![]()

advertisement

.

|

|

![]()

advertisement

.

.

Top Ten Issues in the Hospitality Industry for 2007

-

International Society of Hospitality Consultants

.

| November 2006 - At the recent ISHC Annual Conference held in Miami,

Florida, ISHC members participated in a series of roundtable discussions

to identify the ISHC Top Ten Issues in the Hospitality Industry for 2007.

This year the debate included in-depth discussions on over 100 different issues with 27 making the ballot for the final vote by the members. Ultimately, the following Top Ten Issues were identified as ones that can be expected to potentially have the greatest impact on the industry in 2007. Hospitality Industry for 2007

#1 ISHC Top Ten Issue

The problem of attracting and retaining qualified workers, once an issue

only in an isolated number of markets, is increasingly becoming a global

challenge.. Demography, wage levels, failure to adequately address

Why can�t we find good people? It�s become a global concern, the number one issue confronting our industry. Here are some of the causes: Demographics � Population growth rates have been slowing in Europe, the U.S. and elsewhere for decades so the number of workers leaving the workforce now exceeds those that are entering. The aging workforce moving into retirement is creating a huge void that can only be expected to grow larger going forward.What can we do about it? As an industry, we need to work together to develop strategies for rethinking and rehabilitating our industry�s image as an exciting and rewarding career choice. There was a time not too long ago when people joined the hospitality industry for its glamour. Globally, we need to share best practices for training and retention and make industry sponsored educational programs more readily available to employees at every organizational level. Industry organizations including the International Hotel and Restaurant Association and the American Hotel and Lodging Association Educational Institute provide excellent training libraries as well as web based training programs. Additionally, there are some outstanding independent firms that specialize in human resource training and development�some of which also offer excellent proprietary training materials. Meanwhile, following are some thoughts to share regarding potential opportunities for hotels to meet the labor challenge? Grow Your Own. Hotel companies need to develop internal programs to create attractive career paths so that potential candidates see employment as a professional development opportunity with real potential for advancement. Recruiting for entry level positions is easier when the recruiter can outline a career path and can point to managers who have worked their way up from line positions. Marriott has been doing this better than anyone for decades.In today�s environment, operators are increasingly finding they must compete for workers as hard as they compete for customers. Developing a positive work environment with real opportunities for advancement, combined with creative strategies for recruiting and improving employee productivity will all be increasingly essential skills as the workforce continues to shrink in the foreseeable future. # 2 ISHC Top Ten Issue

All construction costs and the costs for furnishings, fixtures and equipment (FF&E) will continue to escalate in 2007, although at a pace a little slower than experienced in the period from 2004 through 2006. According to the Associated General Contractors of America, construction costs, driven primarily by materials costs, spiked dramatically in 2004. The annual increase for construction materials in general was approximately 10 percent in 2004, followed by 6.0- percent and 8.8-percent increases in 2005 and 2006, respectively. This compares to increases of 3.8 percent in the consumer price index and 3.7 percent in the producer price index for the period from August 2005 to August 2006. In 2004 and 2005, these two latter indices experienced annual increases averaging about 4.0 percent. The outlook for the future is for more of the same, although at a somewhat slower pace. For example, steel prices experienced a 48.8-percent increase in 2004, which was preceded by significant increases in scrap iron and steel prices in 2002 and 2003. Steel prices held steady in 2005 but jumped again in 2006. They are expected to increase again in 2007 and beyond as demand for steel from construction projects in China and India increases. Scrap iron and steel prices have increased approximately 20 percent in the past twelve months. Other important factors contributing to the increases in construction costs include the cost of diesel fuel used for transportation of both raw and finished goods. Some relief has occurred recently, with fuel costs dropping in tandem with crude oil prices have dropped. But uncertainties of supply in crude oil markets and the somewhat tenuous situation in OPEC nations both economically and politically indicate continuing volatility in future pricing. Further, winter temperatures in 2006-07 could alter the balance between diesel and heating oil production, causing a price escalation in one or both of these fuels. Concrete prices are expected to continue to increase spurred by the ongoing increases in cement, aggregate and the fuel necessary to mine or extract these components. The recent downturn in the residential construction industry may moderate concrete price increases, but the impact of ongoing construction in China and India may more than offset these influences. The anticipated increase in the number of hotels currently in the development pipeline will certainly be affected by construction cost increases. Clearly, rising costs will have an impact on budgeting for new development or renovation projects. Construction contractors, particularly smaller ones, may not be able to offer guaranteed-maximum construction contracts, because they may not have the purchasing power to secure materials at favorable or fixed prices. Even the larger contractors are likely to hedge their contract quotes with provisions that shift the risk of increasing materials costs to the developer. This will affect every aspect of a construction project, particularly the scheduling of sub-contractors and deliveries of materials. Developers will be eager to adhere to a tight project schedule, while contractors will often be at the mercy of the materials suppliers as well as the availability of materials themselves. Faced with this situation, what can a developer or owner do to protect its interests? The following strategies may provide some ideas for further consideration and even innovation:

# 3 ISHC Top Ten Issue

Despite a growing awareness of the value of modern, integrated systems, many properties still do not take advantage of them as fully as they might to maximize revenue opportunities. Many also fail to support and secure them to the extent appropriate to the value of their data and to the legal consequences of that data becoming stolen or corrupted. A significant factor restricting wider adoption is the challenge of improving the systems� ease of use as they continue to grow in functionality, in both operational and guest-facing areas. All of these issues support a trend to outsourcing the more complex operational functions and system security to expert, central staff, either corporate or third party. The major factors involved are:

However, many properties handicap themselves through hanging on to systems well past their competitively useful life, greatly restricting their ability to implement such revenue-enhancing measures as taking Internet reservations, performing effective rate/revenue management, collecting more detailed guest data for customer relationship management and targeted marketing, and so on. Sometimes this comes from a lack of appreciation of their potential upside, but there is also often apprehension about the difficulty of integrating older but still valuable systems into a more modern, integrated whole. Current interface technologies go a long way to alleviating this issue, but many properties have found that the benefits from replacing valued older systems with a more comprehensive, integrated system outweigh the possible loss of some minor functionality. Another factor discouraging upgrades is that the more comprehensive systems can seem challenging to use. Certainly good user interface design, as much an art as a science, is something vendors continue to pursue through better data layouts, property-specific screen customizations, the subtle use of color and differing fonts to guide users through the logical sequence of operations, and so on. This is likely to be a continuing challenge in both guest and operations technology. Check-in kiosks and guestroom technology, for example, must be as intuitive to use as possible, for a wide range of guest ages and technical familiarity. Nevertheless, as far as hotel-management systems are concerned the disadvantages of an unintuitive user interface can be overcome through user training, yet many hotels handicap their users by not providing refresher training on at least an annual basis. In an industry with traditionally high staff turnover this virtually guarantees that the systems won�t be used effectively, hindering the property from realizing the full return on its investment and maximizing its revenue. Further, as systems become more comprehensive and wide-ranging their support and security management become both more complex and more essential. Loss of access to the system through hardware, software or network failure is completely disruptive since equivalent manual procedures are now virtually impossible to implement quickly. It is very difficult for an individual property to afford in-house technical support personnel trained in all the systems it uses, yet many properties do not have support agreements with third party vendors that might pro-actively prevent imminent problems. More importantly, guest profile data is becoming an increasingly attractive target for identity theft, and attacks on computer systems containing it are becoming more focused and more sophisticated. In addition, legislation such as Sarbanes-Oxley holds corporate officers personally accountable for the accuracy of their financial data. Despite these factors, many systems do not provide audit trails of which user changed key configuration parameters. Further, although all systems track the user ID responsible for changes to guest data, many hotels fail to enforce control over the sharing of IDs and passwords among users, making it impossible to know who entered or modified specific data � or sometimes even just who�s signed on to the network. All of these factors encourage the movement towards more professional systems management; either from a corporate resource team shared among many properties or contracted out to a professional third party. Centralized revenue management teams, for example, can provide expert help to multiple properties in a regionally cohesive way. Centrally-hosted systems allow for highly-qualified technicians to provide a far more secure and managed systems environment than would be available to an individual property. This trend is expected to continue as awareness grows of the value of keeping systems operating at peak efficiency, and of the potential damage from security breaches. # 4 ISHC Top Ten Issue

The impact of changing demographics on travel trends is a so far reaching no sector in travel, tourism and hospitality remains unaffected. Whether the subject is the gradual retirement of baby boomers, rampant globalization and its impact on business travel, or the increased demand for experiential travel, the dramatic worldwide shift in demographics poses both challenges and opportunities. These recent and ongoing changes in the demographic environment hold major implications for the hospitality industry in particular. With regard to product and service offerings, hoteliers need to begin a strategy that addresses multi-generational needs, wants and desires. Now, more than ever, hoteliers must offer design and amenities that cater to the special needs of aging consumers (Baby Boomers), as well as younger travelers (Gen-X and Gen-Y), who have high expectations in regard to design and technology. The traditional practice of brand standardization flies in the face of this. Hoteliers must adapt and look for ways to enhance all guest experiences regardless of generation. On January 1, 2006 the first of America�s seventy-eight million baby boomers turned sixty-years old, while the last one turned forty. In fact, nearly 8,000 boomers are turning sixty on a daily basis, and according to US Census Bureau statistics, the number of boomers expected to be living in the year 2030 is 57.8 million. This is the year boomers will be between ages 66 and 84. What does this milestone mean for hoteliers? It means changing the way we have traditionally connected with the so-called �senior� market. Primarily because boomers will not �grow old� quietly as previous generations have. This is the generation that has, and will continue to redefine the traditional ideas of aging. Boomers will be more active in their retirement, firmly believing that 50s and 60s are now middle age. This is primarily due to longer life expectancies and significant improvements to overall health and well-being. Although boomers will continue to be important in both population and economical terms, the younger markets (the 49 million Gen X'ers and 72 million Gen Y set) are now coming into their own, entering middle management positions, stepping into political offices, and assuming their rightful positions of influence and affluence. It is important for hoteliers to bring the generations together and begin to serve their different habits, patterns and needs. The successful model for true solutions will require long lead times, but here are some suggested approaches.

# 5 ISHC Top Ten Issue

We can anticipate that it will become increasingly difficult to sustain profit growth and improved return on investment performance. And for several reasons including:1) increasing operating costs that will outpace the growth of Revenues Per Available Room (RevPAR). 2) the rising costs of capital and the need for reinvestment that will adversely affect hotel returns. 3) Increasing labor and benefits costs that are being driven by changes in demographics, government regulations and labor agreements, and 4) higher energy costs. In the US for example, according to Smith Travel Research, RevPAR growth has been robust over the last three years reaching a projected peak in 2006 at 8.9 percent. While there is some debate about exactly where the industry is in the current cycle, there appears to be a consensus that RevPAR growth has peaked. For 2007 Smith Travel Research is projecting growth of 7.1 percent, and with the threat of increased supply looming on the horizon, year over year RevPAR growth is expected to continue to decline. Rising interest rates and higher equity return requirements are anticipated to result in higher costs of capital. At the same time, reinvestment costs (capital expenditures) are increasing as existing supply ages. As a consequence, profits will be reduced and owner returns are expected to decline over the next 12 to 24 months. Labor costs are the number one factor impacting hotel expenses. They are being affected by:

In some cases, the factors that have been identified as affecting hotel profitability are out of the control of individual hotel owners and operators, however, there are steps that can be taken to mitigate their impact. For example: by giving increased attention to yield management, operators can potentially increase their RevPAR; through creative financing and diligent oversight of capital expenditures operators can increase their return on investment; improved employee retention and the use of alternate labor sources such as retirees can help to contain employee labor costs; and the installation of new energy saving devices and more efficient design can help to control energy expense. # 6 ISHC Top Ten Issue

As most of us involved in hotel development and operations are aware, there has been an explosion of new hotel brands/products announced over the past three to four years. Aloft, Cambria, Indigo, Waldorf-Astoria, Hyatt Place, NYLO, Viceroy, Capella, and most recently �1�, are but a few examples of this rabid expansion of product type among both the major hotel franchise companies and small start-ups or spin-off management firms trying to establish themselves as a brand. But, despite all the hype and promotion surrounding the roll-out of these new hotels products, and the promise that each will be �unique� and �different� from their existing or future competition through design, price point, service levels, amenities, and/or the mattress, do the vast majority of consumers really understand all of the products? Do they want them? And what about the existing hotel franchisee or owner faced with yet another brand competitor under an existing franchise umbrella that is first viewed as splitting the pie even further? What does it do to their demand base? How about the �going concern� value of their asset? Today, there are an estimated 140 + hotel �brands,� up from approximately 80 in 1995 and estimated 110 brands in 2000. Are all these brands and choices necessary? Are more brands better, or are we merely creating more confusion for an already confused customer base? The answer is probably yes and yes, but not necessarily negative. Much of the new product being launched is attempting to capture an evolving consumer whose tastes and preferences are changing as they age. The baby boom generation, Gen Xers and Y'ers, Millenniums, etc., all have demographic characteristics and psychographic needs that may or may not be satisfied by today�s hotel products. So the idea is that these new brands and products will better meet these consumer�s evolving needs in sufficient quantity to be market and financially successful. In that light, the larger issue is what to do with the brands left behind. They never seem to go away! Perhaps that�s where more thought and effort should be concentrated by industry consultants, investors and franchisors. On the other hand, in the case of start-up hotel companies such as, Kor, West Paces Hotel Group, which rolled out the Solis and Capella luxury brands under the leadership of a former Ritz Carlton executive, or most recently the �1� luxury brand, begs the question as to whether there is perhaps too much equity and debt capital chasing too few deals in a hot hotel market rather than a verifiable market need for a better mouse trap. From an existing hotel franchisee/operator perspective, how do the major franchise companies protect their existing franchise partners from the impact against these new products so that the new product is not cannibalizing the existing demand base, particularly when there are 10 to 15 years left on the existing operator�s franchise agreement? This is an on-going issue that continues to surface, but has yet to be resolved between franchisor and franchisee. Franchisee councils, 3rd party impact studies, and areas of protection are a few of the methods used to address this complex issue, but none have proven to be a panacea. In both cases, the onslaught of new brands is a cyclical one and tends to occur during the up and peak points of the hotel cycle. So it is likely that this proliferation will subside as the industry cycle matures or begins to decline. At that point, as we have seen too often, the new brands that were ill-conceived and lacking clear definition and marketability ultimately become the weaker performers which are then often �absorbed� by the stronger ones. Eventually, these same brands (and all the hotels bearing their name) that fail to capture sufficient consumer interest languish and trade down the food chain of franchise companies over time, or are broken up and sold off in pieces. These thoughts would suggest that, perhaps as an industry, we should focus more on creative alternative uses for marginal brands and properties as opposed to worrying about the new ones stealing existing business. # 7 ISHC Top Ten Issue

In 2006, it is estimated that $24 billion worth of hotel rooms in the US alone will be booked through internet sites representing 27% of US hotel industry room revenues --- up from $15.5 billion just two years ago. Moreover, industry analysts estimate an additional 25 to 30% of all hotel bookings are influenced by online research. The bottom line is that the hospitality industry continues to experience a revolution in distribution, and organizations are less and less equipped to keep pace with the dramatic changes in this online �landscape�. As distribution via the Internet evolved many experts agreed that online presence helped �level the playing field�; that independent hotels and small hotel companies could compete in cyberspace with major brands. Today, the issue is not �can they compete� but can any hotel or hotel company keep pace with the colossal changes and innovations that flood the online world? At the property level the first challenge was to effectively (and more efficiently) manage a myriad of distribution channels from a tactical perspective. Certainly the efforts to do a better job at the tactical side of distribution management have paid off. Although there�s still room for improvement in this regard, online inventory management and better application of rate integrity policies have certainly helped hotels �take back control� of their inventories and pricing. The newest challenge is represented in the strategic side of distribution management and more specifically the ability to understand, manage and market to the consumer in the online world. This playing field is changing so rapidly that it is virtually impossible to keep pace. Hospitality professionals, whether they be in ownership positions, senior management at corporate or a property level executive, must become �online savvy�. Without some understanding of the online consumer�s buying behavior, it is impossible to effectively �level the playing field� or allocate marketing dollars intelligently. From travel blogs to consumer reviews � from travel oriented social networking to highly targeted, email based direct marketing � from �really simple syndication� (RSS � permits users to subscribe to their choice of Web content) to the use of rich media to differentiate hotel product�all of these innovations are causing what PhocusWright terms �the power shift toward consumers�. The question is: �Are hotels ready for this�? In many cases our �collective heads� are still spinning from the first wave of online distribution challenges. Now hotels must be even savvier about every aspect of how their product reaches the consumer. Directors of Sales & Marketing and Directors of Revenue Management must understand at least the basics of search engine optimization, pay-per-click marketing, link popularity strategies and web traffic analysis. Allocation of marketing budgets and resources must be carefully managed to optimize reach. And the connection (and communication) between demand creation and demand management must be precise - no longer can the right hand not know what the left hand�s doing � imagine a pitcher and no catcher. So, what options and solutions might a hotel consider to better manage this �distribution revolution�? Consider the following:

# 8 ISHC Top Ten Issue

As international travel has become more available and less expensive, particularly during the last two decades, the ability to travel unhindered from country to country has almost evolved as an inherent right of business and leisure travel. In certain cases, special permission has been required in the form of visas and work permits, but for the majority of us, we presented nominal identification at the border before being welcomed into whatever country we were visiting. However, the events of September 11, 2001 and a number of subsequent terrorism acts, has begun a process and a change in cross-border policies, particularly in North America, that might have a significant negative impact on the hotel industry. In the U.S., new security arrangements were introduced in 2004, paving the way for the introduction of new high-tech identification cards to have been introduced on January 1, 2008. During the summer, the Senate passed an amendment postponing the program until June 1, 2009, although there remains some skepticism whether the law will pass or not. If enacted, however, the introduction of the new security measures, known as the Western Hemisphere Travel Initiative, will have a clear impact on travel between the US and its neighbors, particularly the overnight sector. To put this into perspective, a survey undertaken in Canada for the Hotel Association of Canada indicated 36% of Canadians planned at least one trip to the U.S. this year, with 24% indicating they would stay at least one night. However, when asked about the imposition of passport requirements for cross-border travel, 27% indicated they would likely cancel the trip. Of the 117 million nights spent by Canadians visiting the U.S. (2005), therefore, it is conceivable that one quarter would not travel across the border if this Western Hemisphere Travel Initiative proceeds. In considering this potential impact, one also has to remember that Canada has historically been the greatest single source country of visitors to the U.S. (about 30% of all foreign visitors to the U.S.) because of its proximity and ease of access; it is likely that of the remaining 70% of foreign visitors, there would be a higher rate of attrition. In Europe, the situation is slightly different; the formation of the European Union, with its creation of a powerful economic zone to compete at the global level, was accompanied by an agreement of virtually unrestricted travel among the member nations. The right of every European citizen to move and reside freely within the territory of the Member States is enshrined in the Charter of Fundamental Rights of the EU, adopted in December 2000. The fundamental approach to border patrol is written into the �Schengen Convention� which lays the responsibility on those member countries accepting visitors from outside the EU; the prevailing mindset is protect the exterior border of the EU but permit unrestricted travel inside. While there is less risk of impact on overnight travel by Europeans within Europe, there remains the potential impact of a decline in visitors from the U.S. where the travel permit issue is currently most poignant. There were approximately 30 million U.S. resident visits to Europe in 2005, accounting for approximately 15% of the total foreign visits; a loss of any large fraction of this volume would seriously impact the European hotel industry. In the remaining areas of the world, the immediate risk to the hotel industry seems to be lower. For the most part, there is less international travel, and those who do travel tend to already be equipped with passports and international travel documents. However, in the longer term, emerging destinations such as China, India and South America may well impose tighter document control and more stringent customs/immigration procedures that could dampen visitors� enthusiasm. For the time being, the impact of tighter travel permit restrictions is seen only as a potential threat to the hotel industry, with the effects yet to be realized. As individual countries take steps to protect their borders, we are likely to see varying degrees of control imposed. It seems inevitable, however, that biometric passports, facial recognition, optical scans, fingerprint readers and other technology will become an everyday part of cross-border travel. The question will be at what point do the price and imposition cause the traveler to re-evaluate their travel plans. # 9 ISHC Top Ten Issue

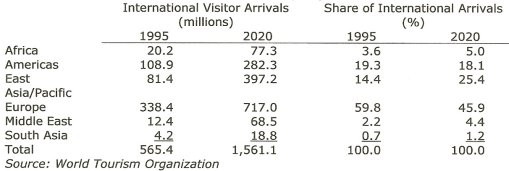

The World Tourism Organization estimates that global tourism visitation (as measured by arrivals) has increased from 550 million in 1995 to 770 million in 2005 and is expected to continue to increase reaching 1,561 million by 2020. China alone is expected to generate 100 million outbound tourists by 2020 up from less than 15 million currently. As the number of international travelers increases, the beneficiaries (i.e., countries and specific destinations) of international tourism will also change. In many cases, historically popular destinations may make gains in the aggregate number of visitors, but the proportion of total share is likely to decrease. A growing interest in �new� and/or previously less accessible destinations (such as Vietnam and China) as well as the strong growth of more traditional destinations (e.g., Singapore) is driving this shift as well as more practical considerations such as location and modes of transportation. Share of World Passenger Traffic 2023

Note: The dark figures in the circles represent 2004 domestic passenger volume (e.g., intra Asian travel) while the dark figures over the lines represent 2004 inter-regional travel (e.g., Europe to North America). The light coloured figures represent percentage change between 2004 and 2003. The World Tourism Organization forecasts significant growth in the aggregate

number of visitors in all regions of the world but the share of travelers

will shift significantly. From a share perspective, the historically

dominant regions of Europe and the Americas will see the greatest declines

while East Asia/Pacific will experience the greatest gains. As a result

based on current projections East Asia / Pacific will overtake the Americas

as the 2nd most important destination by 2020. Nevertheless Europe will

remain as the top destination and will also see the highest increase in

absolute numbers, followed closely by East Asia / Pacific, with Americas

coming in 3rd place.

Share by Region�1995 and 2020  What is driving this rapidly expanding outflow of visitors? Among the leading reasons, travel is being seen as luxury rather a consumer staple at most income levels and as incomes in emerging markets rise, so does the demand for traveling. Regarding the increasing share of Asia it can be attributed to a large extent to the growth of China outbound travel which concentrates in Asia (in 2004, over 70% to Hong Kong / Macao and almost 20% rest of Asia) Demographics are also supporting this interest, again notably among emerging countries, where populations tend to be younger (as opposed to the western world where seniors and near seniors are the fastest growing age brackets) and the middle class is rapidly expanding. Awareness of foreign destinations through electronic images, the rapid acceptance of new telecom products and international branding/marketing has a direct appeal to this younger, more affluent demographic. The four BRIC countries (Brazil, Russia, India and China) provide an interesting perspective of this demographic shift. .

Source: CIA World Fact Book More travelers though does not necessarily translate into �more of the same� when it comes to travel products and services however. Citizens of the BRIC countries and other emerging origins will affect the face of travel in more ways than sheer numbers. For example,

#10 ISHC Top Ten Issue

Capital provides asset liquidity and enables the development of new hotels. Increasing institutional investment into the hotel sector is enhancing asset values and consequently lowering returns. Expectations of revenue and profitability growth are stimulating capital availability for new development. This environment is expected to continue as long as the hotel industry�s cyclical expansion continues. Signs of a cyclical plateau are starting to appear, and the implications of capital availability will be profound. Many factors affect the amount, timing, and availability of capital. In the US the fractured economic conditions that existed after 2001 eroded operating results and values over the ensuing few years, but this in turn set the stage for the current cyclical upturn. Modest potential for new supply, together with the industry�s high degree of operating leverage, have now made hotels highly attractive relative to other commercial asset classes. As a consequence, a large migration of institutional capital to the hotel sector was not long in coming. Investors have bid up hotel prices and bid down required yields to relatively low levels. The momentum of the hotel investment market has been enhanced by significant liquidity in the mortgage markets. Are today�s hotel investors smarter than those in preceding cycles? Evidence suggests that some investments are being underwritten with little margin for error. But the industry itself has not changed: significant operating risks remain. Hotels continue to be a demanding, management-intensive business. Nightly �leases� of guestrooms create more cash-flow volatility than long-term office or retail leases. An expanding pipeline of planned additions to supply may impact existing properties. The robust cyclical recovery may have overshadowed some investor�s perceptions of these risks. Many investors believe that barriers to entry for new hotels are now unusually high. Traditional barriers such as available sites and competing land uses have been augmented by issues of construction materials� availability and cost. Despite recovering profitability, high development costs undercut the feasibility of a great many projects. However, the ongoing recovery of operating fundamentals, the expectation of further gains, and the easy availability of capital are all encouraging construction pipelines to swell in many markets. Positive investment factors often go hand-in-hand with loosening underwriting standards, and this appears to be an accurate picture of the current climate for hotel capital. Loan-to-value ratios have drifted upward for both primary and mezzanine debt, while heavy competition has pushed down interest rates. Mortgage defaults remain low for the time being, but the margin for error is clearly diminishing. Some research indicates that operational gains may be starting to plateau. Opportunistic investors would likely be the first to leave for greener pastures. If they do, a sizable source of capital will leave the sector. This in turn should cause values to moderate. It may also take more time to monetize hotel holdings. Investors should start now to re-conceive exit strategies and ensure that they don�t get caught behind the market curve. In all, the efficient flow of capital into the hotel sector has helped

the industry overcome the difficulties experienced earlier in the decade.

Supply, demand, profitability, and yields have been relatively in sync,

with positive consequences on the operating and asset sides of the market.

Maturation of the industry�s expansionary cycle is likely to result in

a moderation in capital availability and increase in capital costs.

Being aware of these trends will enable hoteliers and investors to plan

ahead and take advantage of capital market conditions.

About ISHC The International Society of Hospitality Consultants (ISHC) is a professional society with 190 members in 21 countries. Membership is by invitation only and members are leaders in the industry in their respective areas of expertise. With over fifty areas of specialty expertise represented in the society and member and experience working in over 65 countries, ISHC represents a one of kind collection of experience and expertise worldwide. For additional information on ISHC or the ISHC Top Ten Issues in the Hospitality Industry for 2007 please visit the ISHC web site at www.ishc.com or contact Lori Raleigh, Executive Director, ISHC, at [email protected]. |

| Contact:

ISHC

|

| Also See: | Shrinking Labor Force is Top Challenge for Global Hospitality, Tourism & Service Industries / Jeff Coy / January 2006 |

| Top Ten Global Issues and Challenges In the Hospitality Industry for 2006 / ISHC / December 2005 |