|

|

|

|

|

|

|

|

Turn Around in 2004 after Three Consecutive Years of Declining Revenues - Estimating 9% Increase in Conference Attendance in 2005 |

.

| Atlanta, May 23, 2005: Conference Centers in the United States saw

their financial fortunes turn around in 2004 after three consecutive years

of declining revenues and profits. When looking forward to the remainder

of 2005, most center managers are expecting even greater improvements in

performance. This finding comes from data collected for the recently released

2005 edition of Trends in the Conference Center Industry, published by

PKF Consulting (PKF-C) in conjunction with the International Association

of Conference Centers (IACC).

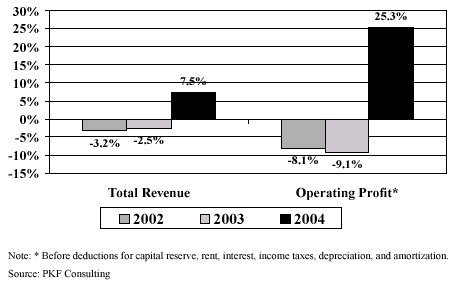

�As a whole, our Trends in the Conference Center Industry sample enjoyed a healthy 7.5 percent increase in total revenue in 2004,� said David Arnold, eastern regional chief executive officer of PKF-C. �Operating under fairly austere conditions after three years of declining revenue, center managers were able to convert the gain in revenue into a 25.3 percent boost to the bottom-line in 2004.� �The best news is that conference center managers appear to be even more optimistic about 2005,� Arnold noted. The conference centers in the survey sample have budgeted for an average increase in occupancy of nine percent in 2005, matched by a 4.0 percent increase in package pricing. For conference centers, most business is sold in packages that include accommodations, meals, and conference services. The Return Of Conferences On average, conference demand increased 4.3 percent in 2004. �It is the return of this �core� conference demand segment that gives center managers the confidence to raise rates in 2005,� Arnold concluded. Conference centers are specialized lodging facilities that thrive on small to mid-sized business conferences. In 2004, conference demand represented 63.8 percent of the room nights occupied at conference centers, as opposed to transient leisure and business travelers. Business organizations (32.5 percent) and academic institutions (30.0 percent) were the primary sponsoring organizations of these conferences. Conference centers have always prided themselves on their unique ability to provide a productive learning environment. Therefore, it is no surprise that 47.5 percent of all conference center groups met in 2004 for the purpose of training or continuing education. Other meetings focused on management planning (20.4 percent) or professional / technical conferences (18.2 percent). Local And Loyal Demand Tight corporate meeting budgets not only reduced the number of conferences

held during the recession, but it also limited the amount of travel for

which companies were willing to pay. As a result, conference centers found

themselves increasingly dependent on local corporations for business. �We

still enjoyed strong demand for locally generated meetings in 2004, but

the growth segments for the year were national and regional groups,� Arnold

said. �In 2004, local organizations were responsible for 48.2 percent of

the groups meeting at conference centers. However, the number of local

groups actually declined by 3.0 percent from 2003 to 2004. Concurrently,

the number of meetings booked from regional or national sources grew by

roughly 2.4 percent.�

Annual Change in Revenues and Profits*  When attempting to find business to book, conference center sales staffs ranked repeat customers and personal sales calls as the two best sources of qualified leads. �Apparently there is a high degree of loyalty and satisfaction among groups that use conference centers. When using a conference center, the success of achieving a meeting�s stated goals counts for more than just the hard dollar R.O.I. Conference centers truly provide an environment that is conducive for a successful meeting,� Arnold surmised. The 2005 Trends in the Conference Center Industry report provides a statistical and financial profile of the conference center industry. In addition, it presents information on facilities offered, package pricing and occupancy statistics, source of meetings, marketing tactics, and human resources. Data is presented for Executive, Corporate, Resort, and College/University centers and is a standard reference resource for conference center owner and managers, as well as meeting and convention planners. Copies of the 2005 Trends in the Conference Center Industry report are available for purchase at PKF�s online store at www.pkfc.com, or by calling Claude Vargo toll free at (866) 842-8754. PKF Consulting, headquartered in San Francisco, is a consulting and real estate firm specializing in the hospitality industry. PKF Consulting has offices in New York, Philadelphia, Washington DC, Atlanta, Indianapolis, Houston, Dallas, Los Angeles, and San Francisco. |

||

| Contact:

David Arnold

|