|

|

|

|

|

|

|

|

.

| by Manav Thadani, Managing Director and Deepika Malkani, Editor

- HVS International New Delhi / November 2004

Introduction The scope of this publication is to assess current trends and future opportunities for the hotel industry in India. As always, apart from conducting specific research for this publication, we have included macro data provided by the Department of Tourism. The publication briefly discusses the tourism industry in India in the context of the current economic scenario and presents the results of our survey on the performance of branded hotels, analysed by each segment of the hotel market, as well as by major cities. Our study also provides an overview of supply and demand conditions in the hotel market in India. As in previous editions of this report, we have, once again, presented our assessment of industry trends and developments; this is included as part of the �Future Trends� section. In addition to the Hotels in India�Trends and Opportunities we publish The Indian Hotel Industry Survey on an annual basis, in association with the Federation of Hotel & Restaurant Associations of India (FHRAI). This publication, the only one of its kind in India, provides detailed financial and operating information on the hotel industry, analysed by star category, across all major cities in the country. The 2003/04 edition will be available by the end of the year. This is the eight edition of HVS International�s Hotels in India - Trends and Opportunities publication. This year, 211 hotels, having a total room count of 28,870 rooms, participated in our research. The survey does not take into account any of the ITDC hotels, resulting in a decline in the total number of participating hotels (compared to 2003). However, overall room count has increased, reflecting the opening of new hotels with large inventories. The Indian Economy - An Overview: The economy performed extremely well during 2003/04, with GDP growing by 8.2%. While agriculture accounted for most of the rebound (registering a growth of 9.1%, in response to the best monsoon in a decade), other sectors also showed a strong performance. Industry grew at above 7.0%. Services, which account for more than half of total GDP, expanded 8.7%. A key component of Services - the trade, financial services, hotels, insurance, transport and communications component -expanded by a seven-year high of 11.2% amid a credit-fuelled consumer spending spree. The economy�s buoyancy, together with initiatives by the erstwhile NDA government - to improve India�s deficient infrastructure, divest loss-making enterprises and ease restrictions on foreign investment, and perhaps most importantly, make peace with neighbouring Pakistan - did much to convince the world of India�s investment worthiness. More than $10 billion in foreign capital poured into India in 2003/04. However, this sense of bullishness has been somewhat dampened, following the NDA government�s failure to return to power in the General Elections in April-May 2004, despite having done well in state elections last year. The present Congress-led United Progressive Alliance (UPA) government�s efforts to `open up� the economy (for example, raising FDI limits in telecom, aviation and insurance, which was proposed in the recently announced Union Budget 2004-05) are being thwarted by its main ally, the Left government. There are essential ideological differences between the two main parties: the Congress is progressive in outlook and both Prime Minister Singh and Finance Minister Chidambaram have been champions of reform; the Left, on the other hand, is not in favour of liberalisation and disinvestment. This has led to a sense of uncertainty as to the course government policy will take, causing foreign investors to hold back, and wait and watch, at least for the time being. The Reserve Bank of India and leading research agencies have forecast a GDP growth of 6.0-6.5% in 2004/05, taking into account the likely adverse effects on agriculture of a late and erratic monsoon. However, recent data on first quarter (April-June) performance reveals the economy has, in fact, done better than expected. GDP growth for the period April-June 2004 is 7.4%. Agricultural production witnessed higher-than-expected 3.4% increase. Manufacturing grew at 8.0% during this period, exceeding the strong growth momentum witnessed in 2003/04. Demand for manufactured goods has, and will continue to, benefit from low interest rates, inexpensive and easily available financing options, and an overall rise in the purchasing power of India�s population, over the last number of years. The trade, financial services, hotels, insurance, transport and communications component, which accounts for 50% of the Services sector, registered an 11.0% increase. Services and Industry will continue to drive the economy in the current fiscal. Also in the economy�s favour is its health: the balance of payments position is stable, a current account surplus is forecast for 2004/05 and India�s foreign exchange reserves (US$118 billion as on September) are amongst the highest in the world. Moreover, the finance minister has strongly emphasised the government�s commitment to liberalisation and key reform initiatives, assuring that they will be implemented, `even if there is a delay�. The government is also contemplating using a part of the foreign exchange reserves (say US$10 billion) towards major infrastructure development. The new government has been concerned about inflation, which has been rising steadily over the past three months, and touched a four-year high of 8.0% (in August � September). The increase is the result of seasonal factors and the higher prices of fuels and manufactured goods. Trends & Developments in Tourism: The year 2003 was an outstanding year in terms of inbound tourism, with tourist arrivals reaching 2.73 million. The strong growth in tourist arrivals in 2003 (especially in the first half of the year) is partly attributable to the outbreak of SARS in east Asia, as well as the war on Iraq, which resulted in India being perceived as a safe region to visit. The more fundamental reason, however, relates to a strong sense of business and investment confidence in India: inspired by India�s strong GDP performance, and initiatives taken by the erstwhile Prime Minister, to make peace with Pakistan, strengthen ties with the developed world and open sectors of the economy to private sector/foreign investment. Significantly, the bulk of international arrivals in India, both in 2003 and 2004, have been business travellers. Domestic travel, both business and leisure, also benefited from a thriving economy. Prior to being voted out of power, the NDA government implemented certain important measures to provide a much-needed boost to travel & tourism. These included the abolishment of the inland air travel tax of 15%; reduction in excise duty on aviation turbine fuel to 8%; and removal of a number of restrictions on outbound chartered flights, including those relating to frequency and size of aircraft. The provision included allowing Indian charters to land at all airports in the country, and Indian passport holders to travel on inbound charters. The government also launched the Incredible India campaign, which has been successful in launching the `Brand India� image. The new government, it appears, is taking active interest in developing tourism in India. The continued Incredible India campaign has had a strongly positive impact on tourist arrivals in 2004. Definite efforts are being made to communicate the Brand India message: India made its presence strongly felt at the WTTC-promoted Global Travel & Tourism Summit held in Doha, Qatar in May this year. India has also been selected (on the basis of competitive bidding) to host the Summit next year. An important new development is the government�s recent decision to treat convention centres as part of core infrastructure, allowing the government to provide critical funding for the large capital investment that may be required. The government has identified Delhi, Mumbai and Goa as the markets to develop these convention centers, which is likely to further fuel demand for hotel rooms. Another effort is the decision to substantially upgrade 28 regional airports in smaller towns, slated to be completed by 2006. Expressions of interest have been received for the proposed privatisation (49% stake) of the Delhi and Mumbai international airports, but, as expected, the Left government has opposed the move. Substantial investments in tourism infrastructure are, undoubtedly, essential for this industry to continue to evolve and grow, and ultimately achieve its potential. The upgrading of national highways connecting various parts of India has opened new avenues for the development of budget hotels alongside. Taking advantage of this and certain other key locations is the Tata group (owners of Indian Hotel � Taj) that has developed IndiOne, a 101-room economy hotel outside Bangalore; they hope to duplicate this across India in the next few years. Another hotel chain called `Homotel�, being promoted by Sarovar Park Plaza group is also likely to compete in this new economy segment. International majors like Accor are also planning to bring in Ibis into India. The year 2004 has been a record year in tourist arrivals, as is evident from data on foreign arrivals for the first eight months of the year. According to provisional estimates of the Ministry of Tourism, January to August 2004 saw approximately 2,093,600 visitors to India, 25.8% more than in the corresponding period of 2003. Growth has been spurred by large increases in airline passenger capacity: international airlines have added more than 4,000 seats a week on international routes to India in the last six months alone. Increases in passenger capacity will play a significant role in fuelling growth in travel & tourism. British Airways has recently been permitted to triple its flights to India, and carriers from Australia are now allowed to offer 4,500 seats a week to India, more than double existing capacity. Moreover, Indian private carriers have recently commenced flights to the SAARC region, and have asked the government to be permitted to fly to East Asian countries. Capacity increases will not only bring in more international arrivals, but will, over a period, reduce airline fares to India, which are currently amongst the highest in the world. Assuming a stable economic and political climate worldwide, the outlook for inbound tourism - both business and leisure - is strongly encouraging. Many international investors, particularly those who have invested heavily into China in the past few years, are now looking at India as the next opportunity. Conde Nast Traveller, in its readers� travel awards for 2004, has placed India at number six among the world�s tourist destinations. Domestic tourism will continue to develop rapidly and, according to HVS, will be the real driving force for this industry over the next decade or so. This segment will be helped by the growing wealth base of India�s population and discounted fare options. A significant new development is the arrival of low-cost carriers, pioneered in India by Air Deccan, with other industry players such as Air India (short-haul, all-economy flights to the Middle East and Southeast Asia) and Indian Airlines readying themselves to enter the low-cost market. According to recent estimates of the WTTC, Indian tourism will grow at 8.8 per cent over the next 10 years, which would place India among the most rapidly growing tourism markets in the world. A longer term, sustained growth of the industry depends on how successfully several issues are addressed - relating to old and poorly facilitated airports, inadequate hotels, poor road and transport infrastructure, high levels of taxation and a bureaucratic visa processing system. As of now, at least, India is clearly taking steps in the right direction. Hotel Supply In the recent past, we have been asked several times about the actual

supply of hotel rooms in India. Taking into account all approved and un-approved

hotels, we estimate this figure to be close to 90,000 rooms. This is an

abysmal figure for a country of India�s size and population. An increase

in business sentiments, leading to higher business-related travel or increase

in foreign tourist arrivals, causes occupancy in markets to go up dramatically.

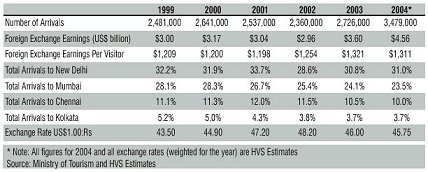

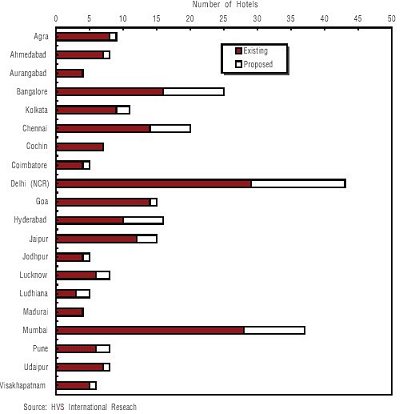

. The Development of Branded Hotels in Major Indian Cities  The year 2003, as we all know, showed an especially strong performance of the tourism industry. While there has been much talk about foreign arrivals, very little has actually been said about domestic tourism, which has grown by about 40% in the last four to five years. Government statistics point to approximately 230 million domestic travellers in 2002 and indicate that this number has risen between 15-20% in 2003. Domestic tourism has, in fact, been the staple diet on which a number of domestic leisure destinations have sustained themselves � the hotel markets of Goa, Jaipur, Agra and various hill stations being among these. With disposable incomes having risen significantly in the last five to seven years, across much of India�s middle income and upper-middle income segments, families have been taking more holidays - and spending more on their vacations - than ever before. The concept of travelling for leisure has, in recent years, gained a more widespread appeal, not only with families, but also young adults, a segment that is earning far more than their parents did at that age. With a certain degree of social change taking place across India, domestic tourism is poised to grow rapidly in the coming years. When will India actually touch the �magic number� of 5 million tourist arrivals? This is a question that those involved in travel & tourism, or the hospitality industry, often ask. This year, for the first time ever, India is going to cross the three million mark. According to our estimates, India would witness nearly 3.5 million foreign tourist arrivals in 2004. The sharp rise in arrivals - as well as the increase in domestic travel - is already showing in the high occupancies of hotels across various cities. Demand for room nights grew at approximately 18% across the country in 2003/04 (according to HVS estimates) and is growing at 15-20% in the current fiscal. Taking into account an estimated demand growth of approximately 18% over the next few years, we estimate that another 65,000-80,000 rooms will need to be added, across the country, in the next five years, to be able to meet the increase in demand. If this does not happen, room rates will rise dramatically, and, consequently, travel will come down, as people will find it too expensive to travel within India unless absolutely necessary. In addition to tourism infrastructure in India being woefully inadequate, the current supply of hotel rooms is much too small to meet the anticipated increases in demand. Our preliminary research indicates that, at best, there are currently only 35,000 - 40,000 rooms under different stages of planning and construction that are expected to enter the market in the next five years. The new supply will also include branded hotels in the budget segment being planned by some major hotel chains across the country. Four years ago, our survey indicated that in the year 2000, 109 hotels were ready to open or were under construction. Last year, this number (hotels expected to open in the next few years) had declined to 63. This year, the number of new hotels under development has once again risen to 97. Moreover, as per our assumptions, an additional 100 economy hotels will also be developed in the economy segment. The maximum development is likely to be witnessed in the National Capital Region (NCR), particularly in Gurgaon. Bangalore and Mumbai are next in line, where at least 9-10 projects are currently under consideration. Hyderabad and Chennai are also likely to witness 5-6 new hotels. We expect the new economy hotels to be developed mostly in secondary and tertiary locations. With regard to the expected increase in supply, it is entirely possible that a number of these projects will face financial difficulties while in progress. The blame for this lies with both the government agencies as well as the new developers. A classic example is that of the numerous developments in Gurgaon. The local government is auctioning land for commercial development (including hotels) at high prices, thus forcing new developers (bid winners) to build hotels that are luxury or upper mid-market in orientation, whereas the need of the hour is budget hotels or dedicated extended stay products. Many of the new developers do not want to be seen building budget hotels, as this does not fit in with the profile of their other businesses. Thus, several such developers are tending to partner with operators who are desperate to enter a particular market and will compromise their standards for location / partner and product just to plant a flag. The recent success of some hotels in Gurgaon - which have done extremely well and beyond most expectations - has been the main motivator for these businessmen. These new owners, it seems, have failed to realize that when 7-9 hotels open at the same time (in the next three to four years), only those projects that have been careful planned and executed will survive the competition or the next phase of economic slowdown in the country. The NCR still remains the favourite destination, in terms of the number of new hotels slated to become operational in the next few years. Seventeen hotels are in various stages of planning and development in the NCR, of which eleven properties are expected to be located in Gurgaon. We understand that, apart from these, there may be a few additional properties under development in West Delhi as well. Survey Results The HVS International survey has been computed by dividing the respondent branded hotels into their respective classifications according to star grading. As before, we have examined the performance of ten major cities across India, wherever a reasonable sample allowed. While most of the responses to the survey were given in Indian Rupees, we have presented some results in US Dollars as well. For the first time in six years, both occupancy and average room rates improved in 2003/04. The performance in US Dollar terms was even better due to the appreciation of the Indian Rupee. |

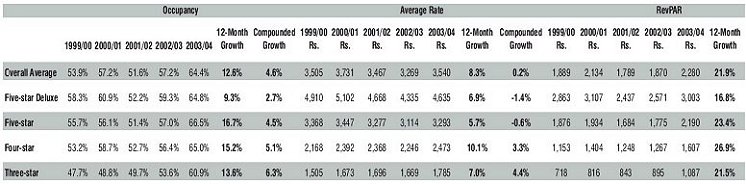

| The number of budget hotels in the branded segment in India has increased

significantly over the past several years, and today represents approximately

35% of the total rooms in our survey. The increased representation of branded

budget hotels has lowered the overall industry figure for average rate.

However, it may be noted that, over a five-year period, the compounded

growth has been the strongest in the budget segment. The RevPAR of the

three-star hotel segment grew at 10.9%, followed by four-star at 8.7%.

The slowest growth was, in fact, witnessed in the five-star deluxe segment,

which grew marginally, at 1.2%.

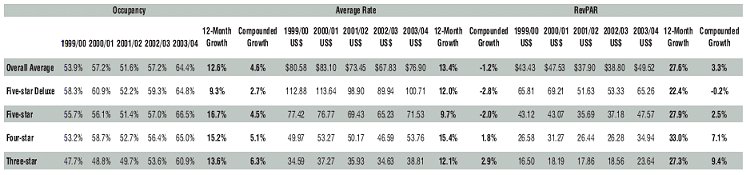

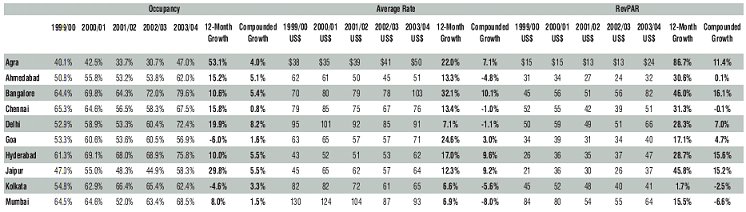

For the second time in a row, there has been an across-the-board improvement in occupancy: average occupancy rose by 12.6% in 2003/04, compared to 10.9% the previous year. Demand for hotel room nights improved across all-star categories in 2003/04, with occupancy close to or higher than double digits, in each segment. The five-star category has witnessed the most growth (16.7%), followed by four-star (15.2%). The increase in occupancy levels this year was even stronger than in the previous year. In terms of average rate, all star categories experienced healthy growth in 2003/04. The four-star segment experienced the most improvement (10.1%), while the five-star segment witnessed the least improvement (5.7%). In US Dollar terms the four-star segment grew at 15.4%, followed by three-star (12.1%) and five-star deluxe (12.0%). Average rate in Rupee terms increased at 8.3% (compared to a 5.7% decline

in 2002/03), resulting in an overall improvement of 21.9% in RevPAR or

a 27.6% RevPAR increase in US Dollar terms. Average rate in US Dollar terms

showed a countrywide increase of, 13.4%.

|

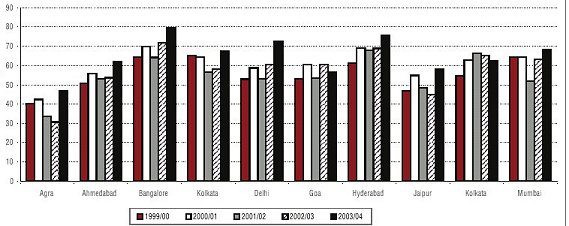

| A new and interesting trend is that Agra and Jaipur have seen substantial

improvement in their performance in terms of occupancy, growing at 53.1%

and 29.8%, respectively. This is followed by Delhi, which is part of the

�Golden Triangle�. Bangalore and Hyderabad - the two IT giants - are clearly

the star performers, recording occupancy of 79.6% and 75.8%, respectively.

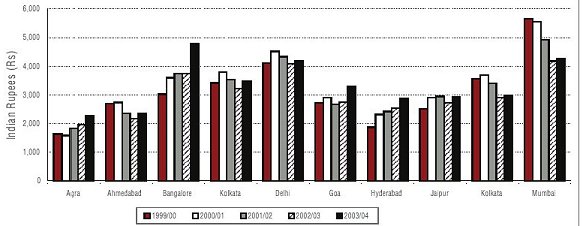

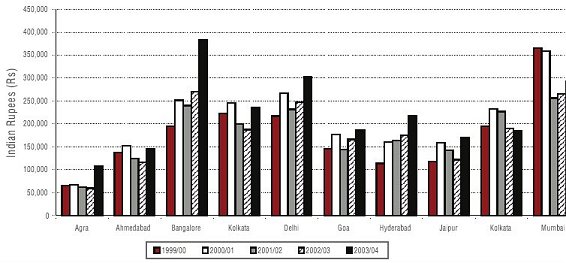

Significantly, Bangalore displaces Mumbai for the first time and has become the market average rate leader with a growth of 28.0%. This is an astonishing achievement for the city which, till four years ago, was ranked fifth (behind the four metros). Goa (19.6%) and Agra (17.0%) were the two cities that showed good improvement in average rate. Hyderabad, which has generally been a very price sensitive market, also grew at 12.8%. Three large metros had modest increases in average rate, and that too for the first time in three years: these were Delhi (2.3%), Mumbai (2.2%) and Kolkata (2.0%). In 2003/04, only two cities exhibited a small decline in occupancy: these are Goa (6.3%) and Kolkata (4.6%). The decline may attributed to new supply entering these cities. Delhi grew at 19.9% and Chennai at 15.8%, followed by Ahmedabad (15.2%), Bangalore (10.6%), Hyderabad (10.0%) and Mumbai (8.0%). In terms of RevPAR in 2003/04, Bangalore was in number one position, followed by Delhi, Mumbai and Chennai, with Mumbai having been relegated to third place for the first time. However, the biggest improvement during 2003/04 in terms of RevPAR was seen in Agra (79.1%), followed by Bangalore (41.5%) and Jaipur (39.1%). The only decline in RevPAR was seen in Kolkata (2.7%). All cities, with the exception of Mumbai and Kolkata, have experienced positive improvement in terms of compounded growth of RevPAR. Over a five-year compounded period, the two main centres of IT activity - Bangalore (18.3%) and Hyderabad (17.4%) - have grown the most. Negative growth was witnessed in Mumbai (�5.4%) and Kolkata (�1.2%) over the same period. This is much to do with a situation of oversupply in these markets. The year 2003/04 saw significant supply additions to several cities, with the maximum growth witnessed in Goa, Mumbai and Kolkata. A huge surge in demand in Goa and North Mumbai has helped in absorbing this new supply. Goa may have experienced decline in occupancy, but its overall performance, in light of the supply increase, is commendable. With very little new supply expected in Bangalore, Hyderabad and Goa over the next two years, we expect these markets to improve significantly. In addition, in the medium term, even Delhi, Mumbai and Chennai are likely to improve. Average rates in cities like Bangalore and Hyderabad are likely to be substantially higher, with Bangalore registering among the strongest growth worldwide. In the leisure segment, we expect Jaipur to see a slowdown, however, Goa remains a very strong prospect. |

| Future Trends

HVS has been conducting this survey for seven years, and, for, the first

time, it appears that Indian hotel industry has completed a full cycle,

experiencing both downswing and upswing periods. The industry is robust

at present, and there are clear indications are that the next two to three

years will be even stronger. Certain markets are already seeing huge un-accommodated

demand during weekdays, with average rates in some of these markets witnessing

unprecedented increases. All the ten cities we studied have seen a positive

trend in both occupancy and average rate.

|

| .

While all cities have seen increases in rooms occupied per day (over the previous year�s corresponding period), Goa (28.7%) is the market leader, this is what has allowed this leisure destination to absorb the new supply increase of 23.8%. Mumbai (18.1%) has the second highest growth. In fact, of the seven cities studied by us, Hyderabad was the only city to have a single-digit growth (9.4%). Chennai (17.9%) Bangalore (15.9%), New Delhi (12.9%) were the other strong performers in the market. In terms of average rate, Bangalore (58.4%), Hyderabad (21.2%), New Delhi (9.7%) and Chennai (9.2%) have all had increases. In fact Kolkata is the only market which saw average rates decline marginally. Year-to-date occupancy for Bangalore at 80% means that there is not much potential for further increase in occupancy, as weekdays are mostly sold out. Strongly escalating demand has caused hotels to push rates way beyond what they should be getting for the quality of product they offer. This is certainly true of some of the properties that never had a proper refurbishment and are now charging exorbitant rates. We would expect operators to raise average rates strongly in Hyderabad as well. Recent indications are that the hotels in south Mumbai have also started to see improvements in performance. This effectively means that Mumbai is poised to see good growth in terms of both occupancy and room rate increases as demand outpaces supply. Goa and Delhi are also expected to see some rate increases. Traditionally, average rates rise in October, therefore, our data is not reflective of rate increases that are likely to take place shortly. Many of these rates are negotiated rates with corporates and travel agents which will come into effect as the peak season kicks in. The most encouraging development during the first five months of the current year has been the healthy increase in RevPAR across all cities. Bangalore (61.2%), followed by Hyderabad (32.6%), have, for the second time in a row, witnessed the highest growth in terms of RevPAR. Chennai (27.4%), Goa (23.0%) and New Delhi (12.2%) have seen double-digit growths. Mumbai (9.9%) and Kolkata (9.5%) also witnessed single digit growth. The Goa market has performed exceptionally well and in the years to come will be one of the best performing markets. The city over the past two years has seen substantial increases in rooms supply, despite this demand continues to outstrip supply, resulting in occupancies to go up marginally even in the current year. At present there is not much new hotel activity planned for Goa, making this one of the preferred location for investment. Another market performing extremely well (but is not part of this survey) is the Pune market. The sharp upturn in Bangalore�s performance is beyond what most hotel owners and developers had anticipated. Despite HVS having forecast the city�s hotel market to do a sharp turnaround we, too, are taken by surprise by the extent of improvement. Existing hotel owners can expect a windfall gain this year as well as for the next few years, until new supply enters the market. The Leela Bangalore is amongst the biggest beneficiaries; this hotel is already setting records for highest average rates in the country for a business hotel (US$275 - US$300). We understand that at least 9 hotels are planning to enter Bangalore. As a result, we can expect the market to slow down in two to three years with rates declining sharply. The trends witnessed in Delhi in 2004 have been quite positive, reinforcing our faith in the city. Occupancies have picked up over the past few months, especially in hotels closer to Gurgaon. These hotels enjoy much healthier occupancies than city centre hotels which, in fact, are pulling down overall occupancy levels. Year-to-date average rate growth is only 3.2%, but is anticipated to increase further during the peak season. Also, with the proposed conversion of Kanishka to Shangri la and Ashok Yatri Nivas� re-development, we can expect further competition within Delhi�s central business areas. The new Trident Hilton (in Gurgaon) has been an extremely good performer and is currently market leader in terms of RevPAR. Opportunities Opportunities for the Indian hotel sector continue to be in the budget and mid-market segment: we anticipate these segments to witness huge growth and expansion, in the next year or two. The luxury segment is set to perform extremely well over the next few years until the supply- demand gap is bridged. We expect average rates to grow in all major cities across India. New opportunities lie in the extended stay segment, which many potential developers are currently shying away from. Also, HVS has observed that owners interested in developing extended stay properties are keen to partner with existing branded chains already operating in India. This, according to us, is an area where specialized serviced apartment chains like Oakwood and Ascot have tremendous scope for involvement. This is particularly true in destinations that are near large concentrations of IT and related services development. Medical tourism could also be the next big thing, and, while we are yet to see any development in this area, we consider that there could be some potential. If world class convention centres are indeed developed in Mumbai, Delhi and Goa (as proposed, with government support), these cities are sure to benefit. Similarly the further liberalization of the aviation sector would mean additional tourists, and with supply unable to keep pace with demand, nearly all segments of the hotel industry would see improvement. HVS is of the view that if you are not already building a hotel in India, then you are late. The present period of upswing however, we believe, will last longer than the previous period of upturn (1995-97). There are clear indications that travel & tourism in India will grow faster now than ever before this bodes well for the hotel industry. In last year�s edition of this report, we mentioned that Agra and Jaipur were the weak links in the industry. Thanks to increase in both inbound and domestic tourism, the two cities have experienced the strongest recovery over the 12-month period. We expect this trend to persist into the current year as tourist arrivals continue to go up. Agra, while having seen highest improvement, has still a long way to go (citywide occupancy 47%). There also some unfinished hotel projects in Agra, which will continue to put pressure on the city�s performance. As regards Jaipur, the recent announcement by a major IT company to set up a base outside Jaipur, as well as the state government�s initiative to promote IT-related activity in the city, means that Jaipur can look forward to some additional room night demand from the business segment. These developments in the leisure segment including the strong performance in Goa leads us to believe that the leisure segment is clearly benefiting from the increase in foreign tourist arrivals and growth in domestic travel. We also consider that in the future years new leisure destinations in Kerela and other coastal areas will also pick up. Recent announcements by the Government of India to promote tourism in the Andaman and Nicobar Islands could not therefore have come at a better time. Hotels in metro cities, with an average rate of Rs 2,600-3,000, and hotels in non-metro cities, with an average rate of Rs 1,800-2,400, are likely to experience rapid growth in demand in the next year or two. Cities to watch out for, in terms of development opportunity, are Pune, Goa, and certain pockets in major cities like Delhi (west) and Mumbai (mill lands). We would however, like to caution investors to stay away from the current �hotspots� of Hyderabad, Bangalore and Gurgaon, as large additions to supply have been planned here. The real opportunity, we believe, is in a good mid-market or budget hotel of international standards. Acknowledgements The Hotels in India� Trends and Opportunities has been developed for the benefit of employees, developers, investors and operators with an interest in the tourism industry in India. The study has been made possible only with the contribution and support of all the domestic and international hotel chains, to who HVS International would like to express its gratitude and appreciation. If you or any of your colleagues would like to receive complimentary copies of the HVS International -Trends & Opportunities report, or HVS Executive Search information, kindly send your e-mail address along with full contact details to Chandrima Budakoti at [email protected] . Alternatively, please visit our website www.hvsinternational.com and register yourself. About the Authors Manav Thadani joined HVS International's New York office as a Consultant and Valuation Analyst in September 1995. Prior to joining HVS, he gained six years of operational experience in various hotels in New York City. In early 1997, Manav planned the opening of HVS International's first Asian office in India, which was established in New Delhi later in the year. Manav holds a Masters degree in Food Service Management from New York University (NYU), prior to which he completed his undergraduate education in hotel management at NYU. Email: [email protected] Deepika Malkani is Editor with HVS International's New Delhi office and is also involved in research. Her previous experience includes working as writer and research analyst with the Economist Intelligence Unit (EIU), New Delhi. She has also been writing for the monthly publication Indian Infrastructure, on infrastructure development and related project financing, for the last five years. Deepika has a Bachelor's degree in Economics from Delhi University and an MA in International Economics and Finance from Brandeis University, USA. About HVS HVS International has been operating in India for seven years. The HVS team has worked on projects ranging from feasibility and marketing studies; valuation of hotels; residual land values; management contract values; operator search & management contract negotiations; development strategies for new brands; impact analysis; research reports, investment services and ECOTEL ® Certification. |

.

| Contact:

HVS International

HVS International New Delhi

|