|

Fewer Asset Listings and Less

Debt

Lodging/Residential Development Evolution . |

HOSPITALITY RESEARCH + CONSULTING SPECIALISTS |

|

|

|

Fewer Asset Listings and Less

Debt

Lodging/Residential Development Evolution . |

HOSPITALITY RESEARCH + CONSULTING SPECIALISTS |

|

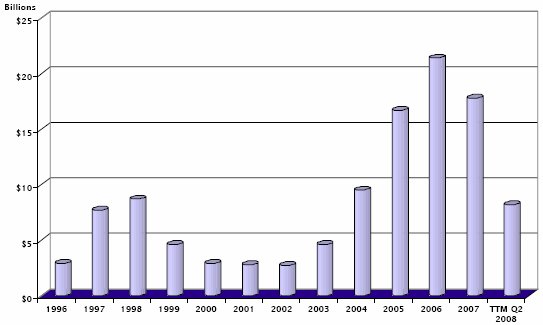

On the Downward Slope Economic Concerns Weigh on Investment Environment As 2007 drew to a close, it was clear that 2008 would taper from the

robust transaction pace experienced over the past three years. Most did

not expect the falloff in deal volume to occur so abruptly, however. The

number of deals and total transaction volume through the second quarter

is one-fourth the amount during the same period last year. Roughly $3 billion

in transactions occurred during the first half of 2008 with a mere 45 assets

trading.

The sale of the Hyatt Regency Century Plaza represented the largest transaction during the first half of 2008. It is the second time the hotel changed hands in the past three years. Deal activity has not been this slow since 2003 when the economy was just beginning to rebound from a recession. The chart below shows the decline in activity as it relates to the prior two real estate cycles. Clearly we are on the downside of the most robust cycle that lodging investments have experienced. While the current environment is almost stagnant in comparison to the height of the market in 2006, deal volume remains above the slow pace of the prior recession between 2000 and 2003. Going back to the last half of 2007, just over $8 billion in transactions took place during the past twelve months. . 1996-Q2 2008

Source: Hospitium UPSCALE & LUXURY LODGING TRANSACTIONS

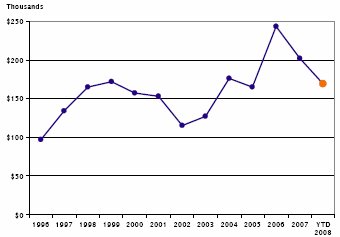

As the table above indicates, the year-overyear comparisons are eye-opening, but probably not surprising. The number of properties sold, total transaction volume, and average price per room have all exhibited dramatic declines in 2008. Closing deals has become more onerous as many sellers still expect high valuations and buyers must work harder to obtain debt. While debt is still available, the loan-to-value ratios are down and spreads have widened. Favorable debt terms were a key component that helped drive pricing during the market peak. Additionally, a less rosy economic outlook has resulted in more conservative underwriting over the past several months. The average price per room continues to slide from 2006 when it hit

$240,000. Several factors have restricted per-key pricing on assets. First

and foremost, with the state of the economy, the condo-hotel fallout, and

the mortgage crisis, residential economics are not currently a factor in

underwriting most new acquisitions. Moreover, high-end resorts and large

multi-faceted properties are virtually absent from the transaction landscape.

A mere two true luxury properties sold over the past six months, and only

four properties located in resort destinations traded during the period.

AVERAGE PRICE PER ROOM

Source: Hospitium

UPSCALE AND LUXURY LODGING TRANSACTIONS

TOP TRANSACTIONS Only four assets topped the $100 million threshold thus far in 2008, further illustrating the scarcity of large, high-end product on the market. At a price of $366.5 million, the Hyatt Regency Century Plaza was the most significant transaction to occur over the past six months by a wide margin. The next highest priced deal was the Renaissance M Street at $141.3 million. All of the assets that attracted high per-room pricing were located in primary urban markets, namely New York, Chicago, Washington DC, and Los Angeles. The Century Plaza and the new Duane Street Hotel in New York were the only two deals to surpass the $500,000 per key mark over the first two quarters. It seems like it was only yesterday when $800,000+ per room was more common for top asset trades. The sales of the Hyatt Regency Century Plaza, the James Chicago and the Renaissance M Street illustrate that it is still possible for sellers to book a gain on asset dispositions in the current market. Each traded within a 3-year hold period and each showed appreciation at a level well above inflation. OUTLOOK As previously discussed, we anticipate the total 2008 upscale and luxury transactions to be around $5 billion to $6 billion. The big question is where will the market go from here? Many operators already anticipate a difficult 2009 with the lagging falloff in the leisure and group segments expected to hit properties. Economic conditions are not expected to rebound until 2009 at the earliest as airlines struggle to remain solvent, gas prices remain high, and the mortgage crisis continues to burden lenders. Many analysts believe that the market will begin to rebound by mid-2009, bringing more lenders back to the table and inducing investors to underwrite stronger performance growth once again. Lodging Development and Residential

Risk

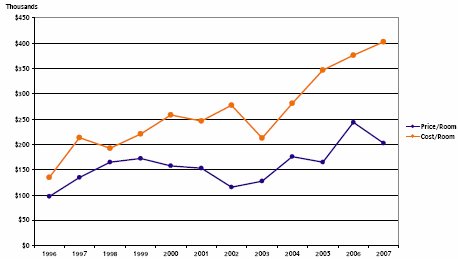

During the height of the transaction market in 2006, when acquisition competition was intense and pricing was frothy, some pondered whether new development might actually be more economical. In some markets, this may have been true; but in general, costs continue to soar above sale prices. The gap between cost and price for upscale and luxury lodging facilities has swelled over the past eleven years. In late 1990s, the ratio of price to cost was approximately 70%-80%. In recent years, the ratio has fluctuated between 50% and 65%. This is quite telling given the exorbitant growth in price per room between 2002 and 2006. Between 1996 and 2007, the average price per room for upscale and luxury

lodging transactions has increased at an average annual rate of 6.9%. Over

the same period, the average cost per room increased at an average annual

pace of 10.5%. The prices of steel, concrete and other construction materials

continue to rise. Fuel costs have further impacted project expenditures.

Some of the cost inflation is due to additional facilities, amenities,

and infrastructure that are necessities for hotels today. Spas, fitness

facilities, business centers, in-room technology, fire and safety items,

and ADA compliance have all factored into the rising costs. The latest

cost addition to new hotels has come as a result of the environmental movement.

Reducing carbon footprints, improving energy efficiency, and even gaining

LEED certification comes with much higher upfront costs.

UPSCALE & LUXURY LODGING FACILITIES

Source: Hospitium THE RISE OF RESIDENCES To compensate for the rising cost of construction, developers and hotel companies have looked to additional return opportunities. Many proposed upper-upscale and luxury hotels are now part of larger mixed-use projects with other real estate components, such as retail, office, and/or residential. In the majority of cases, developers opt for residential units in one form or another, including timeshare, fractional, or whole ownership. In some cases, developers design residential units into the facilities program in order to make the project appear �more feasible,� or less risky, since there is the potential for immediate returns when the unit sales close. This is obviously not the recommended route of developing a luxury hotel. Over the past few months, we have witnessed several projects that have stalled because of the slowdown in residential sales. And we are all familiar with the fallout from acquisitions whose prices were justified by condo-hotel economics. If not, simply google Robert Falor. Nevertheless, with stand-alone hotel projects becoming harder to pencil out, some developers continue to use residences to enhance return expectations. This is not to say that the project will not work, but this often increases the risk rather than lowering it. If the hotel is not feasible on its own, and the residential sales are not as robust as anticipated, the whole project fails. The following chart clearly illustrates the rise of hotel/residential mixed-use projects. In 2000, of the 61 properties that opened, only two included residential units. In 2008, one out of every three new upscale and luxury hotels includes a residential component. Of the projects slated to open in 2009, roughly 40% will include residential units. UPSCALE & LUXURY HOTEL DEVELOPMENT

Over the past few years, the size of the projects and the ratio of guest rooms to residences have changed. In 2000, the average high-end hotel opened with 306 rooms and 5 residences. In 2008, the typical project has 260 guest rooms and close to 40 residences. The growth in hotel/residential projects has resulted in the co-branding

of the hotel and residential components. Four Seasons, Ritz-

Despite the downturn in the economy and the residential mortgage crisis, the trend toward more hotel/residential mixed-use projects is here to stay. We expect the ratio of standalone hotels and hotel/residential developments to stabilize after 2009 with two of every five projects to incorporate residential components. Partially fueled by the retirement of the baby boomer generation, residences

attached to a hotel or resort will be in high demand over the long-term.

Empty-nesters reducing their home size and moving to the city and retirees

seeking a vacation home will produce new demand in both primary urban and

primary resort locations.

Hospitium is a hotel consulting firm that specializes in the upscale and luxury sectors of the lodging industry. From the early stages of development or deal negotiation through asset disposition, Hospitium delivers timely and useful research, analysis, and insight that assist the various needs of owners, developers, management companies, and financial institutions. Hospitium provides a wide array of advisory services and products, including feasibility studies, market analyses, due diligence, underwriting, strategic planning, development consulting, deal sourcing, and transaction guidance.

Data and information for the Lodging Ledger is collected by Hospitium, LLC. Hospitium, LLC is merely a conduit for the data, and assumes no responsibility or liability for its accuracy, usability, confidentiality, or other matters related to this publication. Information herein is believed to be reliable and has been obtained from sources believed to be reliable, but its accuracy and completeness cannot be guaranteed. Use of the data herein may not be resold, distributed or otherwise utilized for commercial use or profit without the expressed written consent of Hospitium, LLC. |

| Contact:

Hospitium, LLC

|

| Also See: | The Lodging Ledger / Investors Flock to Hotels!!! / The Looming Baby Boomer Impact / Steve Hennis / April 2007 |

| The Lodging Ledger / Skyrocketing Transaction Volume and Pricing / Investment Timing is Key / Steve Hennis / February 2007 | |

| The Lodging Ledger / Hotel Deals Continue to Roll Along, The Allure of Luxury Lodging Assets, The Next Wave of Mega-Resorts / Steve Hennis / October 2006 |

Stephen

Hennis has over fourteen years of experience in the analysis of lodging

investments. He has appraised and evaluated over 500 lodging facilities,

and has been involved in the underwriting, negotiation, and acquisition

of over $400 million in luxury hotels and resorts. Prior to becoming Managing

Director of Hospitium, Mr. Hennis served as Vice President of Hospitality

Investments for Lowe Hospitality Group and Destination Hotels & Resorts

where he was involved with acquisitions, dispositions, and development

projects. Mr. Hennis previously served as Vice President and Director of

Research for HVS International where he specialized in the analysis and

valuation of large portfolios for cross-collateralized securitizations

and oversaw the redevelopment of HVS� analytical models and report templates.

He has also worked for Marriott International and Caesars World. Mr. Hennis

is a graduate of the University of Denver�s School of Hotel, Restaurant

& Tourism Management.

Stephen

Hennis has over fourteen years of experience in the analysis of lodging

investments. He has appraised and evaluated over 500 lodging facilities,

and has been involved in the underwriting, negotiation, and acquisition

of over $400 million in luxury hotels and resorts. Prior to becoming Managing

Director of Hospitium, Mr. Hennis served as Vice President of Hospitality

Investments for Lowe Hospitality Group and Destination Hotels & Resorts

where he was involved with acquisitions, dispositions, and development

projects. Mr. Hennis previously served as Vice President and Director of

Research for HVS International where he specialized in the analysis and

valuation of large portfolios for cross-collateralized securitizations

and oversaw the redevelopment of HVS� analytical models and report templates.

He has also worked for Marriott International and Caesars World. Mr. Hennis

is a graduate of the University of Denver�s School of Hotel, Restaurant

& Tourism Management.