|

|

News for the Hospitality Executive |

|

Select-service Hotels Financial Performance

| By Robert Mandelbaum and Steven Nicholas CHA, June 2008

The great investment return that the limited-service segment can provide is probably the worst kept secret in the hospitality business. Gone are the days that any hospitality professional will say, �No one will stay at a hotel without all the bells and whistles of a full-service hotel.� Industry segmentation nomenclature has always been somewhat vague, but over the last few years it has become downright muddy. We have gone from limited-, to select-, to focused-, to the next TBD variation. However, today, most industry participants use the term select-service to define properties that offer either no, or a limited degree, of food and beverage (F&B) service. Typically, these properties are priced in the middle to upper-middle tiers within their respective markets. Most general accepted select-service brands reside in the Midscale without F&B and Upscale chain-scale categories as defined by Smith Travel Research. However, with the continual growth of amenities and services offered at these hotels, the select-service segment is populated with limited-service, full-service, all-suite, and extended-stay properties. The reason for the market appeal of the select-service properties among consumers, brands, and investors is quite obvious by looking at historical market penetration data. Since 1988, the Midscale without F&B and Upscale chain-scale segments combined have achieved a 6.8 percent occupancy premium over the industry wide average for all U.S. hotels. The only thing that seems to change faster than the name of the segment is the services that are provided in the segment. The continual upgrade of services at select-service hotels can be looked at as an �amenity sprint.� Has the continued product differentiation produced positive investment returns? Has this premium market performance transferred from the top-line to the bottom-line? To answer these questions, we have examined data from the Trends in the Hotel Industry database of PKF Hospitality Research. The 2006 financial statements from two groups of select-service hotels were analyzed. One group consisted of select-service properties that offer some-degree of retail food and beverage service (i.e. Hilton Garden Inn, Marriott Courtyard). The second group consisted of properties that either offer just complimentary food and beverages, or no F&B service at all (i.e. SpringHill Suites, Hampton Inn). To provide a comparable comparison, the two groups were selected to be similar in room count (144 rooms) and occupancy (71.3 percent). Select Revenues

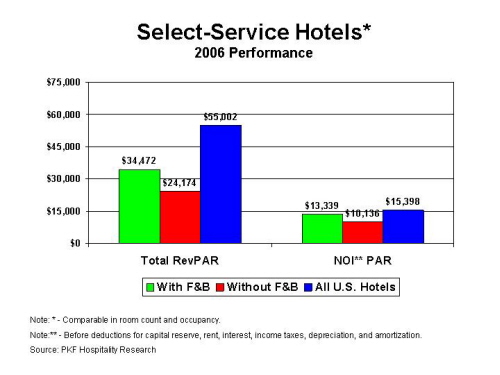

The 32 percent average daily rate (ADR) premium realized by the full-service sample was the main reason for the $10,298 PAR difference in total revenues between the two select-service groups. In 2006, the select-service hotels with F&B achieved an ADR of $118.74, while the properties without F&B averaged $89.93. These numbers clearly illustrate that the customer is willing to pay a premium for the upgraded services that have been added to properties within the select-service segment over the last few years. Also contributing to the total revenue disparity was the $2,773 PAR in food and beverage revenue earned by the full-service properties. For select-service hotels with restaurants and lounges, food and beverage revenue average just 8.0 percent of revenue. For all hotels in the Trends database, food and beverage revenues represent 26.7 percent of total revenue. The revenues produced in the food and beverage department of select-service hotels are not the driver of the investment, but used as an amenity. Select Expenses

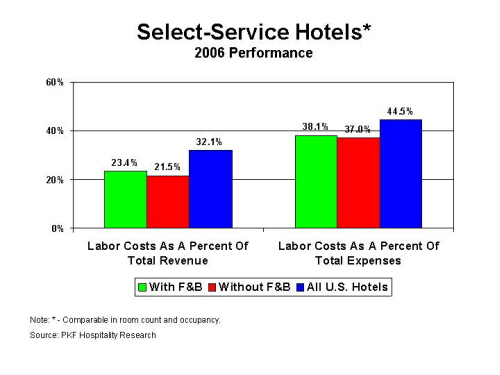

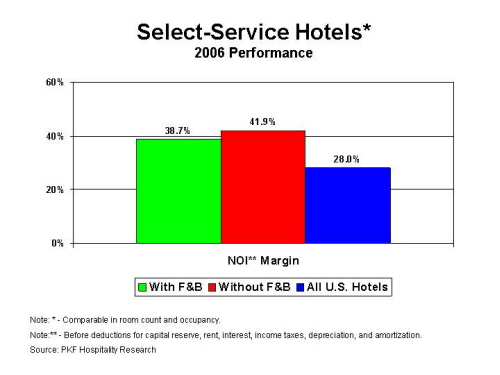

For the typical U.S. hotel, labor costs averaged 32.1 percent of revenue and 44.5 percent of expenses in 2006. In the select-service segment, these ratios are much lower. In 2006, labor costs at select-service properties with F&B averaged just 23.4 percent of revenue and 38.1 percent of expenses. For select-service hotels without F&B, the ratios are even lower. Labor costs at these properties averaged 21.5 percent of revenue and 37.0 percent of expenses. While limited labor costs help the select-service properties achieve a high operated department profit margin, the lower revenue levels make the overhead expenses stand out to a greater degree. In 2006, undistributed expenses averaged 26.6 percent of total revenue for the select-service sample. This is slightly greater than the 24.2 percent average for all hotels in the Trends database.  Perhaps the greatest appeal of select-service hotels for owners and developers are the high profit margins that lead to very high Internal Rates of Return. In 2006, the select-service hotels with F&B earned a 38.7 percent profit margin, while the properties without F&B achieved an even stronger 41.9 percent ratio. These statistics compare favorably to the 28.0 percent profit margin achieved by all hotels in the Trends sample. For the purposes of this analysis, profit is calculated before deductions for capital reserve, rent, interest, income taxes, depreciation, and amortization. The bottom-line of the select-service with F&B sample did benefit from $524 PAR in profit generated by their restaurants and lounges. However, it should be noted that the F&B department profit margin for these properties was just 18.9 percent, compared to a 27.7 percent average department margin for all full-service hotels. This low F&B department profit margin gives further credence to the fact that the purpose of adding food and beverage to select-service properties is really to drive room revenue and room profits. While select-service profit margins are greater than the industry average, the lower revenue levels discussed earlier result in relatively low bottom-line dollars. In 2006, the select-service with F&B sample averaged $13,339 PAR in profits, while the sample without F&B earned $10,136 PAR. Overall, all the hotels in the Trends sample averaged a profit of $15,398. Due to the lack of amenities and service offered by select-service hotels, the development costs for these hotels are typically low when compared to traditional full-service properties. Therefore, while select-service profits range from 15 to 52 percent less than the industry-wide averages, a similar comparison needs to be made of development costs in order for an owner to help determine the viability of a select-service investment.

The concept of not �nickel and dimeing� the customer, and therefore delivering a high degree of perceived value, is the very foundation of the select-service segment. This is the reason why these properties have a history of operating non-revenue generating departments. Examples of the complimentary services offered at select-service properties include free continental breakfast, free local phone calls, and now, free high speed internet access. Customer expectations and brand requirements continue to drive the number and cost of complimentary services offered at select-service hotels. Over the last few years, the increased cost of offering these complimentary amenities has been more than offset by RevPAR increases. Going forward, if RevPAR increases begin to flatten, it will be more difficult for select-service properties to continue to step up these services at the pace that has occurred over the last few years. Robert Mandelbaum is the Director of Research Information Services for PKF Hospitality Research. He is located in the firm�s Atlanta office. Steven Nicholas CHA is Principal and Executive Vice President, Asset Management for the Noble Investment Group. Steven works in the Atlanta headquarters of Noble. This article was published in the May 2008 issue of Lodging. |

| Contact:

Robert Mandelbaum

|

|

|