|

News for the Hospitality Executive |

The Role of Hotel Brands in the War of Survival

.

|

By Bryan E. Younge, MAI, ASA May 2009 The Battle

And so the battle continues. While not welcomed by anyone, this invading economic turmoil is an enemy environment that has already dug its trenches and fortified its position�the presence of which everyone is beginning to get used to and planning to be around for a while longer. In the meantime, hotel operators are being forced to fight for scraps of sustenance to survive while at the same time trying to perform reconnaissance on the enemy. Why is it here? What will make it go away? How do we defeat it? Most critically, how do we live with it here in the meantime? Sparing all but one more combat analogy, hotels can in many ways be compared to infantry. In economic downswings, hotels are often at commercial real estate�s front line. They draw first blood; they draw the most blood. But they help lead the way to victory and are among the first to welcome in-person those who travel into the zone to begin the reconstruction process. And when this happens, the wounds seemingly heal rather quickly. For survival while the battle continues, hotels fall back to their affiliations (brands) and use the system to the best of their abilities to take care of one another, and to provide reinforcements and sustenance for one another to maintain strength and resilience through the struggle. These efforts are necessary not only to ward off the enemy, but also to protect against other brands that try to steal or hoard their means of sustenance. Adding to the unstable environment is another force to be reckoned with�good quality non-branded or boutique hotels�which lately have been commanding a greater deal of respect and finding ways to earn their fair share of the scraps. The Branding Cradle

Over the following few decades, the U.S. endured various recessions, struggled through a number of civil movements and elected presidents with wildly differing policies. Further, the wars of the world were becoming a mark of television fascination. So many events in the world had inflicted a relentless sense of insecurity that the importance of developing a brand cradle that nurtured characteristics such as �large� and �safe� in almost any business was high. Responding to these events were real estate visionaries who realized that developing major national or international hotel brands and franchises would be a far more economically feasible way to expand. These brands offered security, familiarity and a sense of assurance for travelers who were otherwise holed up in their affairs. In fact, hotel branding worked so well, that by the 1980s it became the primary vehicle to introduce new hotel concepts and technologies�activities (including launching select-service or extended-stay prototypes) that might never be introduced by way of boutique or non-branded hotels. Today, there is a noticeably wide perception differential between branded and non-branded properties by both investors and hotel guests. Based on a review of various competitive hotel landscapes complied by Cushman & Wakefield, it is clear that the average room rate attainment by branded properties far outstretches non-branded inns that have a similar level of finishes and amenities. While many might argue that the rate premium for branded properties is intended to reflect the higher degree of quality, amenities and/or service, others would contend that it is a lot of smoke and mirrors to justify costly royalty fees. According to Dan Beider, Senior Managing Director and Chairman of Paramount Lodging Advisors in Chicago, Illinois, �The question of branding is as important during these trying economic times as they are during the height of the cycles. Brands in major CBD's are a significant upgrade to upscale, upper upscale and luxury independent hotels in urban markets. While reservation contribution sometimes is a heavily debated topic, particularly in major markets where there is generally strong demand, when looking at an asset as a long term hold, the big question is �what delivers long term, through all seasons and through cycles?� To us, the benefits that major brands offer outweigh the franchise fees and royalties paid to the brands.� So the begging question is, why would any operator or investor roll the dice with a property that did not feature a well-established brand affiliation no matter what the royalty charges were? Defensiveness of Branding

This answer was not so much a surprise as much as it was reinstituting a seemingly overly easy explanation. The answer seems to be simply too obvious. That is, at the middle part of this decade, hotel operating performance was so positive and so swaggering that at some point hotel owners began to question any palatable importance of keeping or installing such an expensive franchise affiliation. An increasing number of hoteliers became more comfortable with the notion that all of this hotel operational rigmarole might be better controlled as a standalone rather than as part of a big franchise gimmick. Highly confident venturists often might be heard muttering, �who needs a brand, anyway?� Based on a review of participating lodging facilities to Smith Travel Research in the Chicago market, the relative percentage increase of rooms that were added to the Chicago inventory between 2003 and 2008 that represented independent hotels, boutique properties or other inns that were not represented by any major flag outpaced the additions of branded rooms. Compared to the entire 1990s decade, these figures were practically flip-flopped. �In most cases,� according to Greg Kennealey, a senior asset manager with Strategic Hotels & Resorts in Chicago, Illinois, �the major hotel brands provide owners with significant advantages versus independent operators, and this is especially true during economic downturns. These organizations have the tremendous sales and marketing resources which help insure that every possible business opportunity is aggressively pursued. In addition, their expense management systems are comprehensive and very responsive to changes in business demand. This enables owners to aggressively cut costs in a declining market to preserve profit margins.� In a telephone interview with Phil Baxter, Partner at Palmer Hospitality Group in Beverly Hills, California, the non-branded hotels were particularly vulnerable in economic downswings. Mr. Baxter indicated that in larger, established markets such as San Francisco, five-star branded hotels are able to capture travelers that normally would stay at a four-star flag at a similar room rate. Four-star properties then turn to siphon demand from the upscale boutique properties, but the boutique or non-branded upscale hotels often do not have anywhere to go. These properties are believed to have fewer options or endure more difficulty replenishing their base patrons. Mr. Baxter also commented that business travelers, when urged to squeeze travel budgets, commonly would allow for comfort concessions (albeit not significant) to maintain the inflow points in a top brand�s awards program, such as making a downshift in the tier of a generally-preferred property type or select a less expensive hotel that is further from a city�s epicenter. It was almost always considered an advantage for a hotel to be proximate to the area�s primary convention center. Overall, there is �less operational risk� for a property under the umbrella of a major brand than a hotel going solo. As discussed so far, it seems evident that most individuals that intimately understand the mechanics of hotel operations and transactions would place their bets on brands. Okay, point taken. But we are in tough economic times, and for operators of non-branded hotels it certainly is a simple reason and excuse to blame any loss of market share on the lack of a major flag. Not so fast� Branding Resilience: A Statistical Approach

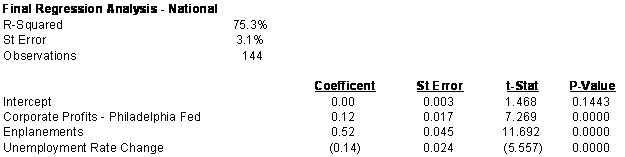

The regression analysis performed focused on RevPAR year-over-year growth and attempted to understand what the coincident and leading economic indicators were that could assist in explaining the RevPAR performance for the national hotel industry. The historical period evaluated was from January 1997 through December 2008, a period of twelve years using monthly data inputs. An array of regression periods, potential economic indicators, and differing monthly lead times were regressed against national RevPAR year-over-year growth to determine the best individual indicators. A summary of the regressions run for each individual indicator is shown below.

Using the above data helped to narrow down the combinations of potential data that could be used to best predict RevPAR trends. Ultimately, a regression was chosen that included the following three economic indicators: Corporate Profits (2 months lead), Enplanements (coincident), and Unemployment (coincident). A summary of this regression is shown below.

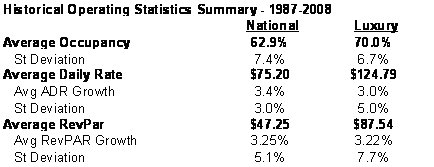

The three economic indicators chosen ultimately provided the highest R-squared (the proportion of variability in a data set that is accounted for by a statistical model) and made the most sense intuitively as potential drivers of RevPAR performance. Similar levels of R-Squared could be achieved by including additional economic indicators; however, they did not add meaningful value. Each of the three indicators intuitively makes sense as a potential driver of RevPAR. Corporate Profits are a good proxy for the health of corporations and their ability to send employees on business trips, thus impacting transient, business, and group demand for hotels. Enplanements measure the total number of individuals flying each month. This indicator represents the demand for travel for both individuals and corporations as each segment weighs the cost to fly as a potential component of the overall travel budget. Unemployment is a good proxy for both individual and corporate profitability and incomes, both of which will impact personal and business spending, including travel and hotel demand. Secondly, to differentiate the performance of all reporting U.S. hotels, Occupancy, ADR, and RevPAR on a national basis were compared to the luxury segment, also on a national basis. This analysis was performed to test the intuitiveness of the selected variables, in that the luxury segment is widely understood to have been one of the more volatile discretionary segments where RevPAR is concerned during economic swings, particularly during drastic recessions. The only question is, will the volatility be at the expense of occupancy or ADR. A summary of the overall U.S. and luxury data is shown below.

Looking first at occupancy, it is apparent the luxury segment has historically targeted a higher occupancy model compared to the overall lodging industry, with luxury occupancy averaging approximately seven to eight percentage points higher than national. Although not material, the volatility of occupancy in the luxury segment was somewhat lower. While the above occupancy data may imply that the luxury segment is somewhat more stable, the exact opposite can be proved by looking at the historical ADR data. The standard deviation of the year-over-year percentage change in ADR for the luxury segment has averaged 5.0 percent compared to 3.0 percent for the overall national average. This higher volatility more than offsets the more stable occupancy profile of the luxury segment and adds to a more volatile top-line (RevPAR) metric for the segment. As shown in the table below, over the last year, performance in the two segments has diverged as the luxury segment has come under more pressure.

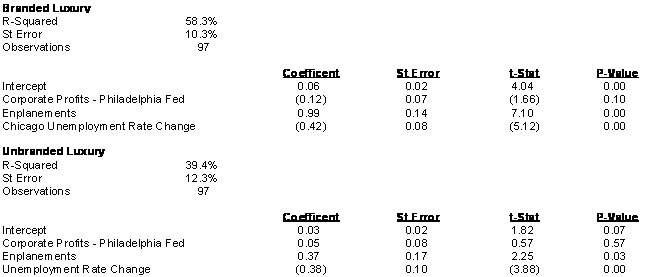

Based on the above data, it is apparent (not surprisingly) the RevPAR of the luxury segment is more volatile and exposed to positive and negative changes in the national economy as compared to the industry as a whole. After completing the national analysis of the economic drivers of the industry and a comparison of the luxury market to the overall industry, the same process was used to evaluate the Chicago test market for both the branded and unbranded luxury segments. For the Chicago market analysis, two data sets were used to evaluate the impact of certain economic drivers on historical RevPAR performance. The two data sets include RevPAR data from December 1999 (year-over year starting December 2000) for unbranded and branded luxury segments. The goal in looking at the Chicago market was similar to that of the evaluation of the national market. First, to determine whether the economic indicators that drive the national hotel market also drive the Chicago hotel market, and second, how each of the hotel segments performs relative to the chosen economic indicators. In addition, the Chicago analysis further evaluated sources of demand and non-room revenues. Ultimately, the three indicators chosen for the final Chicago regression were Corporate Profits, Enplanements, and Chicago Unemployment. These three are almost the exact same as the regression used for the national analysis, with the only change being Unemployment changing from a national to Chicago metric. A summary of the regression outputs for each segment can be seen below.

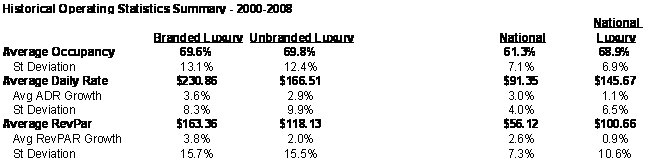

The R-Squared for the branded luxury segment is much lower than the regression used in the national analysis, but is still at a good level of credence at 58 percent. The unbranded luxury regression, however, demonstrates how unique this segment is and how difficult it is to forecast demand in this segment. The R-Squared for the unbranded luxury segment is very low and as can be seen in the low T-Stat (a measure of how extreme a statistical estimate is), the segment is less influenced by corporate profits than is the branded luxury segment. The lower R-Squared is also potentially due to very specific supply risks within submarkets and differing operating strategies, both of which could make macro level economic drivers less important. It also potentially indicates that the customer base for the unbranded luxury segment bases their travel decisions to a lesser degree on what is going on in the national economy and more about what is impacting them personally. In looking at the determinants of RevPAR, there appears to be very little difference in the volatility of either occupancy or ADR between the branded and unbranded luxury segments in Chicago (shown in the table below).

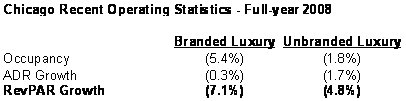

Both segments have managed to approximately 70 percent occupancy over the last nine years with annual volatility equal to approximately 12 to 13 percent. ADR has historically been significantly higher for the branded luxury segment as compared to the unbranded luxury segment; however, the volatility in ADR has been lower for the branded luxury segment. The final result when combining these two inputs and looking at volatility of RevPAR is that there is no material difference in RevPAR volatility between the branded and unbranded luxury segments. When compared to the overall national market and national luxury data, it is apparent that volatility in all metrics is significantly higher at the market level as compared to the national level. Also, as shown below, the branded luxury segment in the previous calendar year has actually come under more pressure as the economy has weakened when compared to the unbranded luxury segment. Could this potentially be due to the higher average price point for hotels in the branded luxury segment? Or perhaps due to a lesser ability for the hotels which are entangled in a web of corporate protocols to adapt very quickly on its operating strategy during economic fluctuations?

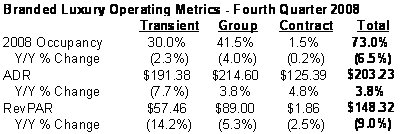

Looking strictly at the branded luxury segment over the fourth quarter of 2008, an analysis of RevPAR was performed for each of the demand segments. As shown below, the weakest performance was in the transient segment as compared to the group and contract segments. This is due to the stress that has been placed on the individual consumer and the need to cut back on both discretionary spending (for leisure transient travelers) and corporate spending (for commercial transient travelers).

The above data can be used by asset managers to help in adjusting their operating strategy to target the different segments depending on where the strengths or weaknesses are in the economy. One would expect the weaker transient demand shown above to correlate with weaker unbranded luxury performance due to the greater overall exposure to this demand segment. However, the difference may otherwise be driven in part due to the lower overall price point in the unbranded segment versus the branded sample. In analyzing all of the above data for the both the national and Chicago data, it evident that the luxury segment, both branded and unbranded, has a higher level of volatility in RevPAR, resulting in underperformance in periods of economic distress. Both the historical volatility data and recent RevPAR performance also support this analysis on a national level. When looking specifically at the Chicago level analysis, it appears the branded luxury is more correlated with the national economic drivers, while the unbranded luxury segment is less correlated. But both segments have historically demonstrated similar levels of volatility in RevPAR. In fact, and interestingly enough, the branded luxury segment has seen more weakness recently. To better understand the above volatility and respective segments, the demand segments for the branded luxury segment were analyzed. The results showed that transient demand has fallen by a significantly larger percentage recently relative to other segments. Despite testimonials by various players in the industry, there is no evidence to suggest that the statistical measurements of the highly volatile transient demand segment are mitigated when attributed to branded lodging facilities, versus non-branded or boutique assets. There are few theories about why there might be a lack of defensiveness of branded hotels (versus non-branded) because most professionals in the industry are conditioned to believe that brands offer significant mitigating characteristics during economic downcycles. Certainly, depending on the market or selection of hotels in a statistical analysis, there are cases that branded hotels are the better option. But the intent of this study is to illustrate that brands do not always offer fiscal resilience. Could the lack of such resilience in this study be due to the proliferation of online bookings, which are generally impartial between branded and non-branded hotels in reservation queries? Or the improving perception that luxury boutique properties offer significant value relative to their competitive branded counterparts? Whatever the battleplan might be, it is clear that no matter the shape, size, color or affiliation a property has, hotel owners cannot simply use the franchise badge as a crutch when times are bad or defer operational responsibilities to the franchise corporation in lieu of managing the asset properly. Most importantly, one cannot underestimate the value of property-level service as part of front-line defensiveness in economic swings. 1 The Value Proposition of Branded

and Unbranded Luxury Hotels in Today�s Real Estate Environment, authored

by Alvin Abriam, Joe Fisher, Sooyon Lee, Angela Rodriguez, Alfie Williams

and Bryan Younge. Special credit is given to Joe Fisher for compiling and

authoring the study�s statistical analysis.

Mr. Younge is a Director and Midwest Area Leader of the Hospitality & Gaming Group, a full service hospitality organization within C&W specializing in appraisal and consulting. Mr. Younge has completed appraisal, consulting and litigation related assignments on a wide range of hospitality assets throughout North America, Central/Latin America, Europe and the Pacific Rim. He has been active in real estate valuation and consulting since 1998, and has a Bachelor of Science Degree from Cornell University, as well as a Masters in Business Administration from Northwestern University's Kellogg School of Management. |

| Contact:

Bryan E. Younge, MAI, ASA

|

| Also See: | Local Internet Marketing Strategies for Franchised Hotels; Complement the Brand�s Efforts and Capture Local Internet Revenue Opportunities / Max Starkov and Mariana Mechoso / September 2008 |

.

|

|