|

|

|

|

|

|

|

|

|

Partners on the Same Path? UNITE HERE Report |

.

| October 7, 2004 - FelCor Lodging Trust [FCH] has had a close relationship

with InterContinental Hotels Group since 1998. FelCor�s merger that year

with Bristol Hotels left it with a substantial portfolio of Holiday Inn-

and Crowne Plaza-branded properties managed by InterContinental�s predecessor,

Bass Hotels. It also gave InterContinental a large equity stake in the

FelCor REIT, now amounting to about 17%.

The long-term effects of this relationship have been mixed, particularly for FelCor�s independent investors. On the one hand, the Bristol merger allowed FelCor to emerge as one of the country�s largest hotel owners. On the other hand, the merger left FelCor with some substantial disadvantages. Numerous hotels were bound under management agreements that limited FelCor�s ability to reposition its management and brand portfolios. Moreover, it reoriented FelCor�s portfolio toward brands that since 1998 have underperformed their peers. While FelCor�s management has taken steps toward reducing some of these negative factors � including the recent renegotiation of several InterContinental operating agreements, and ongoing asset sales [1] � investors should question whether FelCor�s ongoing relationship with InterContinental is in their best interests. In the following pages, we examine two different aspects of FelCor�s relationship with InterContinental, and ask the following question: is InterContinental�s performance as a management company adequately serving investors? In the first section, we compare the performance of FelCor�s InterContinental-branded hotels with that of other hotels in this company�s portfolio. This comparison highlights the fact that FelCor�s InterContinental hotels have seen diminishing performance over time, compared to properties flagged by other management companies. Given this trend, we question whether InterContinental Hotels� brand strategy is likely to generate a turnaround for FelCor�s assets. In the second section, we look at the strike/lockout currently affecting two FelCor properties in San Francisco, which are represented by UNITE HERE Local 2. We argue that this strike/lockout is imposing some substantial costs on hotel owners such as FelCor, even while the issues that underlie the dispute are of concern primarily to hotel operators such as InterContinental. These two perspectives into FelCor�s relationship with InterContinental Hotels raise the question of whether the latter�s performance as an operator and brand manager has been in FelCor�s best interest. In light of this, we urge investors to seriously examine the long-term value of FelCor�s relationship with InterContinental. InterContinental-branded properties are underperforming

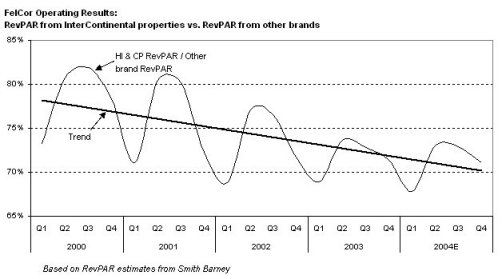

While the InterContinental-branded hotels� disproportionately low operating

profits are in part attributable to their lower-end market segment, a comparison

of these properties with those under different flags shows an interesting

trend. As the chart below illustrates, the ratio of InterContinental-brand

RevPAR to that of other brands has declined noticeably over the past four

years. In 2000, RevPAR at InterContinental-branded properties averaged

approximately 79% of the RevPAR at FelCor�s other properties. In 2004,

this same ratio is expected to average just 71%. In other words, the relative

performance of the InterContinental properties has diminished substantially

compared to the rest of FelCor�s portfolio.

FelCor�s second quarter results indicate that the company�s InterContinental-branded hotels continue to struggle. Holiday Inn properties posted RevPAR performance still well below industry segment benchmarks [3] . Meanwhile, Crowne Plaza hotels recovered substantial occupancy � 9.9% over Q2 2003 � but only at the expense of anemic ADR growth (0.3%). The question for investors, then, is whether InterContinental�s market strategy is likely to yield a significant turn-around for the 44% of FelCor�s portfolio branded under Holiday Inn and Crowne Plaza flags. As the recent resignation of CEO Richard North suggests, InterContinental�s focus may indeed be shifting [4] . The first hotel in its new �Indigo� chain is scheduled to open in Atlanta later this year, and the company will likely devote considerable attention to this launch � possibly at the expense of its other flags. Moreover, the company appears to be in the process of further developing the �InterContinental� brand as its premier full-service brand. However, it is unclear to us that this change in focus is likely to be of direct benefit to FelCor investors. While FelCor may be able to convert some of its urban properties to the new, albeit untested, Indigo brand, it will only be able to do so at the cost of further substantial capital expenditures. The implications for Crowne Plaza of a further developed �InterContinental� brand, meanwhile, remain uncertain. FelCor�s 1998 absorption of Bristol has therefore had mixed results. While through this merger FelCor became the second largest hotel REIT in the US, this growth came at the cost of a heightened dependency on the midscale with F&B market, and on the Holiday Inn brand in particular. Moreover, it had the effect of giving a substantial equity stake (currently about 17%) to a company whose interests may not be precisely aligned with those of other FelCor investors. The San Francisco strike/lockout Events surrounding the recent strike and lockout at two FelCor-owned hotels in San Francisco highlight how InterContinental�s interests and market strategies may be in conflict with those of FelCor and its other investors. This strike/lockout, which may cause FelCor diminished operating results, hinges around questions of primary interest to hotel management companies. Investors should question whether this reduced performance will generate any upside to hotel owners such as FelCor. UNITE HERE Local 2, which represents approximately 88% of San Francisco�s upscale hotel market, has been engaged in contract negotiations at fourteen major properties, seeking to renegotiate a contract that expired on August 14. These fourteen hotels are negotiating as part of the San Francisco Multi-Employer Group (MEG). InterContinental Hotels & Resorts operates five of the fourteen MEG hotels, and is a key player in the group�s negotiations. Two of these five hotels are FelCor-owned properties: the Crowne Plaza Union Square and the Holiday Inn Fisherman�s Wharf. On September 27th, workers commenced a limited two-week strike at a subset of four MEG hotels, including the Crowne Plaza Union Square. Local 2 announced that its members would return to work unconditionally after two weeks, and that it was seeking the resumption of good-faith bargaining by both parties. Nevertheless, on September 29th, operators of the other ten MEG hotels, including the Holiday Inn Fisherman�s Wharf, initiated a worker lockout. InterContinental and the other MEG hotel operators on Tuesday announced that the lockout will extend indefinitely past the original two-week timeline [5] . Among the key issues in this dispute are several that appear of principal interest not to hotel owners, but rather to operating companies � particularly, the term of the new contract. The union has proposed a contract that would expire in 2006, the same year as hotel contracts in several other North American cities. The union�s express goal this contract term is to engage hotel operators on topics of national relevance, such as national health care costs, laws affecting immigrant workers, and so forth. While the issues at stake are of broad importance to both the union and to management companies, they are not of immediate financial concern to real estate owners, particularly those with low concentrations of union employees. In our opinion, Intercontinental has not effectively articulated its opposition to a contract expiring in 2006, however we speculate that they are concerned that managerial flexibility will be constrained by such a contract. Compared with industry leaders such as Hilton and Starwood, FelCor has a relatively small number of unionized employees. About 9% of FelCor�s rooms are in union-represented hotels, with concentrations at InterContinental-branded properties. It is not at all clear how this flexibility benefits Felcor or other owners. Yet it is hotel owners, including FelCor, that are incurring significant the costs of the management companies� negotiating position. The San Francisco Bay Area, for example, is one of 3 urban markets in which FelCor has substantial concentrations � the others are Atlanta and Dallas. Together these three markets make up 21% of operating profits [6] . Given current market trends, the union estimates that the two hotels in San Francisco could account for approximately $35-40 million revenue in 2004, or about 3% of the company�s total. A prolonged lockout could cost FelCor around 1% of total corporate revenues � or $4 to $6 million in revenues over six months. [7] Beyond the immediate economic impact to FelCor, this lockout may also affect long-term operations of FelCor�s San Francisco assets. Over the past 10 years, the multi-employer group in which FelCor�s two properties participate has been engaged in a labor-management partnership with the union. This partnership has yielded productivity initiatives that have been of significant value to the hotels� bottom line [8] . FelCor�s Crowne Plaza Union Square, for example, was able through this partnership to pioneer a new and successful food and beverage model that would have been impossible under a traditional labor contract. At the Holiday Inn Fisherman�s Wharf, meanwhile, the company was able to achieve operating efficiencies that likewise would have been impossible outside the labor-management partnership. The current lockout has put the future of such labor-management partnerships in serious doubt. Conclusion The indefinite lockout initiated by InterContinental at FelCor�s two San Francisco properties has the potential to cause the REIT substantially diminished operating results. However, it is not at all clear to us that FelCor stands to gain much upside from the dispute. We believe that InterContinental�s interests in the dispute are markedly different from those of FelCor, and that the REIT may pay a steep price for InterContinental�s negotiating position. In the context of the diminishing performance at FelCor�s InterContinental-branded properties, relative to the rest of the company�s portfolio, we question whether FelCor�s relationship with InterContinental has benefited the REIT over the long-term. In light of these facts, we urge investors to question the continuing value of FelCor�s relationship with InterContinental Hotels. * Owned by FelCor Lodging Trust

[1] FelCor�s most recent SEC 10-K filing states: �Although we amended our IHG management agreement to extend contracts for 27 hotels in exchange for a $25 million credit to apply to the satisfaction of the termination fees due from the sale of 35 of our IHG managed hotels, the sale of other IHG managed hotels will still trigger termination fees or reinvestment requirements. Additionally, following the full utilization of this credit, which we currently expect to occur during 2004, we will again be required to reinvest the proceeds from the sale of IHG managed hotels in other hotels to be managed by IHG or pay substantial termination fees.� [2] See Bear, Stearns & Co.: Global Hotels, Vol. 2, September 2003 (p. 304, 316). Bear Stearns also states, �Since the acquisition of Bristol in July 1998, the company�s portfolio has been more or less static� After the acquisition of Bristol, management�s attention turned toward improving the quality of the assets rather than continuing to grow. Since 1998, FelCor has invested more than $600 million of capital in its hotels as part of an asset repositioning, renovation, redevelopment, and rebranding effort.� (pp. 308-309). [3] See Bear Stearns 8/4/04. [4] See InterContinental Hotels Group PLC, 9/15/2004; Times of London, 9/15/2004. [5] SFMEG 10/5/2004. [6] See FelCor�s SEC 10-K, 3/15/2004. [7] Estimates are based on FelCor�s stated operating results for the San Francisco Bay Area (SEC 10-Q, 8/6/2004), and on PKF trends data. They assume a 25-50% reduction in hotel revenues resulting from the strike. [8] See Cornell Hotel & Restaurant Administration

Quarterly, April 2000.

UNITE HERE Local 2 represents 12,000 workers in the hospitality industries of San Francisco and San Mateo County. Local 2 is presently engaged in a labor dispute with 14 Class A hotels in San Francisco, including: the Argent Hotel; Crowne Plaza Union Square*�; Fairmont Hotel; Four Seasons; Grand Hyatt Union Square; Hilton San Francisco; Holiday Inn Civic Center�; Holiday Inn Express�; Holiday Inn Fisherman�s Wharf*�; Hyatt Regency; Mark Hopkins�; Omni San Francisco; Sheraton Palace; Westin St. Francis. |

| Contact:

UNITE HERE Local 2 Ian Lewis Research Analyst 415-864-8770 ext 760 [email protected] |

InterContinental-branded

hotels make up a large proportion of FelCor�s cash-flow � about 44% according

to the company�s most recent 10-Q. Yet these rooms have not generated profits

commensurate with their numbers. Holiday Inn-branded hotels, which made

up 32% of FelCor�s rooms in 2003, generated just 24% of the company�s operating

profits. Similarly, Crowne Plaza made up 12% of all rooms, but only 7%

of operating profits. By contrast, the Embassy Suites brand � which constituted

33% of FelCor�s room count � generated 48% of all operating profits.

InterContinental-branded

hotels make up a large proportion of FelCor�s cash-flow � about 44% according

to the company�s most recent 10-Q. Yet these rooms have not generated profits

commensurate with their numbers. Holiday Inn-branded hotels, which made

up 32% of FelCor�s rooms in 2003, generated just 24% of the company�s operating

profits. Similarly, Crowne Plaza made up 12% of all rooms, but only 7%

of operating profits. By contrast, the Embassy Suites brand � which constituted

33% of FelCor�s room count � generated 48% of all operating profits.