advertisement

LE Reports The United States Lodging Construction Pipeline

at 5,652 Projects / 740,272 Rooms

Financial Crisis Impacting Development

and Transactions

.

|

News for the Hospitality Executive |

LE Reports The United States Lodging Construction Pipeline

at 5,652 Projects / 740,272 Rooms

Financial Crisis Impacting Development

and Transactions

.

| October 30, 2008 -

LE�s Construction Pipeline Overview at Q3

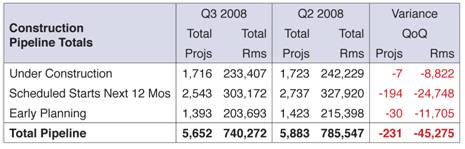

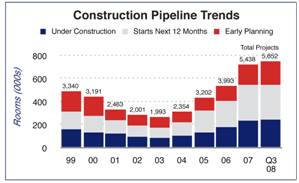

At the end of Q3 2008, the Total Construction Pipeline stood at 5,652 projects and 740,272 rooms, down 4% and 6% respectively quarter-over-quarter (QoQ). It�s the first quarterly decline in five years. Fall-offs are expected to continue into early next decade.

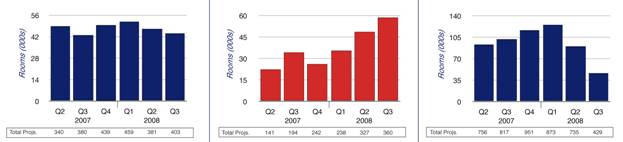

Key Pipeline Metrics Other metrics within the Pipeline underscore developer concerns. Construction Starts in Q3 were down for the second quarter in a row to 403 projects/44,477 rooms. The room count was down 7,387 rooms or 14% from the cyclical peak recorded in Q1 2008. Construction Starts are expected to continue declining for the foreseeable future. Cancellations/Postponements of projects already in the Pipeline increased for the third consecutive quarter and stand at 360 projects/58,949 rooms. Although up in all chain scales, the highest proportion of cancellations were for non-branded, independent projects larger than 200 rooms. New Project Announcements (NPAs) into the Pipeline are off significantly

at 429 projects/46,221 rooms. Project counts are down 51% and guestrooms

are down 63% from the peaks established in Q1. Only 4% of NPA�s in Q3 are

larger than 200 rooms. If the last recession is a guide, New Project Announcements

are likely to drift below 30,000 rooms per quarter early next year.

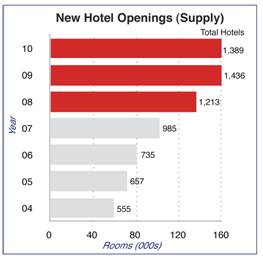

Top Markets Markets that were the fastest growth areas throughout the decade have the largest Pipelines today. New York, Phoenix, San Antonio, Houston, Washington, and Philadelphia have Pipeline counts that are 20% or more than their current guest room census counts. Other markets are important to monitor as well. Atlanta, with 129 projects in the Pipeline, and Dallas, with 116, will add significantly to their Current Census as early as 2009. Chicago, with 16,896 guestrooms in the Pipeline, and Orlando, with 15,375 rooms, also have strong Pipelines, but they won�t start to unfold until late 2010. Leading Companies & Brands Three of the leading Hotel Companies, Marriott, Hilton and InterContinental, have Development Pipelines � including both New Construction and Conversions � in excess of 100,000 rooms each. In order, Choice, Starwood and Best Western follow thereafter. InterContinental has the largest roster of projects in the Pipeline. At 1,244 projects, they are the only company with over a 1,000 projects under development. Activity is primarily driven by its mid-market brands: Holiday Inn, Holiday Inn Express and Candlewood Suites. Choice Hotels has the largest number of conversions at 243 projects, mostly for its Comfort Inn and Suites brand. LE�s Three-Year Forecast for New Hotel Openings

When considering that 233,407 rooms are already in the ground, and even after accounting for a rapid deceleration in future Construction Starts, these forecasts are still near certain to occur. Importantly, these New Opening counts will be at levels below the peaks for New Supply set in previous cycles, which could indicate a quick rekindling of developer activity once the lending crisis is over and the economic recovery gets underway. LE�s Transaction Trends

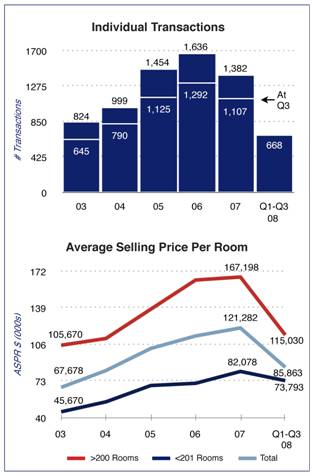

The Average Selling Price Per Room (ASPR) for transactions involving properties larger than 200 rooms topped out in 2007 at $167,198. In 2008, ASPR for these properties is down 31% from 2007�s peak and is at $115,030 per room. The ASPR for properties that are 200 rooms or less is down 10% from the 2007 peak to $73,793 in 2008. Financing has all but closed down for Individual Transactions larger

than 200 rooms. Only some smaller, branded, upscale and mid-market projects

are getting financed in this climate, mostly through smaller community

banks. Even though prices are declining, fewer buyers are active as greater

investor equity participation is required, interest rates are drifting

higher and other terms are tightening.

Then, what is likely to occur first are a series of forced hotel sales. Some will be due to the inability to refinance. Others will be adversely impacted by age or by new competitive pressures from New Supply coming online. Some consolidation is ahead. M&A and portfolio sales that will realign the industry are likely to take place after the credit crisis winds down and, perhaps, before the economic or lodging turnaround has commenced. Attractive investment opportunities could be available by mid-2009. Those with cash reserves, strong balance sheets and credit worthiness will be best prepared for the opportunities that will arise. |

| Contact:

Kathleen Hurley

|

While

declines were modest in the Under Construction and Early Planning stages,

they were down significantly in Scheduled Starts in the Next 12 Months.

213 projects actually migrated backwards into Early Planning, a sure indicator

that the credit crisis and softening lodging operating statistics, both

of which have worsened materially in the last 90 days, are having an adverse

impact on developer thinking.

While

declines were modest in the Under Construction and Early Planning stages,

they were down significantly in Scheduled Starts in the Next 12 Months.

213 projects actually migrated backwards into Early Planning, a sure indicator

that the credit crisis and softening lodging operating statistics, both

of which have worsened materially in the last 90 days, are having an adverse

impact on developer thinking.

Projects

Under Construction peaked in Q2. Having fallen slightly to 1,716 projects/233,407

rooms, Q3 is the fifth quarter in a row where the room count has exceeded

200,000 rooms. Consequently, LE�s Forecast for New Hotel Openings

at Q3 has been revised only minimally. It stands at 1,213 hotels/135,070

rooms, with a 2.8% gross growth rate for 2008. In 2009, the Forecast calls

for 1,436 new hotels/158,851 rooms, a 3.3% growth rate. 2010 will see New

Openings of 1,389 hotels/158,889 rooms and a 3.2% growth rate. Net growth

rates will end approximately ±.2% lower after hotel closings and

other removals from the current Census are compiled.

Projects

Under Construction peaked in Q2. Having fallen slightly to 1,716 projects/233,407

rooms, Q3 is the fifth quarter in a row where the room count has exceeded

200,000 rooms. Consequently, LE�s Forecast for New Hotel Openings

at Q3 has been revised only minimally. It stands at 1,213 hotels/135,070

rooms, with a 2.8% gross growth rate for 2008. In 2009, the Forecast calls

for 1,436 new hotels/158,851 rooms, a 3.3% growth rate. 2010 will see New

Openings of 1,389 hotels/158,889 rooms and a 3.2% growth rate. Net growth

rates will end approximately ±.2% lower after hotel closings and

other removals from the current Census are compiled.

Just

as the financing crisis has impacted development activity, it has also

seriously affected transactions. The volume of Individual Hotel Transactions

peaked in 2006 at 1,636. For the first three quarters of 2008, 668 transactions

were closed, down 48% from Q1-Q3 2006.

Just

as the financing crisis has impacted development activity, it has also

seriously affected transactions. The volume of Individual Hotel Transactions

peaked in 2006 at 1,636. For the first three quarters of 2008, 668 transactions

were closed, down 48% from Q1-Q3 2006.