|

|

News for the Hospitality Executive |

|

Extended Competition Leads to Extended Recovery

.

An Analysis of the Extended-stay Lodging Segment

.

| by: Robert Mandelbaum, December 2007

An analysis of supply change within the extended-stay lodging segment certainly illustrates the appeal of this property type among hotel developers. According to Smith Travel Research, the overall industry has averaged annual changes in supply of 0.9 percent from 2000 to 2006, while the number of new extended-stay rooms has been growing at a 5.1 percent annual pace. The reasons for this attraction are many. Historically, this segment has achieved occupancy premiums and high profit margins. In addition, consumer acceptance has been high, and they are relatively easy operations to manage. Unfortunately, all this growth in inventory has had an impact on unit-level performance. Extended-stay hotels that have been in operation throughout the recent surge in new supply (2000 to 2006) have experienced a lag in revenue and profit growth. Once again, unit-level performance statistics tell a different story than industry-wide data. These observations come from an analysis of unit-level performance data

taken from PKF Hospitality Research�s Trends in the Hotel Industry database.

The analytical sample consists of 200 extended-stay hotels that reported

full financial data each-year for the period 2000 through 2006. The

sample was divided into two categories; upper-tier (i.e. Residence Inn,

Homewood Suites, Staybridge Suites), and lower-tier (i.e. Extended-Stay

America, TownPlace Suites, InTown Suites).

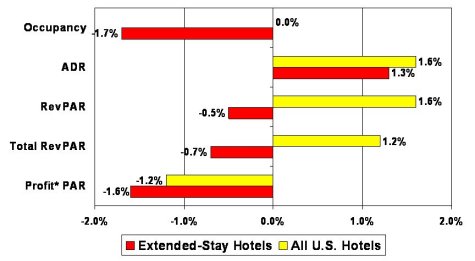

Compound Annual Change � 2000 to 2006

Note: * Before deductions for capital reserve, rent, interest, income taxes, amortization, and depreciation. Source: PKF Hospitality Research Lag In Revenues Because new development activity has outpaced the increase in demand for extended-stay facilities, we have observed a net decline in the average unit-level occupancy since 2000. From 2000 to 2006, there has been a compound annual decline in occupancy of 1.7 percent for our extended-stay sample. It is important to note that despite the lag in annual occupancy change, the extended-stay properties in our sample still achieved a strong 69.9 percent occupancy level in 2006. This fall off in extended-stay occupancy from 2000 to 2006 is the main catalyst behind the decline in total revenue during the same period. From 2000 to 2006, total revenue for the typical lodging property in the U.S. grew at a compound annual rate of 1.2 percent. Concurrently, the typical extended-stay hotel has yet to return to its 2000 revenue level. The compound annual change in unit-level extended-stay revenues was negative 0.7 percent from 2000 to 2006. High Profit Margins Like revenues, the change in extended-stay unit-level profits has also lagged behind the industry wide average. At the bottom-line, unit-level hotel profits had yet to reach their 2000 levels by year-end 2006. The compound annual change in operating profits for the overall U.S. lodging industry was negative 1.2 percent from 2000 to 2006, while the extended-stay sector suffered a greater average annual decline of 1.6 percent. Fortunately, extended-stay hotels are extremely efficient operations

and achieve very high profit margins. The typical extended-stay hotel

earned a 47.7 percent profit margin in 2006. This compares to an

industry wide average of 28.0 percent. Within the extended-stay segment,

the upper-tier properties achieved a profit margin of 35.2 percent, while

the lower-tier properties dropped a tremendous 53.5 percent of their revenue

to the bottom-line.

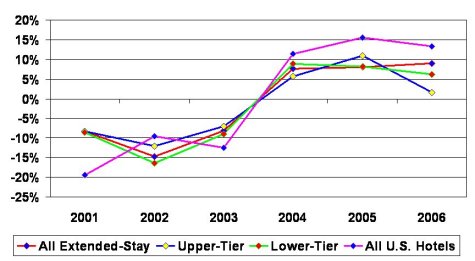

Annual Change in Net Operating Income*

Note: * Before deductions for capital reserve, rent, interest, income taxes, amortization, and depreciation. Source: PKF Hospitality Research Less Volatile While the lag is revenue and profit growth may be disturbing, developers

with a low tolerance for risk within the U.S. lodging industry might find

the extended-stay segment very attractive. Extended-stay financial

performance has proven to be less volatile than the U.S. lodging industry

as a whole. During the 2001 to 2003 industry recession, the extended-stay

segment was somewhat insulated and experienced lower declines in revenues

and profits. However, when the overall industry was reveling in double-digit

gains in revenues and profits during the 2004 to 2006 recovery, the extended-stay

segment experienced more modest single-digit annual growth rates.

Enhancing the inherent financial stability is the fact that extended-stay

hotels typically achieve occupancy and profit margin premiums compared

to other hotel categories.

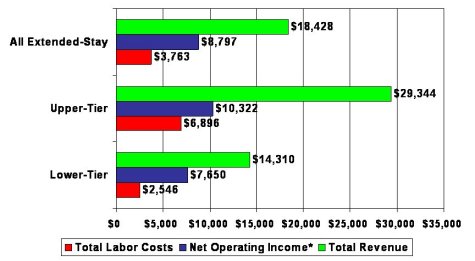

Comparative Performance Dollars Per Available Room

Note: * Before deductions for capital reserve, rent, interest, income taxes, amortization, and depreciation. Source: PKF Hospitality Research Limited Personnel The primary reason for the strong profit margins within the extended-stay segment is the low level of payroll costs. In 2006, the industry wide average for the combined costs of salaries, wages, and benefits was 32.1 percent. For upper-tier extended-stay properties, this ratio was 23.8 percent, while the lower-tier sector kept labor costs to just 17.8 percent of revenue. Because of the extended length of stay within this segment, there are fewer check-ins and check-outs. This requires minimal levels of front desk, laundry, and housekeeping staffing. In addition, some upper-tier and most lower-tier extended-stay properties perform a complete cleaning of their guest rooms just once a week during a typical stay. Further minimizing unit-level labor costs are the limited staffing requirements within the sales department. Extended-stay business is often sold on a contractual basis to companies. These contracts are frequently generated by personnel within national and regional franchise sales departments. Length Matters To maintain the superior levels of occupancy and profit margins, extended-stay hotels must maintain a high percentage of extended-stay business. While transient stays of a shorter duration often come with a higher average daily room rate, these occupied rooms require more service (i.e. laundry, room cleaning, front desk) and thus increase operating costs. Looking forward, PKF Hospitality Research is forecasting a protracted period of extended performance at the peak of the current industry cycle. Overall industry annual growth rates in revenues and profits for the next two to three years will not be as great as they were during the 2004 through 2006 recovery, but will remain above their respective long-term averages. In turn, the stability of the overall lodging market should perpetuate the historical stability of extended-stay revenues and profits that we have observed in our analysis. Robert Mandelbaum is the Director of Research Information Services for PKF Hospitality Research (www.pkfc.com). He is located in the firm�s Atlanta office. This article was published in the November 2007 edition of Lodging magazine. |

| Contact:

Robert Mandelbaum

|

|

|