|

News for the Hospitality Executive |

Construction Pipeline in Europe at New Cyclical High;

Hotel Openings in 2008 to Set Record Pace

.

| Portsmouth, N.H. � October 16, 2007 - Lodging Econometrics

(LE), the Global Authority for Hotel Real Estate, reported to the Lodging

Industry that there are a total of 814 hotels having 139,133 rooms in the

Construction Pipeline throughout Europe.

LE President Patrick Ford said, �Hotel Construction is at a robust pace. Half the Pipeline, 407 projects / 72,205 rooms, are already Under Construction. That means that a record 292 hotels / 45,598 rooms are set to open throughout the region in 2008. �In light of the prosperous economic conditions throughout Europe, the timing of this construction spurt is ideal,� said Ford. �In particular, the region�s capital cities have been experiencing robust hotel occupancies, and many have enjoyed double-digit year-over-year room rate increases in 2006 and again in 2007, strong indicators of a shortage of guestrooms in many markets.� Lodging Construction is Led by Largest European Economies The United Kingdom has the largest Pipeline in the region by far, some

two and a half times greater than Spain, which is in second place.

Of the U.K.�s 277 projects / 40,441 rooms, nearly a third of the rooms

are in London, which is experiencing its best operating performance since

the late 90�s.

While projects in most markets are planned to open near the top of the present economic cycle in 2008 � 2009, the Construction Pipeline in the U.K. is expected to continue to expand and unfold at a growing pace well into the next decade. London is the key travel market and generates a spillover effect for many other areas. It enjoys one of the highest occupancies and room rate levels in Europe. Lodging demand is burgeoning. London is a rapidly growing international financial center with a booming office and residential market. It benefits from a rising flow of travelers from China, India, the Middle East, and Eastern Europe. A new transportation hub at St. Pancras Station, scheduled to open soon, and another terminal at Heathrow Airport in 2008 will boost travel further. Both planned hotel development and traveling are even further amplified by the building and preparation for the Olympic Games scheduled for 2012. Russia, based on GDP growth, is one of the fastest growing economies in the region, and has an escalating pipeline as well. Buoyed by its oil and gas development, 31 of Russia�s 45 planned hotels are located in Moscow and St. Petersburg, which together account for 77% of all guestrooms under development. Projects in both cities are large, iconic, and will carry four- and five-star international brands. Another five European countries have between 15-30 projects each in the Pipeline, led by Portugal, Austria, Turkey, the Netherlands and the Czech Republic. All are smaller countries, but with Pipelines measured as a percentage of their existing Census of Open and Operating Hotels, they have impressive Pipelines indeed. Following London, there are another 14 major European cities with between 10-20 each planned projects in the Pipeline. Most of the countries and cities have around 50% of their projects already Under Construction, with New Hotel Openings scheduled to peak in 2008 - 2009. International Hotel Companies Are Active in Gateway and Secondary Cities For years, the major international lodging companies have concentrated

on expanding their four- and five-star marquis brands in Europe�s gateway

cities. Their Construction Pipelines continue to unfold.

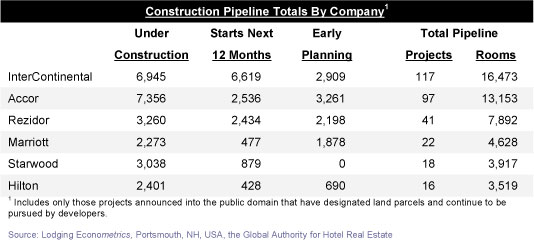

However, the companies with the largest Pipelines today, having the best opportunity to capture the greatest market share across the continent, are those that have chosen to deploy a full roster of upscale and mid-market brands in suburban locations and secondary cities throughout the region. These smaller projects are ideal growth vehicles for gaining market penetration and capturing market share rapidly. Timelines from project inception to opening are far shorter. Land costs are less expensive, permitting is easier, and construction costs are less. To accelerate mid-market development, the international brands often seek experienced financial and/or development partners who will commit to develop a large roster of projects in certain areas and within a specific time period, most often with the brand managing the properties. Brands with a long-time European presence have the largest Construction Pipelines today. InterContinental has 64 Express by Holiday Inns and 25 Holiday Inns being actively pursued by developers. Accor has 41 IBIS and 24 Etaps; and Rezidor has 17 Park Inns. Marriott�s strong Pipeline includes 11 Courtyards, but the company has four other upscale and mid-market brand offerings in the U.S. that they have not yet decided to deploy internationally. Other companies also have impressive brand distribution plans rolling out. When the Hilton Corporation merged with Hilton International, they inherited an international roster of full-service Open and Operating Hilton Hotels and an impressive Pipeline of projects under development. A significant opportunity driving the merger was the launching of Hilton�s entire family of upscale and mid-market brands across the globe: Doubletree, Hilton Garden Inn, Hampton Inn, and Homewood Suites. Newly formed development teams are in place in London and in Singapore to accomplish just that. A number of joint ventures have already been announced to accelerate the launch of these brands. For newly created brands, Starwood Hotels has begun their international rollout of aloft. Earlier, InterContinental introduced Staybridge Suites, and Hotel Indigo, their new contemporary upscale brand, is following. The high number of projects already Under Construction and the Forecast for New Hotel Openings scheduled for 2008 and 2009 all seem fortuitously timed. Recent credit restrictions will understandably make it a bit more difficult for those developers who have yet to obtain financing. A period of more selective credit granting that is likely to extend Pipeline timelines is upon us. The impact on the existing Pipeline will be a modestly higher-than-normal flow of project delays, and perhaps cancellations for some of the more marginal projects. If financing is attained, it�s likely to take longer, be at higher rates and require more of a cash infusion by the investors. That may well cause a second look at some proposed projects� feasibility, particularly if there is any forthcoming fall-off in guestroom demand associated with slowing economies. Offsetting project counts and timeline adjustments to the current Pipeline

is an expected heavy flow of newly announced branded upscale and mid-market

projects into the Pipeline. Europe is one of the most promising regions

in the world for those international companies looking to widely deploy

a full family of brands.

|

| Contact:

Lodging Econometrics (LE)

|

| Also See: | Hotel Construction in the Asia-Pacific Region Is at a Record Level; A Burgeoning Pipeline in China Is Set to Unfold / October 2007 |

|

|