|

|

|

|

|

|

|

Governments in the Region are Making Tourism a Priority |

Paris, 27 August 2004

|

Results of the corporate

chain hotel industry in the Middle East

in July 2004, and

total over 12 months

|

|

|

|

|

|

|

|

| 07/04 vs. 07/03 |

|

|

|

|

|

|

| Total 12 months |

|

|

|

|

|

|

total over 12 months

|

|

|

|

|

|

|

|

| United Arab Emirates |

|

|

|

|

|

|

| Egypt |

|

|

|

|

|

|

| Saudi Arabia |

|

|

|

|

|

|

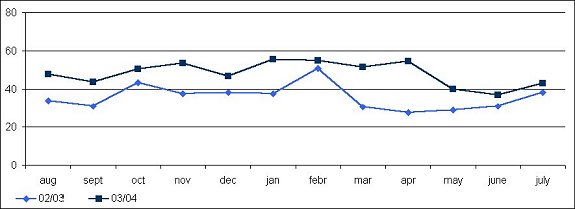

| In the Middle East (zone including, in the results

published by MKG Consulting, the countries in the Arabian Peninsula, Egypt,

Lebanon, Jordan, and Syria), RevPAR (total over 12 months at the end of

July) leaped by 36%, notably thanks to a significant growth in the occupancy

rate of nearly 12 points. Over the entire year, the average occupancy of

hotels in the zone reached nearly 70%. This rise in occupancy rates was

accompanied by a significant rise in the average room rates by more than

13%.

The majority of countries in the zone are running at full steam. The United Arab Emirates, notably thanks to the dynamism of Dubai, recorded a rise in revenue per available room quite near to that of the zone as a whole. Egypt saw an even greater rise (+12 points in occupancy, and +25% in the average room rate for a rise in RevPAR of nearly 50%). The country is a particularly attractive destination. The constant devaluation of the Egyptian pound since 2001 strengthens the attractiveness of this country with regards to international customers. Saudi Arabia, without a doubt the best perceived in terms of security, is seeing its hotel results remain on a growing trend, despite the progressive pullout of American soldiers. Religious tourism is developing, while the authorities have extended the pilgrimage periods towards the holy cities of Mecca and Medina. These positive changes follow a delicate period, after the September 11th attacks, and the opening of the war in Iraq, events that combine to inflate the rate of change this year, notably in March and April. They nevertheless also result from a real dynamism in the hotel industry, which is visibly in the July results. The overall average room rates in the Middle East zone are rather stable throughout the years, though the improvement at the level of occupancy assures monthly RevPAR growth of over 12%. The main explanation for this increase is the rise in inter-regional traffic. Arabs in the Gulf give preference to local destinations rather than trips to the United States and Europe. The additional regional customers are beneficial to the leisure segment, notably in the United Arab Emirates with Dubai, in Egypt with the banks of the Red Sea, the destinations in Upper Egypt, Cairo, and in Lebanon. It also profits from business tourism, due to the numerous infrastructure projects in cities such as Kuwait City, Dubai, Cairo and Abu Dhabi. A second pillar of support in hotel activity in the Middle East resides, paradoxically, in the war in Iraq: after having undergone a slowdown in activity during the beginning of the conflict, the countries of the Gulf today benefit from the presence of the American military and the support of businesses that are playing a role in the reconstruction of Iraq. Up till now, Egypt and Dubai have remained, in the region, the major destinations for leisure customers from the West. Though Oman, Qatar and Bahrain are certainly putting into place a policy of easing visa restrictions and increasing promotions, they have not yet been able to match Dubai's level of activity. Medium-term perspectives are very favourable. Governments in the region are making tourism a priority. For countries that do not have the oil resources found in the Gulf, tourism development may be a significant source of revenue. This is notably the case with Egypt and Lebanon. For the Gulf countries, the development of economic sectors that would allow compensating for a drop in wealth stemming from the oil industry is also beginning to be considered. However, for the moment, the rise in the price of oil should give even greater means to local investors to carry out their massive projects, such as the Palm Islands of Dubai, or the Dolphin oil pipeline, launched by Qatar, which crosses the Arabian peninsula. For the Middle East as a whole, this spirit of competition between the various countries should make the region into one of the most dynamic in the world on the tourism level. |

Revenue per available room

in the corporate chain

hotel industry in the Middle

East

Source: MKG Database - Official

statistics of chain hotels - August 2004

Average room rates and RevPAR

expressed in euros inclusive of tax

| Methodology

The MKG Consulting Database contains a sample of 10,000 corporate chain hotels, representing 1,000,000 rooms throughout the world. MKG Consulting has the largest hotel database in the world, outside the USA, with a good representation of all hotel segments. |

Contact:

Georges Panayotis +33 (0)1 56 56 87 90 [email protected] http://www.mkgconseil.com |