![]()

advertisement

..

|

|

![]()

advertisement

|

Historical Analysis & 2006 Forecast |

| By: David J. Sangree, MAI, CPA, ISHC, Laurel A. Keller, and Joseph

Pierce

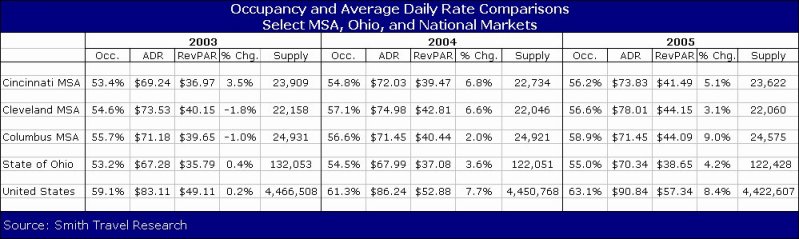

March 2006 Summary This analysis reviews Ohio�s three major lodging markets over the past five years and projects future hotel performance in the Cleveland, Columbus, and Cincinnati MSA�s. It examines historic operating performance, hotel sales, new development and local attractions that affect demand to present a detailed view of each market�s performance and potential. Metropolitan, State, and National Hotel Performance Comparisons This chart shows the historical lodging performance for the Cleveland,

Columbus, and Cincinnati MSA markets as well as for Ohio and the United

States for YE2005.

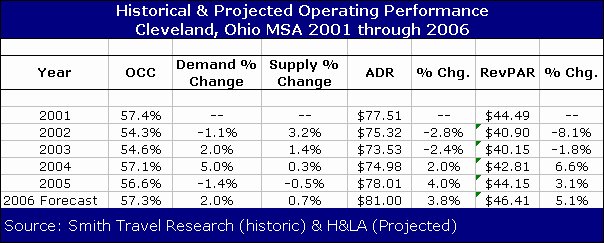

The following sections present a detailed analysis of the individual Ohio hotel markets of Cleveland, Columbus, and Cincinnati. Cleveland, Ohio The Cleveland MSA includes hotels located in Cuyahoga, Ashtabula, Geauga, Lake, Lorain, and Medina counties (22,060 rooms). The Akron MSA (located directly south of the Cleveland MSA in Stark and Summit Counties) contains an additional 6,652 hotel rooms in Stark & Summit counties. Unless otherwise noted, the Akron MSA is not part of this analysis. Historical Performance: The following chart depicts the past five year�s

historical operating performance of the Cleveland MSA�s hotels and our

projection for 2006.

Occupancy dipped slightly in 2005 after increasing in 2003 and 2004 despite the lack of new supply in the market. Although demand decreased in 2005, average daily rate climbed to the highest level recorded during the five year period. Based upon current economic conditions, we project occupancy levels to increase slightly in 2006 as compared to 2005. Furthermore, we project a more substantial increase in average daily rate, as Cleveland area hotel operators project additional rate increases in 2006. Recent Hotel Sales: A total of 13 hotel sale transactions occurred in the greater Cleveland market during 2005. Below are three prominent sales.

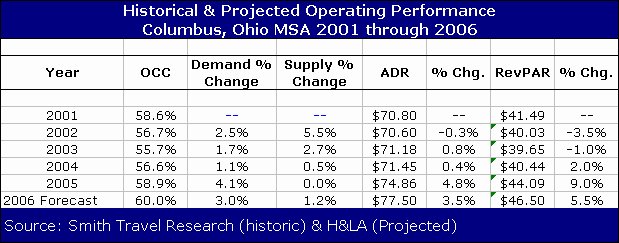

. .  These attractions combined to present Cleveland on a world stage which provides long-term benefits including international business opportunities. The Cleveland lodging market has been soft for a number of years, exacerbated by the slumping economy. However, the RevPAR increase realized in 2005 is encouraging, as the improving national economy and lack of new supply in the market allowed for rate growth despite a decrease in overall demand for rooms. For 2006, hotel operators anticipate ADR growth in addition to minimal occupancy improvement. The positive movement will still be modest as the area lacks a significant new demand generator and continues to postpone the development of a new convention center. Columbus, Ohio As the state capital, the county seat for Franklin County and the largest city in Ohio, Columbus is the focal point for government activity within the state. Government related business provides a demand generator for hotel rooms in Columbus that is not significantly impacted by the rise and fall of economic activity within the state. Additionally, Ohio State University, the state�s largest university, is located in the Greater Columbus area and provides the area with a solid employment base as well as a significant demand driver for hotel rooms. Historical Performance: The Columbus MSA experienced a significant increase in the supply of hotel rooms from January 2001 to December 2002. In that period, 28 hotels opened adding a net 2,567 guest rooms to the market. The following table depicts the past five year�s historical performance

of the Columbus MSA�s hotels.

As the table shows, despite the events of September 11th and the downturn of the national economy, Columbus posted a 2.5% increase in demand for the period 2001 to 2002. The demand growth was overshadowed by the increase in supply mentioned above resulting in a decline of 1.9 occupancy points. Occupancy continued to decline in 2003 as the growth in supply, 2.7% over 2002, outpaced the demand for hotel rooms. Occupancy grew in 2004 and again in 2005 as overall demand increased by 1.1% and 4.1% respectively, while the increase in the supply of hotel rooms grew 0.5% in 2004, with no new supply in 2005. Average daily rates recorded a minimal decline between 2001 and 2002 before increasing between 2003 and 2005. The 2005 ADR was recorded at $74.86, indicating a 4.8% increase from the 2004 ADR of $71.45. We project occupancy levels to increase in 2006 as compared to 2005 based upon current economic conditions with an above inflationary increase in average daily rate. Recent Hotel Sales:Thirteen hotel sale transactions occurred in the greater Columbus market during 2005. Below are three prominent sales.

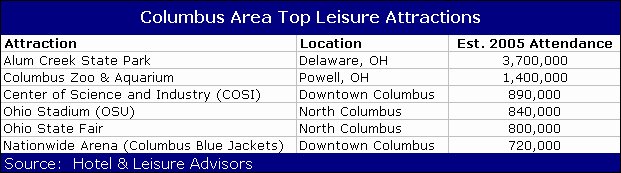

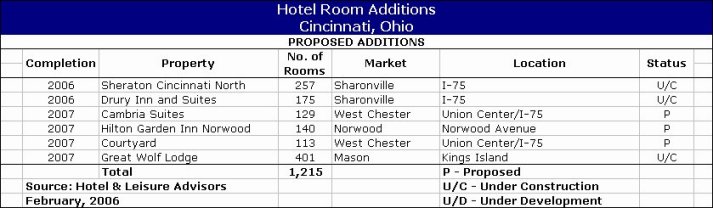

.  The Polaris area around I-71 is rapidly becoming a major development node for the Columbus market with five projects announced and additional ones being discussed. These new projects at Polaris are projected to impact the existing market in Worthington where a bulk of the north side hotels are located. The Holiday Inn Fort Rapids will open with its indoor waterpark in the summer of 2006 and introduce the first indoor waterpark resort to the Columbus region. Leisure Attractions:Columbus area attractions were a mixed bag of success

and disappointment in 2005. COSI Columbus hosted Titanic: The Artifact

Exhibition, in 2005 and was the most visited exhibit in COSI history with

more than 226,000 visitors during its six-month run. Nationwide Arena,

a focal point of the Arena District development in downtown Columbus, was

dark many evenings as the NHL cancelled its 2004-2005 season as a result

of a labor dispute lockout. The following chart lists the top leisure-oriented

attractions in the greater Columbus market.

Ohio State University provides exciting college football and basketball events, as well as other sporting competitions. Schottenstein Arena, a 19,500 seat facility on the OSU campus hosted the 2005 Division I Men�s Ice Hockey Championship. In 2004 OSU and the City of Columbus hosted the NCAA Men�s Basketball First and Second Rounds tournament at Nationwide Arena. Columbus benefits from its central location in Ohio and its status as the state capital. The development of the Polaris, the Arena District, and other major projects have encouraged economic growth in the Greater Columbus area. The stability provided by governmental activity and the area educational institutions bode well for the prospect of long-term economic growth in the Columbus region. The Columbus lodging market continues to show positive demand but still lags behind national trends. However, the decline in new supply has made way for improved occupancy and ADR yielding positive RevPAR growth in 2004 and 2005. Hotel operators can anticipate ADR and occupancy growth in 2006, resulting in a third consecutive year of RevPAR improvement. Cincinnati, Ohio Historical Performance:The Cincinnati MSA saw a large increase in the supply of hotel rooms between 1997 and 2000. According to Smith Travel Research, the occupancy percentage for the Cincinnati MSA stood at 60.2% in 1997 and declined year after year reaching a low point of 50.1% in 2001. The following chart depicts the past five year�s historical performance

of the Cincinnati MSA�s hotels.

Demand increases have been consistent over the past five years and are projected to continue. The growth in demand coupled with the modest overall decline in supply has allowed the market to absorb the pre-2001 supply additions and improve occupancy. The market saw a slight decline in ADR post 9/11, but has been able to advance rates each year since 2003. The combination of increased occupancy and ADR has afforded the Cincinnati market to post RevPAR growth each of the past five years. We project continued demand growth with limited increase in supply, which should afford occupancy and ADR levels to continue to grow in 2006 as compared to 2005 based upon current economic conditions. Recent Hotel Sales: Nine hotel sale transactions occurred in the greater Cincinnati market during 2005. Below are three prominent sales.

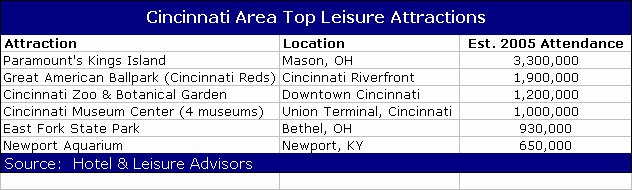

.  The Sheraton Cincinnati North Hotel was formerly a Radisson, which had been closed for two years while it underwent a $20 million renovation. When it reopened it became the only full-service hotel within walking distance of the Sharonville Convention Center. The Union Center/West Chester market is due to add two additional hotels while the indoor waterpark resort Great Wolf Lodge is due to open adjacent to the Kings Island amusement park. Leisure Attractions: Cincinnati�s most widely visited attraction is

Paramount�s Kings Island, an amusement park located in suburban Mason,

which attracts over three million people annually. The Ohio River area

is one of Cincinnati�s premier entertainment districts featuring restaurants,

nightclubs and gaming facilities. Several of these facilities have developed

on floating barges and riverboats in an area located in Newport, Kentucky

known as Riverboat Row. The following chart lists the top leisure-oriented

attractions in the greater Cincinnati market.

Cincinnati�s most widely attended events include Cincinnati Reds baseball, Cincinnati Bengals football, the Kroger Senior Classics Golf and Oktoberfest. Cincinnati also supports a number of cultural opportunities including the Cincinnati Opera, Cincinnati POPS, Cincinnati Symphony Orchestra, Cincinnati Playhouse in the Park and The May Festival. The Cincinnati Convention Center is currently undergoing a $160 million expansion and reconfiguration. When completed in 2006, the facility will offer nearly 200,000 square feet of contiguous exhibition space, more than 100,000 square feet of meeting space including a 40,000 square foot ballroom, a 17,400 square foot ballroom, 37 meeting rooms and more than 750,000 gross square feet of space including pre-function areas and support space. The Cincinnati area�s continual expansion of regional attractions coupled with the limited growth in hotel guest room supply has helped bolster the Cincinnati occupancy and ADR in recent years. The expansion and reconfiguration of the convention center and the overall economic growth of the region bode well for the prospects of the hospitality industry in Cincinnati. The Cincinnati lodging market continues to absorb the overbuilding of the late 1990s causing its occupancy to lag behind that of the other two major cities in the state. However, demand for hotel rooms has been consistently stronger than Columbus or Cleveland and has afforded the market the opportunity to grow occupancy, ADR and thus RevPAR year after year. Ohio Outlook The three major Ohio metropolitan areas are each showing signs of growth although at different speeds. The Cleveland market was the only one to record a decline in demand in 2005 which is not expected for 2006. The Cincinnati market will benefit from the expansion of the convention center which should boost demand for the downtown properties. The Columbus market is benefiting from its government base and stronger corporate growth than in the other two major cities. Authors

Since 1987, Mr. Sangree has provided consulting services to banks, hotel companies, developers, management companies, and other parties involved in the lodging sector throughout the United States, Canada, and the Caribbean. He has spoken on various hospitality matters at seminars throughout the United States, and has written numerous articles for, and is frequently quoted in, magazines and newspapers covering the hospitality field. He can be reached via telephone at (216) 228-7000 ext. 1 or via e-mail at [email protected]. Joseph Pierce is a Senior Associate with Hotel & Leisure Advisors. He received an MBA from Michigan State University�s hospitality program in 1981 and a Bachelor of Science in Accounting from the State University of New York at Brockport in 1978. He has a wide range of experience in operations and accounting in hotels and resorts. Mr. Pierce has been a Controller and Director of Finance and Accounting for Clarion, Renaissance, Marriott, and Westin Hotels. He also managed an independently-owned hotel, The Talbott Hotel in Chicago. Mr. Pierce has performed appraisals, market feasibility studies, and impact studies nationally. He can be reached via telephone at (216) 228-7000 ext. 3 or via e-mail at [email protected]. Laurel A. Keller is an Associate with Hotel & Leisure Advisors. She received her Bachelor of Science in Hospitality Management from Purdue University in 1997. She has been active in valuation and consulting for hotels, resorts and other leisure oriented income-producing properties since 2001. She previously held management positions with the Sheraton Cleveland Airport Hotel and the Sheraton Cleveland City Center Hotel. She can be reached via telephone at (216) 228-7000 ext. 2 or via e-mail at [email protected]. |

| Contact:

Hotel & Leisure Advisors, LLC

|

| Also See: | Indoor Waterparks and Hotels - Year end 2005 Overview / David Sangree / February 2006 |

| David J. Sangree Forms New National Hospitality Consulting Firm: Hotel & Leisure Advisors / October 2005 | |

| Hotel Capitalization Rates Drop Further / May 2005 | |

| Cleveland�s Lodging Market: A Slow Climb Back / David J. Sangree & Joseph Pierce/ February 2005 | |

| Indoor Waterpark Resorts Continue Impressive Growth in �05; a Viable Segment of the Travel / David J. Sangree / January 2005 | |

| Indoor Waterpark Resorts Expand Nationwide / David J. Sangree / April 2004 | |

| Appraisal and Financing of Indoor Waterpark Resorts / David J. Sangree / October 2003 | |

| Cleveland Lodging Market at Bottom with Improvement Predicted / US Realty Consultants, Inc. / January 2004 | |

| Hotel Capitalization Rates Drop Again / David J. Sangree, MAI, CPA, ISHC / April 2004 | |

| Hotel Capitalization Rates Drop / David J. Sangree, MAI, CPA, ISHC / February 2003 |