|

|

|

|

|

|

|

|

|

.

| by Robert Mandelbaum, July 2005

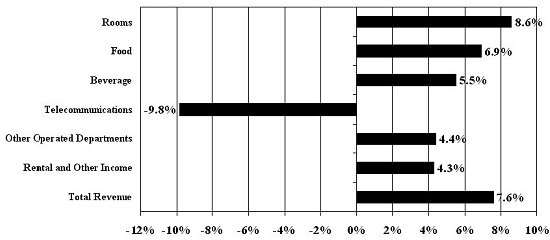

During the recent recovery of the U.S. lodging industry, much attention was given to the growth in top-line performance measurements. Numerous articles have been produced exalting the growth in occupancy and average daily room rates (ADR). After reading these analyses, one might think that the hotel industry lives on RevPAR alone. Not mentioned nearly as frequently are the gains in bottom-line profits being achieved by U.S. hotels. Analysis of movements in hotel profitability is critical in order to measure management efficiency, incentive management fees, changes in values, return on investment, debt coverage, and industry solvency. Certainly, growth in revenue is important and obviously a strong contributor to growth in profits. Management and franchise companies are acutely aware of changes in total hotel revenue since their compensation is frequently dependent on changes in this line item. However, for management companies with incentive fees, owners, investors, and lenders, the profits generated from hotel operations dictate their income. To complete its 69th annual Trends in the Hotel Industry survey of the U.S. lodging industry, PKF Hospitality Research received year-end 2004 financial statements from thousands of hotels across the nation. From these statements, we extracted and analyzed 200 distinct operating measurements. While this analysis provided us with some insight into the revenue improvements achieved in 2004, we learned even more about the changes in unit-level hotel expenses and profits. Profit Growth Outpaces Revenue Growth In 2004, the hotels in our Trends sample enjoyed a 7.6 percent increase

in total revenue, which eventually led to an 11.4 percent growth in operating

profits. This marks the first year of unit-level profit growth since

2000. For reference purposes, the typical hotel in our Trends sample

suffered a 36.1 percent drop in profitability from 2000 to 2003.

This indicates that U.S. hotels still have some ground to make up to achieve

recovery at the bottom line. For the purposes of this analysis, hotel

operating profits are defined as the net income before deductions for capital

reserves, rent, interest, income taxes, depreciation, and amortization.

Annual Changes In Revenue 2003 to 2004  Unit-Level Change From 2003

Source: PKF Consulting In general, it appears that the larger hotels with higher room rates experienced the greatest increases in profitability during 2004. Of course, these properties were some of the most severely impacted during the 2001-2003 industry recession and therefore have the greatest losses to recoup. Of all the different property categories, resort hotels achieved the greatest increase in profitability in 2004. With total revenue growing 9.0 percent, operating profits in this hotel segment grew 17.2 percent. On the other hand, profitability for limited-service hotels experienced a gain of only 6.2 percent. All other property types (full-service, suite, and convention hotels) saw their profits grow in excess of 10 percent in 2004. Expense Growth Mutes Profit Growth While 11.4 percent growth in profits is welcome news to those that benefit most from the bottom line, this level of profit improvement is somewhat disappointing relative to the pace of revenue growth. Back in the late 1990s, 7.0 to 9.0 percent growth in revenues produced 14.0 to 16.0 percent growth rates in profitability. The main reason for this relative under-achievement is the 6.4 percent growth in hotel operating expenses observed in 2004. Separate studies conducted by PKF Hospitality Research found that a spike in operating expenses is common during the initial stages of an industry recovery. The hiring of staff to match the increased business volume, combined with the reinstitution of services and amenities that had been eliminated to cut costs, are the main reasons for this anomaly in operating expense growth. Once again, labor was the single largest expense item for U.S. hotels, averaging 45.6 percent of all dollars spent to operate a typical property. In total, all labor-related costs grew 6.3 percent in 2004. Of note is the fact that salaries and wages grew 5.5 percent, while employee benefits grew 8.9 percent. With many employee benefits mandated by the Government, this is a difficult expense for hotel managers to control. Those departments with the highest labor component also experienced the greatest percentage increases in total costs. Contrary to labor costs, it appears that hotel insurance costs have

started to stabilize. On average, the hotels in our Trends sample

paid 1.8 percent less for property and general liability insurance in 2004

than they did in 2003. Of course, this expense has doubled for hotels

since 1999.

Annual Changes In Select Operating Expenses 2003 to 2004  .

In previous articles, we have described the typical hotel industry �market recovery� scenario, in which occupancy rates begin to rise, followed by room rates. This is what has occurred in recent years, as in 2004 when occupancy increases drove RevPAR gains. However, ADR growth should dominate RevPAR improvements in 2005. Looking at historical �financial recovery� patterns for the lodging industry, we find revenue gains matched with expense growth during the initial years of an industry upturn. The strongest gains in profits usually begin occurring in the third or fourth year of recovery. Based on these analyses, PKF Hospitality Research projects stronger profit growth in 2005 (14% - 16%) than that observed in 2004. However, it may not be until 2006 or 2007 that U.S. hotels match the profit margins and dollars achieved in the late 1990s. Robert Mandelbaum is the Director of Research for PKF Hospitality Research, the research affiliate of PKF Consulting. He works in the firm�s Atlanta office. To purchase a copy of the 2005 Trends in the Hotel Industry report, please visit www.pkfc.com, or call (404) 842-1150, ext 237. |

|||||||||||||||||||||||

| Contact:

Robert Mandelbaum

|