California is well positioned

for a strong

year with healthy supply and

demand fundamentals

Macroeconomic Observations

�During

the first half of 2005, the U.S economy demonstrated signs of modest improvement,

as the federal funds rate increased to 3.0% in June 2005. It is anticipated

that the rate will reach 4.5 % by August 2006. �During

the first half of 2005, the U.S economy demonstrated signs of modest improvement,

as the federal funds rate increased to 3.0% in June 2005. It is anticipated

that the rate will reach 4.5 % by August 2006.

�Preliminary economic analysis indicates a 3.0 % real GDPgrowth rate

during the second quarter of 2005, and economists predict 3.75% growth

through the end of 2006. As GDPsustains moderate growth, the national unemployment

rate is anticipated to stabilize in the upcoming quarters following a decrease

of 0.2 percentage points in the second quarter of 2005 to 5.2%. It is anticipatedthat

the unemployment rate will stabilize at 5.0% through 2006.

�Personal consumption decreased by 0.7 percentage points to 3.5% in

the first quarter of 2005. Consumer Price Index inflation increased during

the first half of 2005 to a 3% annualized rate, but is anticipated to decrease

in the second half of the year, with a modest increase to 2.6% in 2006.

�According to the National Association of Realtors, existing-home sales

surpassed market expectations and reached another record in June as low

mortgage interest rates and favorable market conditions continued to attract

buyers. In June 2005, total existing-home sales, including single-family,

town homes, condominiums and co-ops, increased to an annual rate of 7.33

million from 7.14 million in May. �The Consumer Confidence Index increased

to 102.2 in May 2005, after experiencing four months of decline. As consumers�concerns

about the economy and jobs ease, the Expectations Index, while slightly

below 2004 levels, continues to signal economic growth in the months ahead.

U.S. Lodging Industry Analysis

�The U.S. lodging industry continues to experience strong positive lodging

fundamentals, building upon 2004 levels. Through June 2005, occupancy increased

1.7 percentage points to 62.2% and ADR increased approximately 4.8% to

$90.45 compared to the same period last year, according to SmithTravel

Research (�STR�). Additionally, growth in rooms demand continues to outpace

the growth in supply. Growth in lodging fundamentals is anticipated to

continue through the remainder of the year, as occupancy and ADR are forecasted

to finish at 63% and $90, respectively.

�The United States continues to experience positive internationalvisitation,

building on 2004, which was the first year to experience positive international

inbound travel growth since 2000. According to the U.S. Office of Travel

and Tourism Industries (�OTTI�), international inbound travel to the U.S.

increased by 12.7% through the first quarter of 2005, as compared to the

same

period last year. International travel experienced growth of 4.5% from

Asia, 12.3% from Europe, 14.4% from Central America, and 2.3% from Africa.

The significant increases in visitor arrivals are primarily attributed

to the continued weakness of the U.S. dollar, an increase of approximately

27.8% in sales and marketing efforts in international markets, and Japan�s

gradual recovery from the economic recession that began in mid-2004. The

U.S. Department of Commerce forecasts 6% growth overall in the numberof

international visitors in 2005.

�With decreased national unemployment rates and increased corporate

budgets, business travel experienced a rebound in 2004 as volume increased

by approximately 4%. The rebound in business travel has continued into

the first half of 2005, as urban and airport hotels (which primarily cater

to business travelers) led RevPAR growth over 2004 levels with 10.7% and

10.9%, respectively. According to the Travel Industry Association of America

(�TIA�), business and convention travel is anticipated to continue to outpace

leisure travel in growth with an increase of approximately 3.6% this summer.

TIA predicts that leisure travel will increase this summer by approximately

2.8% to 328 million person trips, as approximately 75% of U.S. adults plan

to take at least one leisure trip this summer, representing an increase

of 5 percentage points over the same period last year.

�The strength of the lodging market and favorable economic conditions

has led to an increase in hotel transactions and new hotel construction.

Many of the hotels currently in the development pipeline, however, will

not enter the market until 2006 and beyond. Lodging Econometrics anticipates

net supply growth for 2005 to be approximately 0.8%; however, according

to STRdata, U.S. lodging supply increased by 0.5% through May 2005. Furthermore,

the availability of capital has led to more active transaction markets

in 2005. Among the most active companies involved in lodging transactions

has been The Blackstone Group, which recently purchased the Rihga Royal

Hotel in New York and acquired Wyndham International, Inc. for $3.24 billion.

In addition, Marriott International, Sunstone Hotels, and Walton Street

Capital acquired a 32-hotel portfolio from CFT Holdings, Ltd. for approximately

$1.45 billion. Significant single-asset transactions include the sale of

the Hilton Gaslamp Quarter in San Diego by S.D. Bridgeworks LLC to LaSalle

Hotel Properties for approximately $85 million and the sale of the Hilton

Glendale in Glendale, California, by Hilton Hotel Corporation to Eagle

Hospitality Properties Trust Inc. for approximately $79.8 million. U.S.

hotel sales reached $12.9 billion in 2004, nearly doubling the $6.7 billion

sold in 2003. Transaction activity forthe U.S. lodging market is anticipated

to remain strong at an anticipated $9 billion in 2005.

�According to Smith Travel Research (STR), midscale properties without

food and beverage outlets experienced the largest growth in RevPAR (approximately

11.8%) in the first half of 2005. The luxury segment leads the industry

in ADR growth of 7.4% for the first half of 2005 vs.. the same period last

year. This trend can be primarily attributed to increasing disposable incomes

of the aging baby boomer generation and reduced restrictions placed on

corporate travelers.

California Mid-Year Lodging Report

California Lodging Industry Observations

�California�s lodging market continues to outperform the U.S in terms

of RevPAR (revenue per available room). For the first half of the year,

California�s RevPAR was $68.56 while the U.S.�s RevPAR was $56.31. During

the first six months of 2005, California�s occupancy increased to 68.1%,

an increase of 2.1 percentage points from 2004�s first six month occupancy

rate of 66%, while ADR increased approximately 4.8% over the same period.

�According to Los Angeles Economic Development Corporation (�LAEDC�),

the international trade industry YTD through April 2005, as compared to

the same period last year, demonstrated an increase in two-way international

trade through California�s three customer districts. San Francisco has

increased 6%, LosAngeles 9.8%, and San Diego 14.6 %. With the historically

busiest quarters yet to come, it is anticipated the industry will achieve

a record high of $459.3 billion in 2005. This trend hasled to plans to

expand the ports of San Diego, Los Angeles, and Long Beach.

�The California Division of Tourism budget has received $7.3 million

in public funding for 2005-06 fiscal year after receiving no public funding

due to a $9 billion dollar deficit since fiscal year 2003-2004. According

to the Industry Association of America, last year�s budget of $7.39 million

ranked California below the national average of $11.95 million dollars.

In 2004, tourism contributed approximately $78 billion dollars to California�s

economy and it is anticipated the restoration of public funding will increase

future visitation.

�The California Travel and Tourism Commission (CTTC) forecasts 2%growth

for domestic travel and 4.8% growth for international travel due to a strong

euro, diminishedanxiety about air security from Europe, improved consumer

confidence, and an increase in number of routes by low-fare airlines. DK

Shifflet and Associated, Ltd. estimated an increase in travel to and through

California duringthe Spring and Summer seasons (2.9% and 3.5% respectively),

with resident travel increasing at an estimated 2.4% and non-resident travel

remaining unchanged. Domestic and international air arrivals demonstrated

consistent growth throughout 2004 and are anticipated to continue to improve

throughout 2005. The drive-in market is anticipated to remain strong as

increases in gasoline prices are not anticipated to change travel plans.

�The number of overseas visitors to California from the two largest

markets, the United Kingdom and Japan, are anticipated to increase throughout

the remainder of the year. The Association of British Travel Agents anticipates

a record number of British tourists to the U.S. for 2005 due to the weak

dollar vs. the British pound and competitive transatlantic air fares. Japan

is anticipated to increase outbound travel in 2005 to 17.6 million, representing

an increase of approximately 6%. Major Japanese travel wholesalers, such

as JTB, KNT, Jalpak, and ANAHallo, stated the number of tours occurring

during the first quarter of 2005 increased approximately 10% -15%. United

Airlines recently began nonstop service between San Francisco International

Airport and Nagoya and added double daily flights between Los Angeles International

Airport and Narita. Furthermore, Governor Schwarzenegger�s first official

overseas trade mission to Japan in November generated media publicity in

Japan and is anticipated to increase travel to California from Japan in

the coming years.

�Native American gaming continues to positively affect tourism for California.

Currently, approximately 55 casinos operate in California with additional

projects under development. In 2004, California's Native American gaming

revenue increased 13% over 2003 levels to $5.3 billion and generated 28%

of the nation's Native American gaming revenue (2.5 times more than Connecticut,

its closest rival). Growth for 2005-2006 is anticipated to continue with

the following plans for new developments underway:

-

The North Fork Rancheria of Mono Indians has been planning on building

a large casino on State Route 99 at Avenue 17. This �destination resort�

would include a 200-room hotel, several restaurants, a large casino, and

a spa. However, because of the location proximate to the city of Madera,

and the government of California�s desire to keep casinos out of urban

areas, future plans may be stalled.

-

The California Valley Miwok tribe�s proposal for a casino-resort in the

city of Los Banos, which is on the west side of Merced County.

-

Pechanga Resort and Casino, located in Temecula, California is adding a

400,000-square-foot, $252 million expansion in December.

-

The Fantasy Springs Resort Casino in Palm Springs $200 million casino and

restaurant expansion in January which is slated to include a 251-room hotel

and a 100,000-square-foot special events center. Plans to add another 300-400

room hotel by 2010 are under discussion.

-

The Chemehuevi tribe�s plan for a $186 million Indian casino-hotel in West

Barstow.

-

In June 2005, the Lytton tribe�s plan to open a Vegas style casino in San

Pablo was stopped by a U.S. Senate committee. The bill prevents the tribe

from operating Class IIILas Vegas-type slot machines in the Bay Area. Currently,

there are no urban casinos in California.

�The cruise industry continues to expand in California with new routes

offered by Disney Cruise Lines starting in May 2005 and the Queen Mary

2 in 2006. San Diego�s cruise line industry has experienced 300% growth

in the last five years and plans to enhance the port within the next three

years are currently under discussion. The Los Angeles Port has also encountered

a similar growth trend and the city is anticipated to expand the port to

accommodate increased traffic and ship size.

California Mid-Year Top 10 Thoughts

1. Transactions � Hotels in strong locations remain in high demand

due to the current low cost of capital and high replacement cost. Hotels

are attractive to investors seeking a high risk/high yield real estate

investment, particularly as the lodging industry continues to outperform

other sectors of real estate. According to HVS International, the average

value of a U.S. hotel property is anticipated to increase approximately

28% in 2005 and an additional 23% in 2006. In addition to the increase

in property values, readily available financing has also fueled the increase

in the number of hotel transactions. Borrowers have benefited considerably

from higher leverage loans and more flexible loan terms. Although interest

rates may rise slowly in the near future, it is anticipated that the number

of hotel transactions in California will remain strong into 2006 as the

lodging industry continues to demonstrate healthy performance and the reduced

number of loan delinquencies encourages lenders to offerfavorable financing

terms. Primary Impact: Transactions and valuations

2. Condominium Conversions �Both the trend to convert hotels

into condominiums or the trend to develop a �condotel�has become increasingly

popular because operators can boost their own profits while offering buyers

upscale amenities. In 2005, it is anticipated that a larger number of developers

will offer for-sale units in their luxury hotels. Previously, condominium-hotels

existed in leisure destinations, such as Hawaii, and doubled as second

homes. Now, these units have become increasingly more plentiful in urban

centers such as New York, Miami, Chicago, Boston, San Francisco and Toronto,

as well as Las Vegas. As more baby boomers become empty nesters, they are

more likely than the previous generation to move to downtown locations

from their suburban homes, thereby creating the downtown hotel/condominium

trend. This recent trend to create �condotel�units has penetrated Californian

markets and is anticipated to remain hot as long as real estate prices

continue to escalate, interest rates and stocks and bonds remain low, and

the lodging industry sustains its increasing performance. However, due

to concerns surrounding loss of employment for workers at converted hotels,

San Francisco recently passed an 18-month moratorium on condominium conversions.

Primary Impact: Supply and profitability

California Mid-Year Lodging Report

3. Supply Trends � According to Lodging Econometrics (�LE�),

lodging supply is decreasing in some major U.S. markets. Approximately

58,240 new guestrooms were added in 2004,resulting in an estimated 1% net

supply increase. Although 70,646 rooms are anticipated to be added in 2005,

analysis indicates that net new supply growth will be less than 1% this

year due to numerous significant hotels exiting thelodging market. This

trend holds true for Californian markets, such as San Francisco, where

a significant number of guestrooms have temporarily ceased operations as

the properties undergo repositioning, including the Fairmont Hotel which

is transforming 226 of its 591 rooms into condominium units. In Los Angeles,

Anaheim, and along the Californian coast, prime real estate locations are

being bought and restructured to include condominiums to offset the surge

in construction costs and land acquisition, including the Douglas Building

in downtown Los Angeles which wasconverted into 50 luxury condominiums.

In the urban centers of Los Angeles and San Francisco, some hotels are

converting a portion of their guestrooms into residences. The only area

in California that experienced a real growth of hotel rooms in 2004 was

San Diego, which experienced rooms supply growth of 2.5%. According to

LE, it is anticipated that 917 hotels with 100,559 guestrooms will open

in 2007 in the US, the highest total for new openings since 2001. Even

with large increases in supply, market participants anticipate hotel revenues

in 2007 to exceedthe record $26 billion anticipated for 2006.Primary Impact:

Rooms supply

California Mid-Year Lodging Report

4. Labor Issues �During 2005, Los Angeles and San Francisco experienced

hotel labor disputes, an issue that is anticipated to negatively impact

future convention bookings. InLos Angeles, the Unite Here Local 11 succeeded

in securing a contract with an expiration date of November 2006, aligning

the contract with unions in Hawaii, New York, Chicago, Sacramento, Monterey

and Toronto. The union had soughtan expiration date in April of 2006, but

accepted November 30 in the hopes of avoiding a future labor dispute. InSan

Francisco, the labor dispute that began in September 2004 continues to

have negative ramifications for the city. After a nearly year-long labor

dispute, hotel employees and management remain at odds over wages and health

care coverage and have been unable to resolve the conflict involving 4,300

union workers at 14 major hotels. It can be anticipated that this labor

dispute may negatively impact the city�s ability to attract and retain

scheduled conventions as the city has recently lost several bookings including

the Organization of American Historians who moved to San Jose and theSan

Francisco Business Times'meeting moved to the Oakland Convention Center.

A contract proposal that San Francisco hotel owners hoped would end an

11-month labor dispute was rejected on July 13. Negotiations will resume

on August 10, 2005. Primary Impact: Profitability

5. Enhanced Security Measures �The U.S.�s plan to tighten restrictions

on entering the country is anticipated to create challenges regarding future

overseas demand. The California tourism industry will face challenges as

Visa Waiver Program (�VWP�) countries will be required to produce passports

with digital photographs by October 26, 2005. On this date, all VWP countries

must also present an acceptable plan to begin issuing integrated circuit

chips, or e-passports, within one year. This announcement relates to the

Enhanced Border Security and Visa Entry Reform Act of 2002 requirement

that any passport issued after October 26, 2005, and used for VWP travel

to the U.S., must include a biometric identifier based on applicable standards

established by the International Civil Aviation Organization. Approximately

15 million VWP travelers visited the United States in 2004, representing

a significant percentage of total visitation to theU.S. Primary Impact:

Demand

6. Bigger and Better Amenities �Consumers want convenience, luxury

and, as leading hotel companies have discovered, amenities. From bedding

to iPods, the hotel industry is anticipated to spend approximately $4.1

billion this year on renovations and upgrades, an increase of approximately

37% from 2004. Many leading hotel chains have introduced new bedding packages

in an effort to compete with Westin�s successful �Heavenly Bed�campaign.

Westin launched its fitness initiative in November 2003, custom designing

fitness facilities and creating private workout rooms. Hyatt Hotels, in

an effort to create an amenity niche, is partneringwith XM Satellite Radio,

installing the radios in more than 50,000 Hyattguestrooms nationwide.Primary

Impact: Profitability

7. Exchange Rates �The U.S. tourism industry has benefited in

an increase in international tourism due to the weakening dollar. Although

the dollar is anticipated to appreciate throughout the remainder of 2005,

the current exchange rate remains low in comparison to rates at the beginning

of the decade. The result of the weakened dollar has been an increase in

overseas travel to major U.S. metropolitan markets and an increase in domestic

travel due to higher costs of international travel. With the combination

of stronger international buying power, more affordable transatlantic airfares,

and the addition of international flights, the California Tourism Department

anticipates 4.8% growth in overseas travel in 2005.Primary Impact: Rooms

demand

8. Direct Booking �Selling rooms on third-party websites appears

to be decreasing because hotels are providing limited inventory. Efforts

by hotel operators to guaranteethe best rate to consumers is reinforced

by a recent survey by Consumer Reports that found rates to be comparable

between third-party sites and hotel-operated sites. Also, because consumers

receive additional benefits by booking directly through a hotel website

(reward points, fewer restrictions, etc.), booking via third-party sites

appears to be declining. In 2004, the number of direct booking through

brand websites increased substantially as brand websites gained share compared

to third-party merchant and opaque websites. According to eTRAK, brand

websiteswere the source of 71.4% of the brands�centrally booked Internet

reservations in 2004, compared to 66.5% in 2003. Merchant websites, such

as Expedia, Orbitz and Travelocity, accounted for 8.6% of Internet reservations.Primary

Impact: ADR and profitability

9. State funded tourism �Many states have increased tourism marketing

budgets as the hotel industry continues its recovery. According to the

Travel Industry Association of America (�TIA�), states will spend more

than $600 million this year to promote their attractions. In July 2005,

Governor Arnold Schwarzenegger signed the fiscal budget for 2005-2006 restoring

the $7.3 million in public tourism marketing funds to the California Travel

and Tourism Commission. Although California�s funding for 2005-2006 falls

shorts of the budgets of two of its major competitors in 2003-2004, Hawaii

($56 million) and Florida ($25 million), the governor�s decision is anticipated

to increase California�s ability to market its tourism industry to potential

domestic and international travelers. Primary Impact-Rooms demand

10. Native American Gaming �California tribes continue to expand

casinos faster than any other location in the nation. In 2004, approximately

405 Indian casinos employed 539,000 workers, paying $19.4 billion in wages

and generating $6.2 billion in taxes for the entire U.S. Californialed

the states with $5.3 billion in revenue, representing 28% of the nation�s

Indian gaming revenue. On June 21, 2004, Governor Schwarzenegger announced

a set of compacts with five leading gaming tribes. Thecompacts preserve

the tribes' monopoly on casino-style gambling and the tribes may exceedthe

current limit on the number of slot machines, but must pay increasingly

more to do so. Primary Impact: Lodging demand

San Francisco

Lodging Market Analysis

�The economic conditions in San Francisco are improving. The city�s

unemployment rate has steadily decreased throughout the year to a low of

4.5% in May. According to the California Employment Development Department,

San Francisco�s unemployment rate has decreased at a greater rate than

the State�s overall unemployment rate, which declined from 6.3% in May

2004 to 5.3% in May 2005. Improving economic conditions have benefited

the hospitality industry, contributing to increased occupancy rates and

RevPAR over 2004 levels. According to STR, occupancy increased approximately

2.1 percentage points to 67.6% year-to-date June 2005 vs. the same period

last year, while ADR increased approximately 3.3% to $122.52 year-to-date

June 2005 vs. the same period last year.

�The San Francisco International Airport�s passenger traffic count increased

6.8% for year-to-date April 2005 vs. the same period the previous year.

Oakland International Airport and Mineta San Jose International Airport

have experienced a 3.4% increase and -2.2% decrease in passenger traffic

for April, respectively. The lodging market is experiencing growth from

domestic markets, such as NewYork and Chicago, and international markets,

particularly Japan and Western Europe which is anticipated to remain strong

through 2006.

�According to the San Francisco Convention Center, the number of meetings

and conventions booked in 2005 is anticipated to increase 4% vs. last year,

in the wake of a trend of shorter but more frequent conventions. The convention

center met the estimated budgeted revenue in 2004 and anticipates increased

growth in the upcomingfiscal year.

.

.

�At the end of the second quarter in 2004, the San Francisco Convention

and Visitors Bureau launched a new marketing and branding campaign titled,

�Only in San Francisco,�in an effort to enhance the city�s tourism industry.

Businesses such as local magazines, television and radio stations, outdoor

media companies, and San Francisco International Airport have committed

more than $1.2 million in local advertising space and time to the new campaign.

�Only in San Francisco�extends beyond traditional advertising to include

uniquetour packages, �Only in San Francisco, Only with Visa�offers, exclusive

deals with See�s Candies, and �Wish You Were Here�sweepstakes.

�According to the National Association of Realtors, the commercial real

estate market in the Bay Area is improving as vacancy rates continue to

decline and rents increase in all fourcommercial market sectors. Cushman

& Wakefield reported a decrease in San Francisco�s overall citywide

office vacancy from 18.0% during the first quarter of 2005 to 17.3% at

second quarter, while the CBDdropped from 16.4% to 15.5% over the same

time period. In addition, over the past two quarters CBDClass A direct

rental rates increased 6.0% to $32.28 per squarefoot .

�The Port of San Francisco is in the process of constructing the International

Cruise and Bryant Street Pier Project. This $400 million mixed-use project

is anticipated to feature a state-of-the-art international cruise terminal

facility, luxury residential condominiums, office and retail commercial

developments, and a waterfront park known as Brannan Street Wharf Park.

Construction is slated for completion in late 2006.This development is

anticipated to accommodate the growing cruise ship business. The Port of

San Francisco officialsnote there has been a 120% increase in the number

of cruise ships docking here and a 213% increase in the number of passengers

since 2001.

�Signs of economic recovery are emerging in Silicon Valley as entrepreneurs

and technology companies move into new businesses and markets and focus

on biotechnology, life sciences, healthcare, and nanotechnology. Examples

of Silicon Valley�s adaptability include Apple Computer�s rebirth as a

consumer electronics giant, Yahoo�s evolution from Internet directory to

entertainment portal, and Google�s creation of an online advertising model

to compete with traditional media businesses. Profitable results observed

from this restructuring include Google's stock price tripling from its

initial public offering last summer and Apple�s six-fold earnings increase

for the first quarter of 2005. However, the economy of Silicon Valley has

encountered mixed results. The Employment Development Department of California

states the number of jobs in Santa Clara County remains down 20% percent

since 2000 and the number of commercial real estate vacancies remains high.

Retail sales havegrown to approximately $6.48 billion in 2004 from $6.13

billion in 2003 and the nation�s highest housing prices have continued

to climb. Venture capitalists in start-up companies placed $7.4 billion

into 724 companies in 2004, representing an increase of 17% from 2003.

�The biotech industry should continue to be a major travel demandgenerator

for the Bay area throughout 2005, particularly due to the California Institute

for Regenerative Medicine�s (�CIRM�) decision to locate its headquarters

in San Francisco. The CIRM was created in November after voters approved

a measure allowing California to borrow $3 billion to fund human embryonic

stem cell research over 10 years. The institute plans to build a 17,000-square-foot

office with a maximum of 50 employees who will help give nearly $300 million

in research grants annually for 10 years. CIRM is anticipated to give San

Francisco increased scientific and marketing prestige and to generate new

biotechnology companies which may settle nearby.

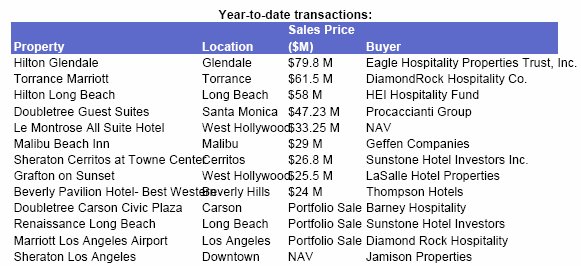

�According to the Atlas Hospitality Group, Northern California led the

state with the largest number of hotel transactions completed during 2004,

and it is anticipated that 2005 will follow a similar pattern. The San

Francisco market posted a 23.5% increase in individual sales, yet experienced

a decline of 7.4% in the median price per room. According to Jones Lang

LaSalle Hotel�s recent Hotel Investment Sentiment Survey, this competition

for assets has shifted the cap rates down to their lowest level with San

Francisco reporting a market-wide cap rate of 8.2%, as compared to the

average of 8.9% for the top 18 U.S hotel markets.

�The addition of several new luxury properties to the San Francisco

market is anticipated to increase the ADR in the upcoming years; however,

the increase in ADR may be offset by a decrease in occupancy given the

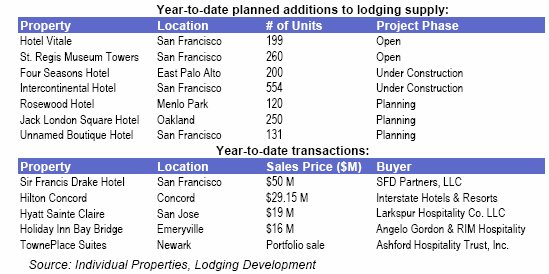

significant amount of new lodging supply. In March 2005, Hotel Vitale added

eight suites, six studios, and 185 guestrooms. This luxury boutique hotel

is part of the city�s Embarcadero redevelopment, which has included the

highly successful transformation of San Francisco�s Ferry Building into

the city�s newest landmark, a thriving bazaar of artisan food shops, restaurants,

and a thrice-weekly Farmers Market. The St. Regis Hotel and Residences

San Francisco will open in July and add 260 rooms and102 private residences.

The 40-story tower in the heart of the Yerba Buena Gardens district will

be home to a five-star restaurant, a 13,700-square-foot luxury spa, a combined

total of 22,000 square feet of indoor/outdoor meeting space and the Museum

of the African Diaspora. In addition, Four Seasons will open a 200-room

hotel in East Palo Alto later this year as the centerpiece of the prestigious

new University Circle complex which will also include three six-story office

buildings,15,000 square feet of retail space, and a parking structure that

will accommodate 1,820 vehicles.

Los Angeles

Lodging Market Analysis

�According to Los Angeles Economic Development Corporation (�LAEDC�),

Southern California�s economy is anticipated to gain momentum through 2005.

Despite increasing gasoline prices, tourism in Southern California is anticipated

to improve throughout 2005. During the first half of 2005, overall hotel

occupancy and ADR for Los Angeles reached 74.7% and $102.44, respectively,

compared to 71.7% and $95.81 during the same period last year. The 50th

anniversary celebration at Disneyland and a King Tut exhibit in Los Angeles

are anticipated to attract additional travelers to the Los Angeles area.

�According to LAEDC, the international trade industry is poised to experience

a 14.9 percent increase in two-way international trade through California�s

three customer districts�San Francisco, Los Angeles, and San Diego. It

is estimated that the international trade industry may reach a record high

of $402.4 billion in 2004. Furthermore, the Los Angeles Customer District

is anticipated to reach a record high of $270.1 billion in 2004.

.

�Los Angeles World Airports (�LAWA�) anticipates significant increases

in domestic and international passenger volume during the summer, forecasting

approximately 18.5 million travelers to pass through LAX between Memorial

Day and Labor Day, representing a 6% increase over the same period last

year. Ontario International Airport is also anticipated to set a summer

record with approximately 2 million travelers, representing an increase

of 4% over the same period last year. The record number of international

passengers at LAX during the first quarter of 2005 is anticipated to continue

through the summer travel season with international passenger traffic estimated

at approximately 5.1 million anticipated for this summer, representing

an increase of 10% over the same period last year.

�The $11 billion expansion plan for LAX was approved by the Los Angeles

City Council on October 21, 2004. The construction will be completed in

phases with the initial $3 billion expansion anticipated to increase the

current passenger capacity of LAX by 30% to approximately 78 million passengers

annually. In May 2005, the Federal Aviation Administration issued the Record

of Decision, approving the LAX Master Plan and permitting construction

bids be submitted. The remaining $8-billion expansion will undergo separate

environmental testing before final approval is granted.

�The 97-year-old Port of Los Angeles is currently undergoing an expansion

andfacelift called the Bridge to Breakwater Waterfront Development. The

San Pedro Waterfront and Promenade Master Plan is a long-term plan to turn

400 acres of Port property from industrial space into parks, public waterwaysand

recreation facilities. The development, which broke ground in February

2004 with a 10-year timeline, is anticipated to allow the Port of Los Angeles

to be a user-friendly port for cruise-ship passengers and will cover approximately

400 acres along eight miles of the coast. The first phase of the expansion,

the $6 million Los Angeles Cruise Ship Promenade, wascompleted in December

2004. The second phase, the Harbor Boulevard Parkway and Gateway Plaza

project, is anticipated to be completed this summer and will connect the

World Cruise Center to downtown San Pedro. Additionally, in 2006, the new

downtown plaza at the intersection of 6th Street and Harbor Boulevard will

be constructed and is anticipated to be connected to the proposed 7th Street

Pier.

�Los Angeles, however, may be vulnerable to a growing emigration of

movie and television productions to other states or overseas, attracted

by tax breaks, financing, and other incentives. Expertspredict Los Angeles

County may lose 1,500 jobs in the entertainment industry by year-end.

�The National Football League (�NFL�) continues to pursue plans to have

a Los Angeles team in place for the 2009 season. The project has extended

its previous site selection date to thefall of 2005 due to a general lack

of proposals and the rescinding of proposals by Pasadena and Carson, leaving

the Coliseum and Anaheim as the two remaining stadium concepts. The Coliseum

has been in position to complete a deal with the league but has been stalled

by discrepancies in an agreed upon rental fee for the team; meanwhile,

Anaheim officials are optimistic their concept to build a stadium in the

Angel Stadium parking lot will be selected .

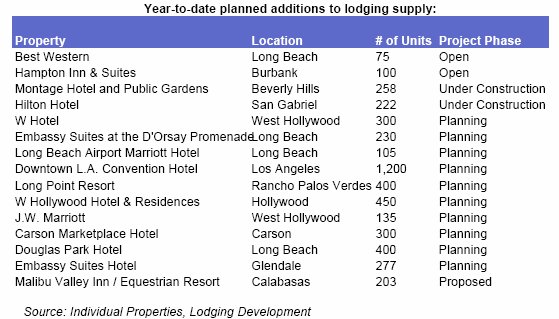

�Los Angeles is anticipated to benefit in the short term from a limited

number of new lodging properties anticipated to enter the market in the

next year. No new hotels opened in the first half of 2005; however, 11

hotels, with 874 rooms, are currently under construction throughout the

county, representinga 68% increase over the first half of 2004. The most

significant supply addition may be the $200 million Montage Beverly Hills.

In April 2004, the Beverly Hills Planning Commission approved plans for

the city�s first luxury hotel project since 1991 and is anticipated to

include a 214-room hotel and 25 private residences. Additionally, W Hotels

is anticipated to open its second Los Angeles property in 2008 at the intersection

of Hollywood Boulevard and Vine Street. The hotel is anticipated to feature

approximately 300 rooms, 150 W Residences, a signature restaurant, a rooftop

bar, a branded 9,200-square-foot spa and a 25-yard lap pool. An additional

W Hotel is anticipated to be included in the Sunset Millennium project

in West Hollywood.

�Apollo Real Estate advisors and developer Lew Wolf are developing a

1,200-room hotel and 1,000 luxury condominium residences next to the Staples

Center in downtown Los Angeles. The hotel site is owned by Anschutz Development,

which is planning an adjacent 27-acre Nokia Entertainment Center anticipated

to include a 7,000-seat theater, 40,000 square-foot plaza, 4,000-seat movie

theater, numerous shops, restaurants, and nightclubs, a television and

radio broadcast center, 5,300 parking spaces, and 4,000 condominium and

apartment units. The hotel and district are seen as essential to drawing

more business to the convention center and ground will break after the

completion of the Nokia Entertainment Center in 2007.

�The Related Companies master plan for the Grand Avenue project was

approved in May 2005. Architect Frank Gehry will design the centerpiece

40-to 50-story tower that will likely include a 275-room boutique hotel

and 200 condominiums on the upper floors and a portion of the retailmall

fronting the concert hall. The project is anticipated to break ground in

late December 2006, with completion in 2009.

�Another mixed-use development project, the Sunset Millennium, was approved

by the West Hollywood City Council in April and will begin construction

later this year. The project�s eastern parcel, at Sunset Boulevard and

La Cienega Boulevard, will be the site of a W Hotel and a J.W. Marriott.

Anaheim/Orange

County Lodging Market Analysis

�Travel to Anaheim/Orange County is anticipated to remain strong in

the coming years due to Disneyland, popular luxury coastal resorts and

increasing convention demand. Through mid-year 2005, John Wayne Airport

demonstrated a strong increase in the number of passengers, demonstrating

an increase of 6.3% YTD through April 2005 vs. thesame period the previous

year. In 2004, 42 million people visited Orange County and spent approximately

$7.3 billion, an increase from $6.8 billion in the previous year.

�Anaheim�s largest demand generator, Disneyland, began celebrating its

50th anniversary celebration on May 5, 2005. Disneyland, which attracts

more than one million people to Southern California each year, is anticipated

to spend approximately $150 million to promote the 18-month anniversary

celebration.

�Though Orange County is primarily known as a leisure destination, Anaheim

continues to establish itself as a premier convention city. The Anaheim

Convention Center experienced an increase in attendance of approximately

1.3% from 2003 levels to approximately 1,175,990 attendees in 2004. The

669 meetings/conventions held in Orange County during 2004 generated approximately

$1.6 billion in visitor spending. The number of conventioneers is anticipated

to remain strong throughout 2005 and into 2006.

.

.

�Orange County�s top coastal resorts, hotels, shopping centers, and

golf courses have united to form a premiere leisure and business destination

called the OCeanfront. Using the popularity of �The OC� television

show in their brand name to create an image of fine living, the coalition

of these beachfront communities is anticipated to increase recognition

to the area. The partnership�s goal is to increase the average length of

stay in the county from approximately 3.8 days while increasing hotel occupancy

andADR.

�Several hotels are currently undergoing extensive renovations asarea

hotels continue to promote the image of a luxury leisure destination to

travelers. The Hyatt Regency Newport Beach recently completed a $12-million

renovation to update its rooms, restaurants and meeting space, while the

Hyatt Regency Orange County recently completed a $52-million renovation

including a $7.5-million transformation of the South Tower guestrooms.

The Newport Beach Marriott Hotel and Spa is in the process of a $60 million

makeover, anticipated to open in November 2005 and include 20 new luxury

suites. Additionally, the Ritz-Carlton Laguna Niguel is anticipated to

complete a $40-million renovation by the end of the summer, while the Coast

Anaheim Hotel is anticipated to undergo a major renovation of its 490 guestrooms

and be renamed the Sheraton Anaheim Hotel by the end of 2006.

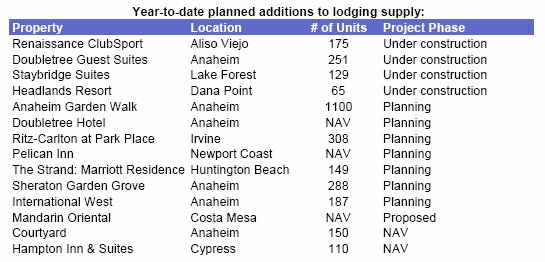

�Due to the continually increasing costs of construction and landacquisition,

a limited amount of new lodging supply is anticipated to come online in

2005. Hotels anticipated to open during the second half of 2005 include

the 251-room Doubletree Guest Suites in Anaheim and the 129-room Staybridge

Suites in Lake Forest. Atlas Hospitality Group reports, however, an approximately

27% decrease in the number of Orange County hotel projects in various stages

of planning, from 15 at mid-year 2004 to 11 in 2005. Further significant

lodging supply additions include:

-

The Garden Walk complex in Anaheim which includes the development of three

hotels. Though the project has been delayed for several years, phase one

is anticipated to be completed by 2007 with construction of the hotel following.

-

A Renaissance Club Sport Hotel in Aliso Viejo, anticipated to contain 175

guestrooms, a 67,300 square-foot sports club, and 4,000 square feet of

conference space. The project is anticipated to be completed in 2007

-

The CIM Group�s project called the �The Strand,�located at downtown Huntington

Beach (formerly known Blocks 104 & 105), is anticipated to open in

the summer of 2006.This mixed-use project will include 102,000 sf of retail,

restaurant, and entertainment, plus a 149-room Marriott Residence Inn along

the pier in Huntington Beach.

-

Makar Properties�s Pacific City is anticipated to open in the spring of

2007 and contain a 400-room boutique hotel.

San Diego

Lodging Market Analysis

�Although San Diego has ranked as the top-performing lodging market

in California and one of the top markets in the United States, its hold

on the market share may decline with consecutive tourism budget cuts, anticipated

flattening demand, decreases in international flights to the San Diego

area, and 2.5% growth in hotel room supply. Lodging fundamentals, however,

were healthy YTD through June compared tothe same period last year, with

a 0.7 percentage point increase in occupancy to 72.4% and an 8.0% increase

in ADR to $120.31, resulting in a 9.2% increase in RevPAR to $87.11.

�California Tourism and Travel Commission anticipates growth potential

in Southern California to remain strong as demand generators remainplentiful.

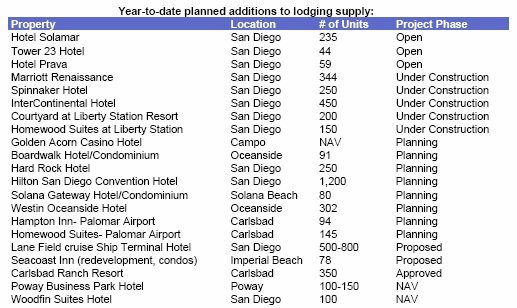

San Diego has seen a significant amount of new hotel activity during 2005.

The lodging market may experience strained lodging fundamentals in the

coming years due to the significant amount of new lodging supply, including

the opening of three new hotels during the first six months of 2005, representing

817 rooms as well as an increase of 3.4% over the same period last year.

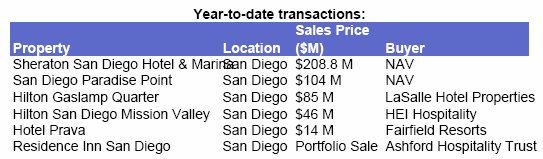

�In addition to new hotel construction, numerous hotels have recently

changed hands, including the sale of the 192-room Residence Inn Mission

Valley for $37.2 million in 2004, two additional hotel sales for a total

of$131 million, and four others reportedly valued at $240 million. Four

high-profile hotels are currently for sale, including the 421-room Hyatt

Islandia on Mission Bay, the 206-room Shelter Pointe Hotel, the 261-room

W Hotel San Diego, and the 281-room Marriott Del Mar.

�The San Diego lodging market continues to benefit from the growth of

the bio-technology and defense industries. Demand for high-technology jobs

in San Diego appears to be approaching 2000 levels, as the last six months

have shown a noticeable increase in hiring. A study performed by the Milken

Institute in June 2004, ranked San Diego as the largest biotechnology job

market out of the major metropolitan areas of the United States, with approximately

56,000 jobs in the industry and approximately $5.8billion in yearly income.

Although the biotech industry has experienced fallout due to recent drug

recalls of Vioxx and Bextra, safety warnings, and previous purchasing of

facilities, signs of a growing market still exist.Genentech�s announcement

in June to buy Biogen Idec�s newly built Oceanside drug facility for $408

million is anticipated to strengthen the industry throughout the San Diego

area.

.

.

�San Diego is now playing a larger role in the defense industry than

it has in the past, following an increase in federal spending on defense

and homeland security. In particular, Los Angeles-based Northrop Grumman

has acquired three defense-related businesses in the San Diego area over

the past couple ofyears, starting with their acquisition of Ryan Aeronautical

in 1999. Since then, Northrop has also taken over TRWand Newport News Shipbuilding,

acquiring some 4,300 employees in the San Diego area. The company plans

to add upwards of 700 more employees throughout 2005 which is anticipated

to bring more people, meetings, and money to the local market. �San Diego

International Airport is the busiest, single-runway commercial airport

in the nation, and in 2004, annual passenger traffic reached a record approximately

16 million passengers. Due to continued increased traffic, the airport

is quickly running out of space and anticipated to exceedits capacity be

2012. In June 2005, the operators of San Diego International Airport have

decided tomake Terminal 2 the focal point of a proposed 10-gate expansion.

The decision initiates a state environmental review on the $536 million

project that is anticipated to take one year to complete.

�Fiscal year 2004 was the highest-performing year in the San Diego Convention

Center�s 15-year history, with 68 conventions and tradeshows hosted throughout

the year, generating an estimated 714,519 hotel room nights. Preliminary

analysis indicates that fiscal year 2005 has fallen short of 2004 levels,

with 53 conventions and tradeshows, generating an estimated 664,555 hotel

rooms nights. An impressive 71 events representing 914,717 hotel room nights

for future years were secured during the 2005 fiscal year. The events contracted

include such super groups as the National School Board Association (37,600

room nights), Digestive Disease Week (41,100 room nights) and the American

Society of Hematology (39,780 roomnights). It is anticipated that the local

lodging market and economy will receive benefits from these bookings through

2017.

�On July 15, the mayor of San Diego resigned due to continual questioning

concerning San Diego's approximately $1.37-billion pension fund deficit,

which is largely the result of decisions in 1996 and 2002 to avoid payments

to the retirement fund and enhance benefits.

�In accordance with City Manager Lamont Ewell�s proposed $858 million

budget for the 2006 fiscal year, the SanDiego City Council decreased the

San Diego Convention and Visitors Bureau�s (�ConVis�) budget by 10%, or

approximately $1 million, to $8.8 million, representing the third consecutive

year ConVis�s budget has been reduced (from a high of $13.9 million in

2002). The bureau�s proposal of an ordinance that would increase the 10.5%

nightly room tax by 2% to generate a $24 million operatingbudget failed

in two subsequent ballot propositions in 2004 . The bureau plans to increase

lobbying efforts in an upcoming ballot proposition to increase future funding.

�Centre City Development Corporation has estimated that the opening

of PETCO Park in the spring of 2004 has spurred development amounting to

$1.4 billion in downtown San Diego. Planned projects that are anticipated

to increase lodging demand to San Diego include:

-

Broadway 655, a 23-story, 365,000-square-foot office tower anticipated

to open in June 2006 and contain 17 apartments and 16,314 square feet of

retail space.

-

DiamondView Tower at the Ballpark, a 14-story, 300,000-square-foot office

building. The development is anticipated to contain 36,000 square feet

of retail and restaurant space and open in the fall of 2006.

-

A $20.6 million second phase to the Gaslamp City Square anticipated to

open in April 2006, anticipated to contain 88 condominiums, 25,000 square

feet of retail, and 250 parking spaces.

�The Chargers are proposing to build a $450-million stadium in addition

to new homes, a hotel, and some office and retail space on the 166-acre

Qualcomm Stadium site. The old stadium will be torn down after the new

stadium is completed. The Chargers have decided to circumvent the San Diego

City Council and take their proposal for a new stadium in Mission Valley

directly to voters in which they only need a simply majority for victory.

If accepted, this project is anticipated to benefit the local economy by

increasing employment, demand, and supply.

�After a purchase agreement with Lego Systems for $459.2 million,on

July 1 Blackstone Group became the official owner of four theme parks,

including Lego Land in Carlsbad.

The Ernst & Young 2005 Mid-Year Lodging Report contains an analysis

of data compiled from many sources, including Smith Travel Research. Thecontent

of this report is for reference only, not to be used as business advertisement

or to set standards on policies or actions. Ernst & Young (�E&Y�)

may have relied upon certain assumptions in calculating the figures herein

which may change. E&Y makes no representation or warranty with respect

to this report. This report is provided �as is�and may contain omissions

or inaccuracies. E&Y does not guaranteethe merchantability, fitness

for a particular purpose, title or noninfringement of this report and hereby

disclaims any such express or implied warranties. The information contained

in this report may not be relied upon and does not constitute an endorsement

or advice. E&Y and its employees, affiliatesor agents are not liable

for any decision made or action taken in reliance upon this report or for

any consequential, indirect, special or similar damages related thereto.

This report includes certain estimates and forecasts that involve risks

and uncertainties; actual results may differ materially from those expressed

or implied herein. This report is proprietary to E&Y and is protected

by copyright and other intellectual property laws.

|