|

News for the Hospitality Executive |

What's Happening to Hotel Cap Rates,

Values and Financing?

.

|

By Jim Butler, Hotel Lawyer | Author of www.HotelLawBlog.com 12 May 2008 Hotel Cap Rates are changing. What are hotel cap rates? What do the changes mean for your hotel buy or sell, hotel financing or refinancing, or next visit from the FDIC? What is the relationship between cap rates and equity return expectations? Suzanne Mellen, Managing Director of HVS' San Francisco office is one of the experts I look to in this area ([email protected]), and she gave us some great information that I want to share with you today. What are Cap Rates? Coincidentally, several blog readers have recently told me a little sheepishly that they sort of know what cap rates are, but could use a little refresher. So here is a one minute review that puts it all in street English (my apologies to the appraisers and financial analysts) and explains why cap rates are so important. And if you want to skip the basic explanation, and get straight to the hot information Suzanne Mellen gave us, just skip to the next section below. First, appraisers and many investors use "cap rates" as one of the benchmarks for determining a hotel property's value -- actually any property's value -- for purchase and sale, evaluating collateral for loan underwriting, or other investment purposes. A "cap rate" is just the rate (expressed as a percentage) of return that a certain set of cash flows represents on the value of an asset. The basic formula for expressing the relationship between Cap Rate, Asset Value and Cash Flow is: (Cap Rate ) x (Asset Value) = Cash Flow For example (A 10% cap rate) applied to (an asset value of $1,000,000) = (Cash Flow of $100,000) At a 10% cap rate a million dollar asset would be expected to produce $100,000 of cash flow But if you remember your basic algebra, you can rearrange the formula to solve for any one of the variables. So here it is in another format: (Asset Value) = (Cash Flow) / (Cap Rate) This means that a $100,000 cash flow implies the following values at the indicated cap rates Cap Rate ....... Value Implied

Thus the implications of the market demanding a higher cap rate on are profound. If cap rates go up, as it appears they have, as a seller of an asset, you will receive a lower price. As a borrower or lender, the value of the collateral goes down. The cash flow may be the same, but the value is reduced when higher cap rates are required. And the final reminder: Cap rates and values move in opposite directions. In other words, as cap rates go up, the value of the asset on the same cash flow go down. As cap rates go down, the value of the asset goes up on the same cash flow. Hotel Cap Rates:

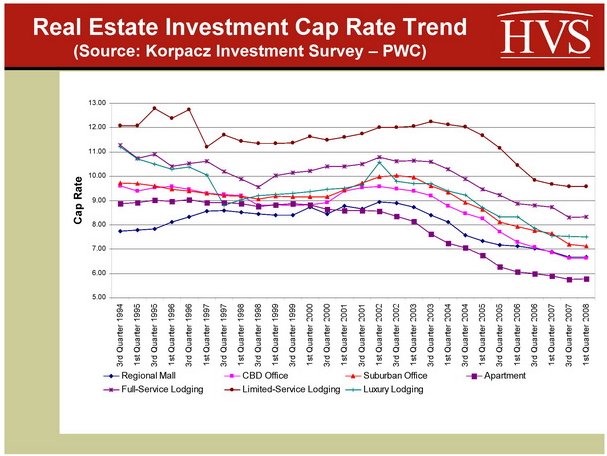

All of the slides included below are courtesy of Suzanne Mellen, MAI, CRE, Managing Director of HVS, and were presented by Suzanne in the Industry Leader's State of the Industry power panel on May 7, 2008. These are also her comments on the slides. A picture is often worth a 1,000 words, and this slide is one of them. It shows cap rates for various asset classes of real estate from 1994 through present. You can see how there has been a significant decline in cap rates and in discount rates since 1994.

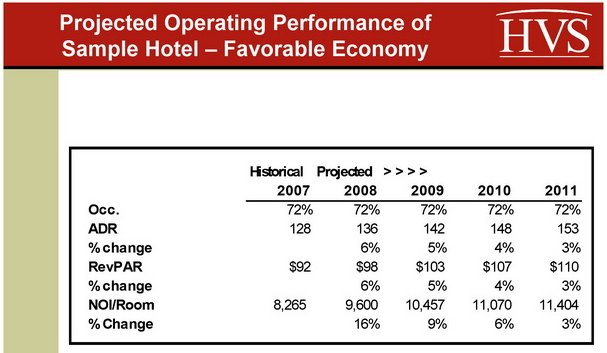

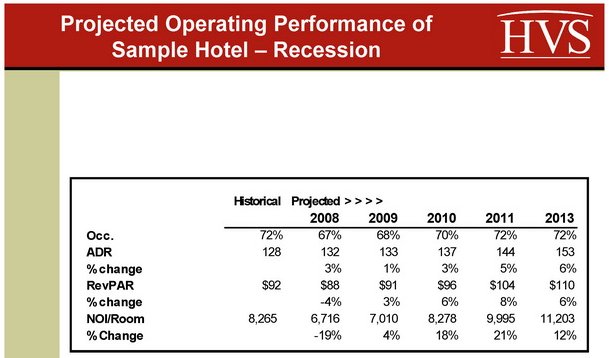

But the factors affecting hotel values, wholly aside from investor demand or supply, are very complex as shown in this series of slides from Suzanne, seeking to show the inter relationship of factors like the credit Crunch, lower LTVs, higher returns demanded by equity, and effects of a recession and recovery. The following slide reflects the performance of a sample hotel as it would have been anticipated before the capital crunch - assuming no recession, and a moderate amount of upside generated by above-inflationary gains in average rate. Note that this case study is of a sample hotel, and should not be taken as a projection or commentary on any single hotel or hotel values at large.

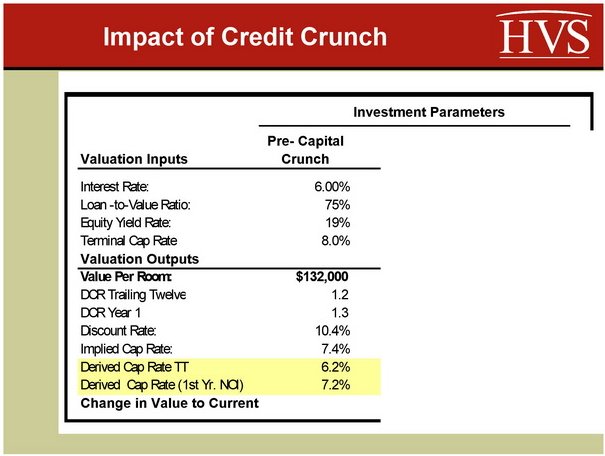

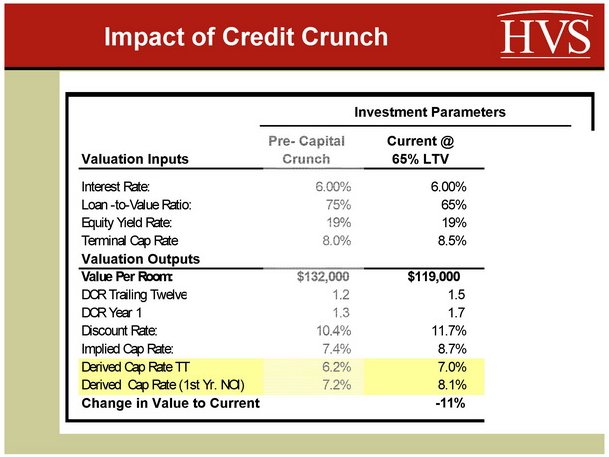

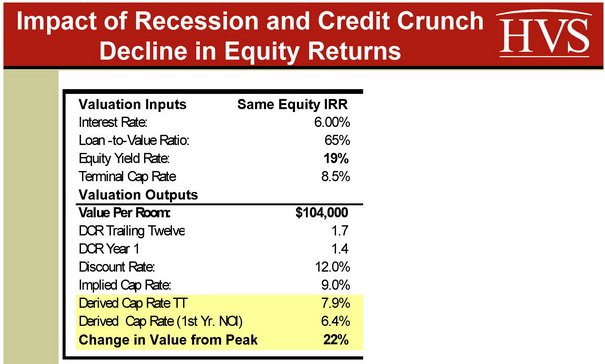

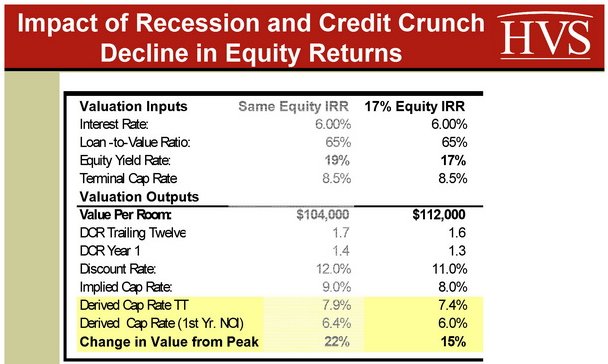

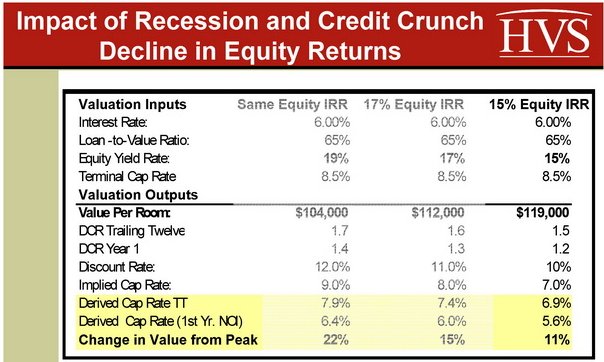

.  Now let's see what the impact on value is from the lower LTVs that we are witnessing today. The same interest rate is assumed, given the recent decline in interest rates and floating rate debt. The equity yield rate is held constant, while the loan-to-value ratio is reduced to 65%. The terminal capitalization rate is increased by 50 basis points to 8.5%; there is a general consensus that terminal rates have increased now that we have moved beyond the stellar investment market of the last few years. .  The reduction in LTV from 75% to 65%, and a 50 basis point increase in the terminal capitalization rate result in an 11% decline in value, all other things being equal. A greater decline in the LTV, from 75% to 60%, and a 100 basis point increase in the terminal capitalization rate, results in an 18% decline in value, as evidenced in the next slide. Note the increase in capitalization rates from 6.2% to 7.4%, based on trailing twelve NOI, and from 7.2% to 8.6% based on first year projected NOI. .  Now let's see what happens to the value of this sample hotel if a downturn in NOI is anticipated due to an economic recession. The following slide sets forth the anticipated change in NOI that is forecast over the next few years, through an economic downturn and a recovery. .  The sample hotel is projected to experience a 5 point occupancy decline and then a three year recovery to pre-recession occupancy levels. Now let's see what happens to the value of this hotel from its pre-capital crunch peak. Assuming the more moderate 65% LTV, the total decline in value resulting from the lower LTV, higher terminal capitalization rate and anticipated decline in NOI due to the recession is 22%. One can see why there is a dearth of transactions, given the specter of a recession and the increased equity that must be raised by investors to consummate a sale. .  No one appears to be supporting the idea of a 22% decline in value, thus, the only variable that can change to close the bid-ask gap is the equity return. Assuming that the equity internal rate of return is reduced to 17%, the change in value is reduced to 15%. Given the general consensus that hotel values have only declined around

5% to 15% from their peak, the equity yield would have to decline to 15%

to compensate for the lower LTVs and anticipated temporary decline in NOI.

Investors with whom we spoke indicated that their equity return requirements

have remained the same or have increased in the current investment environment,

due to the perception of greater risk. Lower LTVs should lower equity return

requirements, given the lower risk of reduced leverage, but it appears

that it may take awhile for investor views (both buyer and seller) to catch

up with the reality of the new investment paradigm.

Jim Butler is a Founding Partner of Jeffer, Mangels, Butler & Marmaro LLP and he is Chairman of the firm's Global Hospitality Group®. If you would like to discuss any hospitality or condo hotel matters, Jim would like to hear from you. Contact him at [email protected] or 310.201.3526. For his views on current industry issues, visit www.HotelLawBlog.com. |

| Contact:

Jim Butler

|

| Also See: | A Crash Course In Cap Rates / Canadian Lodging Outlook - January 2005 Year-to-Date |

| (Cap)Rating Perceptions of Risk / Patrick Quek / PKF / June 1998 |

|

|