advertisement

..

.

|

News for the Hospitality Executive |

|

|

| by Karen L. Johnson, Warnick + Company

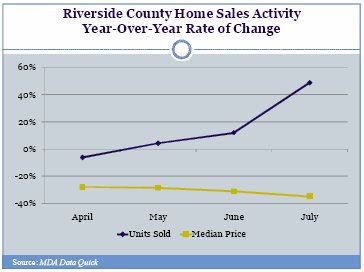

September 2008 Fortunately, wringing the speculation out of the oil markets appears to have saved us from a brutal recession in favor of a minor but prolonged one. Unfortunately, 9 out of 10 American consumers believe we are in a recession.1 Now that the effect of the economic stimulus checks has been felt, personal income is falling, by 0.7 percent in July as compared to June. Not surprisingly Smith Travel Research reports that, although revenue per available room (�RevPAR�) grew slightly in July, August entered negative territory. RevPAR declined 1.8 percent, 1.7 percent, and 0.8 percent for weeks one, two, and three in August, respectively. Actual results were not in, but the American Automobile Association�s forecast for Labor Day travel indicated fewer trips and put travel at the lowest level since 2002. Week four numbers showed positive RevPAR growth, but credited the national conventions for much of it. The signs are fairly clear � from a hotel industry standpoint, we have entered a mild but stubborn recession. In the Fed�s most recent beige book, the businesses interviewed reported strains brought on by a battered real estate market, tapped-out consumers, and stubbornly high prices for staples.2 Negative variances to budget will increase with each remaining month and most hotels will miss budget in 2008. Operators will be challenged during 2009 and beyond to understand the causes and implications for their individual markets and properties. �Orderly� Bank Failures An oxymoron? The Fed stepped in on September 7th before either Fannie Mae or Freddie Mac actually failed. In August, the head of the FDIC signaled its intent to borrow from the US Treasury Department when only nine banks had failed. The last time the Fed borrowed from the Treasury was in the latter years of the Resolution Trust Corporation (�RTC�) when over 750 thrifts failed in the late 1980s and early 1990s. The bad news is we will have bigger problems this time around. The RTC bail-outs were of substantially smaller institutions and cost the tax payers only $480 billion.3 The combined total of the housing bill that passed in July and the Fannie Mae and Freddie Mac bail-out have put taxpayers on the hook for $500 billion in loans and guarantees. Estimates for cleaning up this mess range between $1.0 and $2.0 trillion (with a �t�) when private sector losses are factored in. The concern is that increased government debt will push up the yields on treasuries, which will translate into higher interest rates and even more foreclosures. The more immediate problem is that credit will remain tight through 2009 as lenders themselves struggle to repay $790 billion in floating rate notes 4 that they took out last year at the same time they need to increase their cash reserves. That means reduced lending to clients for business expansions and capital improvements, impeding new job formation. Inside Mortgage Finance magazine reports that lending fell 10 percent between the first and second quarters of 2008.5 There is widespread belief that the credit crisis will not end until home values stabilize. 6 The sub-prime debacle is the virus that is spreading through all lending and then the wider economy. The Path to Home Value Stabilization Lenders learned at least one lesson from the prior crisis and that was to cut prices quickly and decisively to unload foreclosed properties and stimulate transaction activity. Nationally, home sales pace in July was up 3.1 percent, pulled up by larger increases in the highest foreclosure states (California and Florida). Riverside County, California, which may be in the top three most affected, experienced a nearly 49 percent increase in home sales velocity. But the medicine burns going down; buyers watched prices skid along the bottom before stepping in at discounts of 30 to 35 percent to pricing for the same months of 2007. You will know that housing prices have stabilized when they roll back to 2003 or 2004 values.

The majority of the notes defaulting now originated between September 2005 and November 2006. Since loan originations fell off sharply in early 2007, foreclosures should revert to traditional triggers: job losses, major medical bills, divorce, and the like. How widespread is it? California is one of the hardest hit states and, through June 2008, only 2.4 percent of the homes and condos have been taken back. The real impact is psychological. Consumers feel poor. Home equity lines will be used for new roofs, not vacations. From the Fed�s newest beige book: �Consumer spending was reported to be slow in most districts, with purchasing concentrated on necessary items and retrenchment in discretionary spending.� Discretionary dollar (leisure) travel will be down. In most markets, social catering spend will be down. Timeshare and fractional sales, which held up after 9/11, will also be affected. A Smart Virus Doesn�t Kill the Host After oil spiked to $145 per barrel, demand fell off. Drivers logged 3.7 percent fewer miles on the nation�s highways in May as compared to the same month of last year. Airlines announced that flight capacity will be cut by 10 percent after Labor Day. Just as with the �energy shortage� at the new millennium, a significant component of the run-up was driven by speculation and windfall profits. Retail gas prices have receded almost 40 cents per gallon since the peak � but to a new, higher plateau based in part on increased demand from China and India. One index of consumer confidence bounced up 10 percent on that note, one of the few bright spots in this summer�s economic news. Watch oil� it has a disproportionate effect on consumer confidence. Unfortunately, the run-up in air fares has dampened demand at a faster rate than the legacy carriers can cut flights. A recent article in The Nation7 suggests that the legacy airlines will have to cut capacity back to pre-deregulation levels and achieve double-digit fare increases to survive. Expedia indicates that air fares for the fourth quarter of 2008 are up by an average of 16 percent. Routes that were heavily discounted previously, like New York, are up 27 percent. Air travelers will pay more, but get fewer flight delays as a byproduct. A troubling question is whether rapidly increasing airfares will exacerbate demand reductions and push the airline industry into a vicious downward cycle. For 2008 and 2009, hotels in fly-to destinations should expect reduced business travel as employers �pile on� to the cost control trend. The following is excerpted from a July purchasing industry periodical on controlling business travel expense.

�The theme for the rest of the year is demand management,� says DeAnne Dale, vice president for strategic account management and consulting services for Travelocity Business in Dallas. �That is, companies will be asking themselves such questions as: �Do we need to have so many incentives meetings?� �Are they motivating our sales staff?� They will look at decreasing travel without impacting their business.�8 Expect poorer pick-up in groups with fewer delegates, decreased food and beverage spending, shorter lengths of stay, and more doubling up; however, it is leisure that will be hit hardest. The temptation to cut rates must be resisted. Numerous studies have shown that this will not sufficiently stimulate demand. Yield manage, but don�t cut rates. Staycations? A July survey of 2,231 American adults 9 revealed that only nine percent were substituting a �staycation,� for a vacation they otherwise would have taken out of town during the next six months. The reasons given were: �gasoline prices are too high� (61 percent), �travel in general is too expensive� (44 percent), and �cutting back on discretionary spending� (43 percent). The good news is that one in five of these cost cutters said that they expected to stay in a local hotel, motel, or resort for at least one night. One in seven American leisure travelers said they had taken a �staycation� during the prior six months. The worst may be over, but reduced disposable income will push average daily rates (�ADRs�) backward in non-gateway leisure markets, as captured in a recent Orlando Sentinel headline: �Hotel Room Rates in Metro Orlando Area Dip -- 1st Time Since 2003.� For how long? For as long as job losses increase and as long as foreclosure signs are hanging out on lawns. See second paragraph, above. The effects of the economizing will be uneven. Hawaii is being crushed, Orlando is down modestly, but Miami is attracting enough Canadians and Europeans to offset domestic declines due to the still relatively weak dollar. A Weak Dollar Cuts Both Ways Much has been written in our trade publications about the attractiveness of US gateway cities now that our dollar is weak and its impetus to domestic vacations. But, the weak dollar is partially to blame for the rapid run-up in oil prices � oil is a dollar denominated commodity. The flip side of this is the cost advantage accruing our manufactured goods on the world markets and what that means for skilled employment in the United States. One recent commentator in The Wall Street Journal referred to exports as the �lifeline� to our economy.10 Exports helped drive durable goods orders up 1.3 percent in both June and July, with the biggest winner being aircraft (up 28 percent). In August, however, the dollar regained eight percent of its strength against the Euro and even more against the pound. Think of it as the echo of our diminished consumption of imported goods. Economists expect that this will dampen global demand for our manufactured items. The question is, by how much? Hotel properties located in manufacturing centers should not be tarred with a recessionary brush unless the dollar continues to fall. And, with export driven agribusiness booming too, the Great Plains are a good place to own a hotel right now. Speaking of agribusiness� My Food Costs are Going Through the Roof The economic development in the developing world is triggering unprecedented demand for US food products, which is amplifying the cost increases attributable to increased fuel costs in harvesting and transportation costs, and competition for corn from the bio-fuel industry. This phenomenon is not likely to change. Perhaps the US food service industry should revert to the portions sizes of the 23 percent, from 5.7 ounces to 7.0 ounces. Most of America is on a diet and women now comprise 50 percent of the traveling public. Before you increase your menu pricing 20 percent, do two things. Try and eat the entire portion from two courses on your menu. Does it feel like Thanksgiving? Go back to the bussed trays and look at what is left on the plates. Skip the re-print and cut portion sizes? Long term: think about smaller plates for your next china change out.

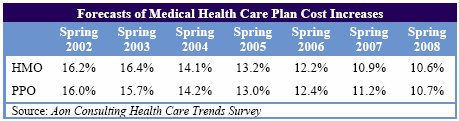

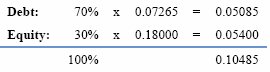

Well, the rate of growth in employee health care seems to be tapering off. While still in doubledigits, Aon Consulting�s survey of forecasted plan cost increases is at its lowest level in seven years. Talk of national health insurance may act as a brake in the near term but our workforce is aging. Our industry needs to continue to look for more opportunities to automate. Cost pressure from numerous areas (labor, food products, and energy) will outpace revenue growth. Re-bid contracts and review your staffing assumptions. Net operating income (�NOI�) will be under a great deal of pressure. And Then the New Supply Hits Low cap rates and easy money have contributed to another wave of new additions. Smith Travel Research attributes most of the recent occupancy declines to new supply, not declining demand. Lodging Econometrics reports that rooms under construction held firm between the first and second quarters of 2008 at 242,000 new rooms; the limited number of bank failures thus far suggests that they will all be completed. Supply will likely grow 2.9 percent in 2008 and 3.4 percent in 2009.11 The real question is how many of the 328,000 rooms that are scheduled to begin construction within the next 12 months will break ground, and when. If 50 percent are built, another 3.3 percent will be added in 2010. Let�s hope the new rooms are all in markets that are underserved. Will There Be RTC-Scale Hotel Bargains? Not yet, transaction pace has slowed to a crawl. Jones Lang LaSalle reports that in the US hotel sales pace is off over 80 percent from the first half of last year. Buyers don�t want to �catch a falling knife.� Sellers don�t want to acknowledge the new, higher cap rates. But some owners won�t have a choice in when and whether they sell. How big will the problem be? HVS data indicates that there were approximately 250 hotel sales (above $10 million) between April 2006 and April 2007, the peak of the hotel financing frenzy. The sale prices for the 68,000 rooms aggregated to $13.4 billion. Still other hotels were built and re-financed at relatively high loan-to-values. Most of these loans anticipated continued and substantial real growth in NOI. The borrowers will be fortunate to �preserve� � let alone grow � 2007 cash flow over the next two years. What, in hindsight, looks like imprudent levels of leverage were provided via short-term notes maturing in 2008 and 2009. No alternate lenders will be there for take-outs at the current loan balances and loan-to-value ratios. Some owners will step up their equity and work-outs will be negotiated for other borrowers if they will step up to fund the capital expenditures necessary to be good stewards � if their lenders don�t fail and if they are not CMBS loans (where there is no one to negotiate with). The other properties will be foreclosed upon and liquidated, quickly by still solvent banks and slowly by the successor to the RTC. It took Congress a year of arguing to structure the RTC. We may see the greatest number of distressed hotel transactions in 2010. Whether or not these trade at the early 90s mantra, �12 on trailing 12� will be determined by the pace of the return of credit and pricing. The distressed pricing of the hotels sold by banks or the government is likely to put downward pressure on average daily rates. If you can buy a $20 million asset for $10 million, you have the ability to sell the rooms a lot cheaper than the investor who bought or built at $20 million. What Happens to Cap Rates? For most assets, the day of the 6.0 and 7.0 percent cap is gone. They are drifting back up and will stay there. Consider this, the average going-in cap rate for hotels was 10.8 percent12 between 1992 and 2005 according to RERC�s annual surveys of institutional investors. Not possible? Look at the math. A capitalization is a weighted average of the cost of debt (the mortgage constant) and the buyer�s levered internal rate of return (�IRR�) expectations. For a deal that is 70 percent financed with a first mortgage at 6.0 percent interest with a 30-year amortization and by an equity source with a targeted IRR of 18 percent, a logical cap rate would be 10.5 percent, as follows.

Any investor that buys at a cap below 10.5 percent at the above terms is banking on real dollar growth in the NOI. His/her profit is not realized until the exit and is predicated on a rebound in ADR at a rate that is greater than inflationary growth in expenses and, for full-service operators, lockstep growth in menu pricing and food cost. If you are going to have to sell within a three-year window, it might be wise to do it now, before your cash flow has trended down for two years and before the liquidation-flavored foreclosures hit the market. Otherwise, wait it out. Recovery by 2011 The retail gas shock may have sown the seeds of our next recovery. July durable goods orders for motor vehicles and parts rose 1.2 percent, turning the tide on a 15.7 percent slide over the previous 12 months. Observers speculate that the carriers are replacing older aircraft and consumers who can afford to make a switch are changing over to fuel-efficient cars. The �bank owned� signs will come down. The American taxpayer and consumer become inured fairly quickly to increased debt. No one seems to know or care that the previous bail-out hasn�t been paid for yet. Face-to-face business will get done, and there will be more reasons to attend a meeting or convention than skip it. In addition, in that same survey on �staycations� there were positive, long-term signs for the leisure industry.

1 Kelly Evans, �Personal Income Falls, Sentiment is Weak,�

The Wall Street Journal, August 30, 2008

About Warnick + Company Warnick + Company is a strategic advisory firm that specializes in the lodging and recreational real estate industries. With offices in Chicago, Los Angeles, New York, and Phoenix, the firm provides consulting, asset management, investment banking, and development management services to investors, developers, financial institutions, hotel companies, and government agencies worldwide. |

| Contact:

|

.

Fully

64 percent of the July sales in Riverside County were of foreclosed properties

as compared to 53 percent in April. Fortunately, the rate of increase in

foreclosures is abating. Notices of default across California were up only

6.6 percent between the first and second quarters of 2008, after doubledigit

increases for the four preceding quarters.

Fully

64 percent of the July sales in Riverside County were of foreclosed properties

as compared to 53 percent in April. Fortunately, the rate of increase in

foreclosures is abating. Notices of default across California were up only

6.6 percent between the first and second quarters of 2008, after doubledigit

increases for the four preceding quarters.

Any

Relief in Expenses?

Any

Relief in Expenses?

Karen

Johnson specializes in hotel management contract issues, master-planned

resort development, hospitality brand development, litigation support,

due diligence underwriting and valuations of complex assets. A graduate

of Michigan State University�s School of Hotel, Restaurant & Institutional

Management her consulting career began at Pannell Kerr Forster in 1981

and led over the years to the feasibility group at Marriott International,

Gloodt Associates, PKF Consulting, and Landauer Associates. Ms. Johnson,

a member of the International Society of Hospitality Consultants (ISHC),

has provided expert witness support for cases being litigated or arbitrated

in California, Illinois, Nevada, Texas, and London.

Karen

Johnson specializes in hotel management contract issues, master-planned

resort development, hospitality brand development, litigation support,

due diligence underwriting and valuations of complex assets. A graduate

of Michigan State University�s School of Hotel, Restaurant & Institutional

Management her consulting career began at Pannell Kerr Forster in 1981

and led over the years to the feasibility group at Marriott International,

Gloodt Associates, PKF Consulting, and Landauer Associates. Ms. Johnson,

a member of the International Society of Hospitality Consultants (ISHC),

has provided expert witness support for cases being litigated or arbitrated

in California, Illinois, Nevada, Texas, and London.