy, RevPAR and

ADR) for the periods

included in this report on a same-store hotel

basis. We

define our same-store hotels as those which (i) are

managed or owned

by us for the entirety of the reporting periods

being compared or

have been managed by us for part of the reporting

periods compared

and we have been able to obtain operating statistics

for the period of

time in which we did not manage the hotel, and (ii)

have not sustained

substantial property damage, business

interruption, or

undergone large-scale capital projects during the

current reporting

period being presented. In addition, the operating

results of hotels

for which we no longer managed as of March 31, 2009

are also not included

in same-store hotel results for the periods

presented herein.

Of the 224 properties that we managed as of March

31, 2009, 192 hotels

have been classified as same-store hotels.

RevPAR is defined

as revenue per available room.

(10) Operating statistics for our wholly-owned

hotels includes our entire

portfolio of 7 hotels,

including the Sheraton Columbia and the Westin

Atlanta Airport,

both of which underwent comprehensive renovation

programs throughout

2008.

(11) See discussion of EBITDA, adjusted EBITDA,

adjusted net loss and

adjusted diluted

loss per share, located in the "Non-GAAP Financial

Measures" section,

described earlier in this press release.

(12) This amount represents the effect on income

tax expense for the

adjustments made

to net loss. For the first quarter of 2009 and 2008,

we used the effective

tax rate of 22.0% and 34.5%, respectively. For

2009, the rate excludes

the non-recurring income tax expense

described in footnote

7.

Source: Interstate Hotels & Resorts

CONTACT: Carrie McIntyre, SVP, Treasurer, +1-703-387-3320 |

Earnings Conference Call

Interstate will hold a conference call to discuss its

first-quarter results today, May 6, at 10 a.m. Eastern Time. To hear the

webcast, interested parties may visit the company's Web site at www.ihrco.com

and click on Investor Relations and then First-Quarter Conference Call.

A replay of the conference call will be available until midnight on Wednesday,

May 13, 2009, by dialing (800) 405-2236, reference number 11130289, and

an archived webcast of the conference call will be posted on the company's

Web site through June 6, 2009.

Interstate Hotels & Resorts has ownership interests

in 56 hotels and resorts, including seven wholly owned assets. Together

with these properties, the company and its affiliates manage a total of

224 hospitality properties with more than 45,000 rooms in 37 states, the

District of Columbia, Russia, Mexico, Belgium, Canada and Ireland. Interstate

Hotels & Resorts also has contracts to manage 16 to be built hospitality

properties with approximately 4,000 rooms. For more information about Interstate

Hotels & Resorts, visit the company's Web site: www.ihrco.com.

Non-GAAP Financial Measures

Included in this press release are certain non-GAAP financial

measures, which are measures of our historical or estimated future performance

that are different from measures calculated and presented in accordance

with generally accepted accounting principles in the United States of America

(or GAAP), within the meaning of applicable Securities and Exchange Commission

rules, that we believe are useful to investors. They are as follows: (i)

Earnings before interest, taxes, depreciation and amortization (or "EBITDA")

and (ii) Adjusted EBITDA, Adjusted net loss and Adjusted diluted loss per

share. The following discussion defines these terms and presents the reasons

we believe they are useful measures of our performance.

EBITDA

A significant portion of our non-current assets consists

of intangible assets, related to some of our management contracts, and

long-lived assets, which include the cost of our owned hotels. Intangible

assets, excluding goodwill, are amortized over their expected term. Property

and equipment is depreciated over its useful life. Because amortization

and depreciation are non-cash items, management and many industry investors

believe the presentation of EBITDA is useful. We also exclude depreciation

and amortization and interest expense from our unconsolidated joint ventures.

We believe EBITDA provides useful information to investors regarding our

performance and our capacity to incur and service debt, fund capital expenditures

and expand our business. Management uses EBITDA to evaluate property-level

results and as one measure in determining the value of acquisitions and

dispositions. It is also widely used by management in the annual budget

process. We believe that the rating agencies and a number of lenders use

EBITDA for those purposes and a number of restrictive covenants related

to our indebtedness use measures similar to EBITDA presented herein.

Adjusted EBITDA, Adjusted Net Loss and Adjusted Diluted

EPS

We define Adjusted EBITDA as, EBITDA excluding the effects

of certain recurring and non-recurring charges, transactions and expenses

incurred in connection with events management believes do not provide the

best indication of our ongoing operating performance. These charges include

restructuring and severance expenses, asset impairments and write-offs,

gains and losses on asset dispositions for both consolidated and unconsolidated

investments, and other non-cash charges. We believe that the presentation

of Adjusted EBITDA will provide useful supplemental information to investors

regarding our ongoing operating performance and when combined with the

primary GAAP presentation of net loss, is beneficial to an investor's complete

understanding of our operating performance. We also use Adjusted EBITDA

in determining our incentive compensation for management.

Similarly, we define Adjusted net loss and Adjusted diluted

loss per share ("EPS") as net loss and diluted EPS, without the effects

of those same charges, transactions and expenses described earlier. We

believe that Adjusted EBITDA, Adjusted net loss and Adjusted diluted EPS

are useful performance measures because including these expenses, transactions,

and special charges may either mask or exaggerate trends in our ongoing

operating performance. Furthermore, performance measures that include these

charges may not be indicative of the continuing performance of our underlying

business. Therefore, we present Adjusted EBITDA, Adjusted net loss and

Adjusted diluted EPS because they may help investors to compare our performance

before the effect of various items that do not directly affect our ongoing

operating performance.

Limitations on Use of EBITDA, Adjusted EBITDA, Adjusted

Net Loss and Adjusted Diluted EPS

We calculate EBITDA, Adjusted EBITDA, Adjusted net loss

and Adjusted diluted EPS as we believe they are important measures for

our management's and our investors' understanding of our operations. These

may not be comparable to measures with similar titles as calculated by

other companies. This information should not be considered as an alternative

to net income, operating profit, cash from operations or any other operating

performance measure calculated in accordance with GAAP. Cash receipts and

expenditures from investments, interest expense and other non-cash items

have been and will be incurred and are not reflected in the EBITDA and

Adjusted EBITDA presentations. Adjusted net loss and Adjusted diluted EPS

do not include cash receipts and expenditures related to those same items

and charges discussed above. Management compensates for these limitations

by separately considering these excluded items, all of which should be

considered when evaluating our performance, as well as the usefulness of

our non-GAAP financial measures. Additionally, EBITDA, Adjusted EBITDA,

Adjusted net loss and Adjusted diluted EPS should not be considered a measure

of our liquidity. Adjusted net income and Adjusted diluted EPS should also

not be used as a measure of amounts that accrue directly to our stockholders'

benefit.

This press release contains "forward-looking statements,"

within the meaning of the Private Securities Litigation Reform Act of 1995,

about Interstate Hotels & Resorts, including those statements regarding

future operating results and the timing and composition of revenues, among

others, and statements containing words such as "expects," "believes" or

"will," which indicate that those statements are forward-looking. Except

for historical information, the matters discussed in this press release

are forward-looking statements that are subject to certain risks and uncertainties

that could cause the actual results to differ materially, including the

volatility of the national economy, economic conditions generally and the

hotel and real estate markets specifically, the war in Iraq, international

and geopolitical difficulties or health concerns, governmental actions,

legislative and regulatory changes, availability of debt and equity capital,

interest rates, competition, weather conditions or natural disasters, supply

and demand for lodging facilities in our current and proposed market areas,

and the company's ability to manage integration and growth. Additional

risks are discussed in Interstate Hotels & Resorts' filings with the

Securities and Exchange Commission, including Interstate Hotels & Resorts'

annual report on Form 10-K for the year ended December 31, 2008.

(6) Please see footnote 9 to the financial tables within

this press release for a detailed explanation of "same-store" hotel operating

statistics. |