advertisement

What Hotels, If Any, Will be Able to

Improve Their Profits in 2009?

.

|

News for the Hospitality Executive |

What Hotels, If Any, Will be Able to

Improve Their Profits in 2009?

.

| by: Robert Mandelbaum, June 2009

The outlook for the lodging industry in 2009 is certainly bleak. As of June 2009, PKF Hospitality Research (PKR-HR) is forecasting that the average U.S. hotel will suffer a 37.8 percent decline in net operating income (NOI) from 2008 to 2009. If this projection holds true, it would be the greatest annual decline in unit-level profits observed ever since PKF started tracking hotel performance back in 1937. Despite this gloomy forecast, there will be some hotels that persevere and achieve an increase on the bottom line during the year. To identify those properties that might have the opportunity to increase their profits in 2009, PKF-HR has analyzed 2001 hotel performance information from our Trends® in the Hotel Industry database. Despite an overall average decline in profits of 19.4 percent in 2001, 25.1 percent of the hotels that participated in our survey that year realized an increase in their NOI (�winners�). This is the lowest percentage of this measurement during the last 40 years of our Trends® survey. PKF Trends in the Hotel Industry

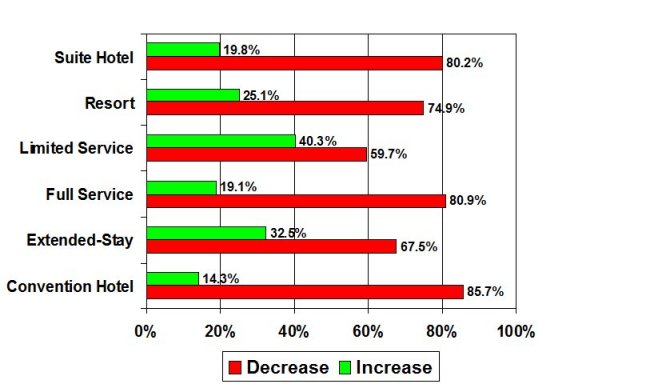

Profile Of The Winners Of all the hotels that achieved profit growth in 2001, nearly half (46.0%) were limited-service properties, followed by full-service hotels (29.2%) and extended-stay properties (12.3%). This is consistent with our analysis of �winners and losers� within each property type category. Among hotel types, the limited-service segment had the greatest percentage (40.3%) of properties that increased their NOI, followed by extended-stay hotels (32.5%). Least able to push the bottom line were convention hotels (14.3%) and all-suite properties (19.8%). It appears that both limited-service and extended-stay hotels benefited from their relatively low rate structures, as well as leaner staffing needs and operating expenses. PKF Trends in the Hotel Industry Sample

from 2000 to 2001 Change from 2000 to 2001

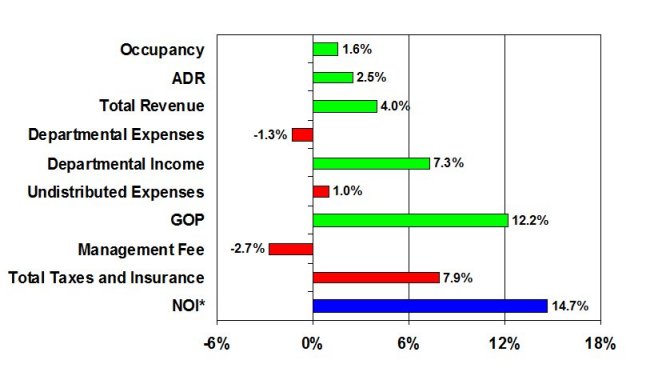

Source: PKF Hospitality Research, Average Size = 164 rooms Hotels located in the South Central region of the nation comprised the largest segment (30.9%) of the properties that were able to increase their profits in 2001, followed by the South Atlantic region (25.2%) and Mountain-Pacific states (23.7%). The average size of the hotels that achieved NOI growth was 164 rooms. Revenue Growth Despite deteriorating market conditions, operators at the hotels that were able to increase their profits in 2001 managed to grow their occupancy and push their room rates. In 2001, the overall Trends® sample experienced a 10.3 percent decline in RevPAR, the result of a 7.4 percent decline in occupancy and a 3.1 percent drop in ADR. Conversely, at the �winning� hotels, occupancy levels increased 1.6 percent while room rates grew 2.5 percent. In addition to rooms revenue, all other revenue sources at these same properties increased as well. For those properties with restaurants, lounges, and meeting space, food and beverage revenue increased 2.3 percent. Other operated revenues improved 4.7 percent, while rental and other income grew 4.2 percent. In aggregate, total hotel revenue at the �winning� properties increased 4.0 percent. Controlling Expenses Management at the hotels that achieved NOI growth in 2001 were able to control their expenses to some degree, but achieved just a minor overall cost reduction of 0.02 percent. This is far less than the 5.2 percent decrease in expenses implemented on average by the entire Trends® sample. With the number of rooms occupied growing by 1.6 percent, the �winning� sample did not benefit from any reductions in the variable expenses associated with serving guests. Further, management was under less pressure to cut costs since their total revenue grew 4.0 percent. In 2001, all hotels were challenged to cut expenses since some of the major fixed costs were rising at levels above their long-term average. For the hotels in the �winning� sample, utility costs increased 8.2 percent, while property taxes grew 6.2 percent and insurance premiums jumped 15.3 percent. To achieve the overall 0.02 percent cut in costs, the �winning� hotel managers made their most meaningful reductions in the operated departments. Expenses in both the rooms and food and beverage departments were reduced 1.4 percent. The operated departments contain the greatest amount of employees, especially at limited-service hotels. Therefore, it appears that hotel management focused on staffing, salaries, and wages to control costs. Among the undistributed departments, administrative and general expenses were reduced by 2.3 percent, while maintenance costs were cut by 1.7 percent. Contrary to the cuts in administration and maintenance, the �winning� hotels made a 2.9 percent investment in sales and marketing. Given the 4.4 percent increase in RevPAR, a large part of the rise in marketing expenditures can be attributed to the corresponding growth in franchise fees. However, there was also a slight increase in the amount spent for other direct sales related activities. Revenue Challenge in 2009 In 2001, the hotels that were able to achieve an increase in NOI did so because of a 4.0 percent increase in revenue, while holding expenses virtually flat. The net result was an average profit growth of 14.7 percent for these �winners.� Given the poor outlook for both occupancy and ADR in all of the 50 markets for which PKF-HR prepares a forecast, it will be an extreme challenge for operators to increase their revenues in 2009. Therefore, it can be assumed that during this industry recession, expense controls will be the key for any hotel hoping to grow their profits. Aiding hotel management in their effort to control costs will be the high rate of unemployment, current low price of oil, and expectations of price deflation for the year. On the other hand, hotel managers will need to keep an eye on the Employee Free Choice Act legislation, which is generally believed to put upward pressure on wage rates. In addition, cash-starved governments and insurance companies will most likely compensate for their financial struggles by raising property taxes and premiums. There will be some �winning� hotels in 2009 that are able to increase

their profits. This will most likely be triggered by some unique

local market conditions or extraordinary circumstances that generate lodging

demand for proximate hotels. However, it is tough to imagine that

one-quarter of the nation�s hotels will be able to improve their profits

in 2009 like we observed in 2001. Given the extreme nature of the

economic and market conditions, a lot of lodging industry records will

be broken in 2009, most for poor performance.

Robert Mandelbaum is the Director of Research Information Services for PKF Hospitality Research. He is located in the firm�s Atlanta office (www.pkfc.com). This article was published in the May 2009 issue of Lodging. |

| Contact:

Robert Mandelbaum

|

|

|