July 2, 2008 (USA) � Lodging Econometrics (LE), the Global Authority

for Hotel Real Estate, has released its Construction Pipeline Report for

Europe, announcing the Total Construction Pipeline at a new cyclical high

of 1,031 projects/172,815 guestrooms at the end of Q1 2008. LE President

Patrick Ford commented, �The Pipeline in Europe continued to grow, propelled

by peak occupancy rates, ADR and RevPAR in many markets, as well as the

ongoing global development surge of the very popular, smaller, contemporary

branded hotels, particularly in the upscale and mid-market segments.�

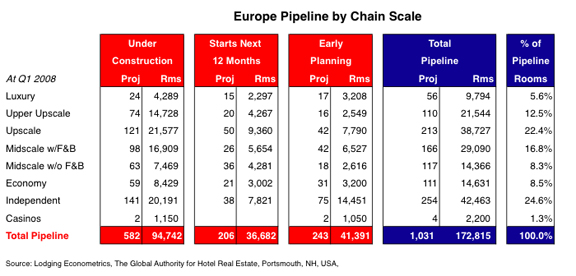

There are a cyclical high 582 projects/94,742 rooms currently Under

Construction, some 55% of project and room counts in the Total Pipeline.

With financing for these projects secured earlier, developers have noticeably

rushed to get underway and opened. Totals in Early Planning also reached

a cyclical high of 243 projects/41,391 rooms. In the wake of the credit

crisis, larger projects in the Pipeline not yet under construction are

encountering some difficulty in securing financing and will idle while

developers wait for the credit crisis to resolve. As a result, totals for

projects Scheduled to Start Construction in the Next 12 Months have decreased

to 206 projects/36,682 rooms. All projects included in the LE Pipeline

have dedicated land parcels, are being actively pursued by developers and

have been verified by the brands.

Ford noted, �With Europe�s abundance of international business and financial

centers, the historic and cultural allure of its capital cities, the shortage

of land parcels, and the high barriers to entry, Europe�s lodging industry

remains a very attractive investment sector. The challenge is finding financing,

as institutional lending for mixed-use projects and larger, freestanding

hotels has evaporated. Still, there are a few smaller lenders without balance

sheet difficulties willing to provide financing to experienced developers,

particularly if their project involves a globally recognized brand. Generally,

the projects finding financing are smaller and the terms are more stringent.�

Ford noted, �With Europe�s abundance of international business and financial

centers, the historic and cultural allure of its capital cities, the shortage

of land parcels, and the high barriers to entry, Europe�s lodging industry

remains a very attractive investment sector. The challenge is finding financing,

as institutional lending for mixed-use projects and larger, freestanding

hotels has evaporated. Still, there are a few smaller lenders without balance

sheet difficulties willing to provide financing to experienced developers,

particularly if their project involves a globally recognized brand. Generally,

the projects finding financing are smaller and the terms are more stringent.�

Lodging�s operating performance has been excellent through early spring,

particularly in Northern and Western Europe. For the most part, developers

remain optimistic, thinking the slowdown from high operating peaks, while

prolonged, should be shallow. As a result, developers are looking beyond

today�s concerns and into the next cycle, thinking the lending crisis will

eventually right itself.

LE�s Forecast for New Hotel Openings

During

Q1 2008, 57 New Hotels/8,691 rooms came online. LE�s Forecast for the rest

of 2008 calls for 233 New Hotel Openings with 32,349 rooms, and 361 Hotels/56,316

rooms in 2009. With 94,742 guestrooms currently Under Construction, these

projected New Openings are already in the ground, making LE�s New Supply

Forecast for 2008-2009 a certainty. During

Q1 2008, 57 New Hotels/8,691 rooms came online. LE�s Forecast for the rest

of 2008 calls for 233 New Hotel Openings with 32,349 rooms, and 361 Hotels/56,316

rooms in 2009. With 94,742 guestrooms currently Under Construction, these

projected New Openings are already in the ground, making LE�s New Supply

Forecast for 2008-2009 a certainty.

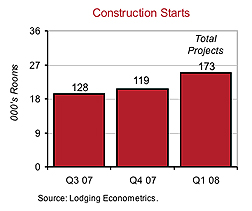

Construction Starts Jumped Forward in Q1

New Construction Starts for hotels already in the Pipeline jumped up

in Q1 2008, with 173 projects/24,938 rooms now underway. These projects

had financing in place before the credit crisis materialized. Postponements

and Cancellations trended upward to 45 projects/8,318 rooms. The reduced

availability of financing will likely restrain Construction Starts going

forward, and will also result in increased Postponements and Cancellations.

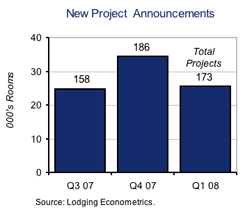

Fewer New Projects Announced in Q1

After

peaking in Q4 2007, New Project Announcements into the Construction Pipeline

declined to 173 projects/25,488 rooms. As New Project Announcements are

a key indicator of developer sentiment, this slowdown underscores the disappearance

of institutional financing for large four- and five-star projects, and

the growing popularity of smaller, mid-market branded properties that are

easier to finance. After

peaking in Q4 2007, New Project Announcements into the Construction Pipeline

declined to 173 projects/25,488 rooms. As New Project Announcements are

a key indicator of developer sentiment, this slowdown underscores the disappearance

of institutional financing for large four- and five-star projects, and

the growing popularity of smaller, mid-market branded properties that are

easier to finance.

Many New Project Announcements are located in London, as well as in

other cities throughout the UK, and are set to open early next decade in

anticipation of the tourist boom for the 2012 Olympics. There are also

a large number of New Projects announced in emerging markets in Central

& Eastern Europe (CEE) and the Commonwealth of Independent States (CIS).

Country and Market Trends

The United Kingdom, a target area for every global brand, has the largest

Total Pipeline in Europe, with a total of 321 projects/46,531 rooms. 75

projects/14,010 rooms are in London, 44 of which are expected to come online

in 2010 and beyond, as the city prepares to host the 2012 Olympics. High

levels of development with New Openings planned for early next decade are

also seen in other urban areas and key industrial centers. Among the cities

expected to benefit from increased travel are Birmingham, Manchester, Liverpool,

Edinburgh, Aberdeen, Sheffield, Leeds, and Glasgow, which have a combined

83 projects/13,271 rooms.

Other than in Russia and the CIS countries, where Pipelines are just

beginning to form, Pipelines in other European countries were seeded much

earlier in the decade and have 50% or more of their projects already under

construction and have a heavy flow of New Hotel Openings scheduled for

2008-2009.

Spain has the second largest Pipeline in the region with 179 projects/27,701

rooms, led by Madrid with 20 projects, Barcelona with 19, then the port

city of Malaga, all popular tourist and cultural hubs. Germany has 76 projects/14,274

rooms in various stages of development. The capital of Berlin has 13 projects/3,148

rooms, followed by the financial centers of Frankfurt and Munich, and the

industrial port city of Hamburg. France�s Total Pipeline has 56 projects/6,347

rooms. Its capital, Paris, leads with 11 projects.

Countries in Central & Eastern Europe (CEE) are enjoying growing

economies, increased consumer spending and an expanding flow of inbound

tourists. Lodging companies have aggressive growth strategies in these

countries, targeting their high-end brands in the capital cities and their

mid-market hotels elsewhere.

The Czech Republic has 19 projects/3,320 rooms in its Pipeline. Prague,

the capital, accounts for 15 of those projects. Of Poland�s 16 projects/2,449

rooms, 3 are in the capital of Warsaw, with the remainder in key locations

like the main seaport of Gdansk, education hub Poznan, and Katowice, a

major coal and steel center. With its celebrated coastline on the Adriatic

Sea, Croatia is gaining ground as a resort destination. The country has

14 projects/3,319 rooms in its Total Pipeline, all in coastal locations

such as Zadar, Split and Dubrovnic.

Russia has the fourth largest Pipeline in Europe with 60 projects/14,261

rooms. 21 projects are in Moscow, which is rapidly expanding due to growing

oil and gas revenues. 11 projects are in historic, more tourist-oriented

Saint Petersburg. Kazakhstan has 9 projects/1,801 rooms in its Pipeline,

mostly in its capital and commercial center, Almaty.

While modest compared to the rest of Europe, the Pipeline in the CIS,

at 79 projects/18,364 rooms is likely to expand quickly. Several global

lodging companies recently outlined expansive development aspirations in

this area, for Russia in particular.

For Global Companies, Upscale and Mid-Market Brands Are Finding

Favor

Approximately 75% of projects in the Construction Pipeline have already

made a branding decision. Of the remaining 25%, nearly 80% will make a

branding decision prior to opening. This may be a surprising observation

to some, as a sizeable portion of Europe�s Current Supply of Open and Operating

Hotels is unbranded. But, as elsewhere, the branding revolution is well

underway in Europe, as global companies see great opportunity in rapidly

expanding their modern, contemporary branded concepts so popular with global

travelers.

InterContinental Hotels Group leads development in the region, with

137 projects in their Pipeline. The company�s midscale offerings are most

prominent. This includes 34 Holiday Inn projects, many of which will be

in the United Kingdom and Russia, and 68 Express by Holiday Inn projects,

the majority being sited in the UK, Germany and Spain.

Marriott continues to expand its global reach with 33 projects in its

Pipeline, 15 from its high-end brands: Ritz-Carlton, Marriott and Renaissance;

as well as 18 Courtyards. The company has plans to further expand its European

portfolio, which includes an added focus on the Courtyard brand. A number

of New Project Announcements will soon be forthcoming for the Edition brand,

an exciting new venture between Marriott and noted boutique hotel developer/designer

Ian Schrager.

Hilton Hotels has 31 projects in its Pipeline, 19 of which will be

from its Hilton Hotel brand. The company is aggressively increasing its

presence throughout Europe with its new, enlarged portfolio of brands,

including Doubletree Hotels, Hilton Garden Inn and Hampton Inn. Joint ventures

are a preferred strategy for Hilton to accelerate the introduction of its

family of brands throughout the region. Recent joint venture agreements

include 15 projects in the UK, 25 properties throughout Russia, and another

25 hotels in Turkey.

Starwood�s 22 projects in their Pipeline draw heavily from their portfolio

of luxury and upper upscale offerings, including 10 large, full-service

Sheraton Hotel projects.

European-based global companies are active and strong pace-setters

throughout the region.

France�s Accor has 92 projects in its Pipeline, including 41 midscale

Hotel Ibis properties, with 11 in France and 13 in Spain. Accor also has

significant development with their budget brand Etap Hotels with 22 projects,

mostly in the UK, France and Spain.

Rezidor Hotel Group, based in Belgium, has 74 projects in their Total

Pipeline, with 40 to be upscale Radisson SAS properties, 23 of which will

be in emerging markets in CEE and CIS countries. Rezidor also has 30 projects

in its mid-market Park Inn brand.

Kempinski Hotels & Resorts has 14 projects, most already Under

Construction and being built in Central & Eastern European countries,

including Croatia, Slovakia and Latvia.

Spain-based NH Hoteles has 21 projects in their Pipeline, while Sol

Melia Hotels & Resorts, has 11 projects, 7 of which are their mid-market

Sol Hotels brand.

For UK hotel companies, Whitbread has 16 Premier Inn projects making

up their Pipeline, and budget hotel company Travelodge has 38 projects.

All projects are being developed in the UK.

Summary

The Construction Pipeline is set to unfold at a quickening pace throughout

Europe, with over 88,800 rooms forecasted to come online over the next

two years. Much of this is already under construction and is certain

to occur. However, the lending crisis and resulting uncertainty have projects

in Early Planning idling a bit, while developers wait for the financing

situation to improve.

The number of New Project Announcements into the Pipeline is declining

as developers await more visibility about how the financial crisis, rising

inflation and slower economic growth rates will impact existing hotel operations.

The summer travel season will be a true test, as we assess how consumers

react and businesses respond to changing economic conditions. A few more

months are needed for new trend lines to take shape, before we can project

the future impact on both hotel operations and development trends.

Lodging Econometrics (LE) is the global authority for hotel real estate.

LE conducts Supply Side research for all markets, countries, companies

and brands � worldwide!

To learn more about LE's products and services, please contact LE at

+1 603-431-8740 ext. 25. Or visit online at www.lodgingeconometrics.com. |