|

|

|

|

|

|

|

|

But So Do Expenses - 2006 Trends in the Hotel Industry |

| Atlanta, May 23, 2006: In 2005, U.S. hotels were able to turn

a healthy 8.8 percent rise in total revenue into an impressive 15.5 percent

increase in profits according to the recently released 2006 edition of

Trends in the Hotel Industry published by PKF Hospitality Research (PKF-HR),

an affiliate of PKF Consulting. This marks the second consecutive

year of double-digit profit growth for U.S. hotels. However, expenses

continue to escalate at a level more than twice the rate of inflation,

causing concern for hotel owners and operators.

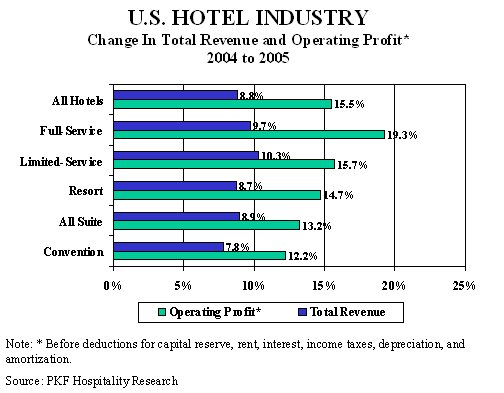

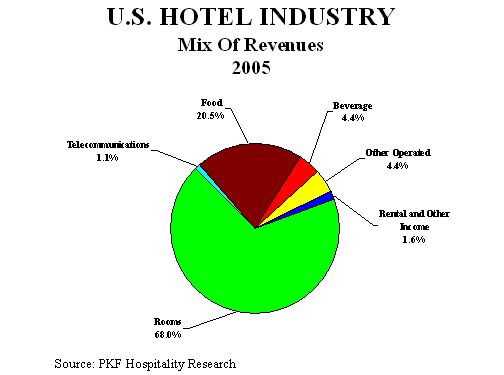

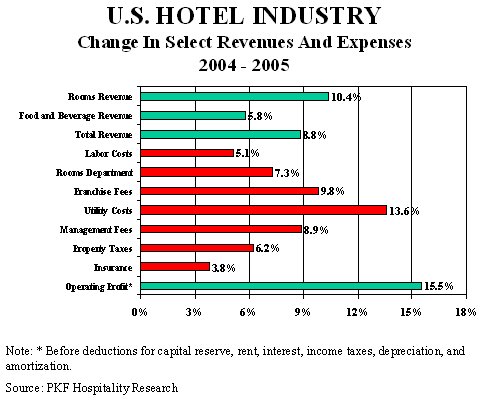

.  �Overall, the strong economy has been a blessing for U.S. hotel managers. However, it also presents some operational challenges,� said R. Mark Woodworth, president of Atlanta-based PKF-HR. �Hotels have been the beneficiaries of strong increases in demand that have resulted in tremendous gains in revenue. However, the inflated costs of such expenses as property taxes, utilities, and labor have inhibited the flow-through of top-line dollars into bottom-line profits.� In 2005, the cost of operating a U.S. hotel grew 6.5 percent. Leading all expenses in percentage growth were utilities that grew 13.6 percent from 2004 to 2005. The largest cost center, labor and related expenses, increased by 5.1 percent last year, creating another drag on profit growth. �Hotel managers have some degree of control over expenses like labor, but limited control over contractual or municipal costs such as management fees, franchise fees, property taxes, insurance, and utilities,� Woodworth noted. The 2006 Trends in the Hotel Industry report marks the 70th annual review of U.S. hotel operations conducted by PKF. This year�s sample draws upon year-end 2005 financial statements received from approximately 5,000 hotels across the country. Profits are defined as income after management fees, property taxes, and insurance, but before capital reserves, debt service, rent, income taxes, depreciation, and amortization More Properties Benefit Unlike 2004, a wider variety of properties started to benefit from the industry upswing during 2005, the second year of recovery from the 2001-2003 recession. �In 2004, we observed that the larger hotels with higher room rates experienced the greatest increases in profitability,� Woodworth said. �In 2005, all five property types in our Trends survey achieved strong gains in total revenue, as well as double-digit increases in bottom-line profits.� PKF-HR breaks down their survey sample into five property categories: full-service, limited-service, convention, all-suite, and resort. Among the different property categories, limited-service hotels achieved the greatest increase in revenue (10.3%), while full-service hotels achieved the greatest increase in profitability (19.3%). While convention hotels lagged the other property types somewhat in terms of revenue and profit growth, the 7.8 percent gain in revenues and 12.2 percent increase in profits posted by these hotels are well above the long-term averages for this segment. Components Of Revenue Growth For the hotels in PKF�s 2005 Trends sample, a 2.9 percent increase in occupancy combined with a 7.4 percent increase in ADR to generate a 10.4 percent increase in RevPAR. This favorable mix of RevPAR drivers was the primary reason for the high growth in profits achieved in 2005. �Following typical market recovery scenarios, we expect ADR growth to dominate RevPAR increases in the next few years,� Woodworth noted. �In fact, the Spring 2006 Hotel Outlook forecast prepared by PKF Hospitality Research and Torto Wheaton Research calls for ADR to grow 4.7 percent in 2006, while occupancy growth slows to 1.5 percent.� In 2005, revenues from all other minor-operated departments did not keep pace with the significant rise in rooms revenue. The combined revenues from the food department, beverage department, telecommunications, other operated departments, and rentals and other income increased by 5.6 percent from 2004 to 2005. �Since guest count is frequently the impetus of sales for these supplemental operated departments, this comparatively slow growth rate can be attributed to the fact that the number of rooms occupied grew only 2.9 percent in 2005,� Woodworth said. �Fortunately, the cost of operating these other departments grew just 4.3 percent, thus revealing that the minor-operated departments did contribute to the increase in overall hotel profitability.� Not contributing to the increase in bottom-line profits was the telecommunications

department. Sales in this department dropped another 7.6 percent

in 2005, the fifth consecutive year of revenue declines.

Expenses Grow With Business Volume Total operating expenses for the hotels in the Trends sample grew 6.5 percent in 2005, double the 3.3 percent rate of inflation for the year. �As we have seen in the past, strong growth in revenues was able to mask significant increases in the cost of operating a hotel,� Woodworth noted. - Labor Costs.  Approaching Peak Performance Looking to the future, PKF Hospitality Research finds the U.S. hotel industry starting to approach the peak of the current cycle. Growth is forecast to continue in all major industry measurements � occupancy, ADR, RevPAR, and profits. However, the pace of growth is expected to slow down as most markets begin to exceed their long-term natural performance levels. �Like other forms of real estate, the lodging industry performs in cyclical patterns. Based on our analysis of supply, demand, and economic conditions, we believe the U.S. hotel industry is leaving the recovery phase of the current cycle and approaching the peak,� Woodworth noted. �Life at the peak of a business cycle is both exhilarating and treacherous. While we foresee an extended period of peak performance for U.S. hotels, we also know that a potential downturn lies somewhere on the horizon.� �Leaving the recovery phase and approaching the peak means that we will see a slowdown in the rate of revenue and profit growth compared to recent years,� Woodworth said. �However, this deceleration does not mean that the lodging industry is entering a recession. In fact, several factors lead us to forecast a persistent period of strong performance for U.S. hotels in the next few years.� PKF Hospitality Research is forecasting total revenue growth of 7.6 percent in 2006 and 4.1 percent in 2007. This is projected to result in profit gains of 14.9 percent and 7.0 percent, respectively, in 2006 and 2007. Based on this forecast, U.S. hotels will be achieving a profit of approximately $14,800 per-available-room in 2006 and $15,800 in 2007. The 2007 figure is slightly more than the $15,674 profit level generated at the peak of the last cycle in 2000. �On the surface, the hotel profit picture appears to be very attractive. However, in real dollars, most owners and operators are still 20 percent behind where they were in 2000. For those property owners that have been riding the ups and downs of the lodging cycle since the year 2000, their smile will not totally return until real profits have fully recovered, which might not be until the end of this decade,� Woodworth concluded. To purchase a copy of the 2006 Trends in the Hotel Industry survey or a Benchmarker report, please visit the firm�s online store at www.pkfc.com/store, or call Claude Vargo at (404) 842-1150, ext. 237. PKF Hospitality Research (PKF-HR), headquartered in Atlanta, is the research affiliate of PKF Consulting, a consulting and real estate firm specializing in the hospitality industry. PKF Consulting has offices in New York, Philadelphia, Washington DC, Atlanta, Indianapolis, Houston, Dallas, Los Angeles, and San Francisco. |

| Contact:

R. Mark Woodworth

|