|

|

|

|

|

|

|

|

|

Issues Report Analyzing Strategic Hotel Capital's Pending IPO |

April 12, 2004 Is Strategic Hotel Capital a Strategic Investment for You? Strategic Hotel Capital Inc. has filed a securities registration with

the Securities and Exchange Commission. The company will segregate the

assets historically owned by Strategic Hotel Capital LLC (referred to below

as �Historical SHC�) into two pools: one a publicly-traded Real Estate

Investment Trust (the �Public REIT�); and the other a

Introduction Strategic Hotel Capital�s offering is being underwritten by one of its major owners, Goldman Sachs & Co. In light of the potential for conflicts of interest in the underwriting, the structure of the offering, and the management of SHC�s two portfolios (one public and the other private), we have taken a critical look at why the company has withheld several significant assets from this long-awaited IPO, and pose the following question: What benefits does this reorganization bring to the company�s current ownership, and what risks does it pose to potential new investors? Goldman Sachs, through its Whitehall Real Estate Funds, has been a major owner of Historical SHC since the company�s inception in 1997, and will remain an owner in both the newly-formed Public REIT, and in the Private LLC whose assets are withheld from the current offering. Goldman Sachs has also been a major source of debt financing for Historical SHC. Given the critical role an underwriter plays in setting the price of newly issued shares and in overseeing disclosures provided to public investors, we believe investors are not getting an independent evaluation of the company and its restructuring as they consider buying into this IPO. Moreover, the Public REIT has agreed to indemnify Goldman Sachs against offering-related risks, despite the fact that the Public REIT � and therefore public investors � may be disadvantaged by the insider role Goldman plays in the company and in the offering. One of the more intriguing aspects of this IPO is the division of Historical SHC�s hotel assets into two separate pools: those owned by the Public REIT and those retained by the Private SHC. The hotels included in this offering have historically performed better than those withheld in the private pool, and will therefore command a higher offering price from new investors. The poorer performing asset pool � which possibly holds greater �upside� potential � will be retained by the private owners, but it will be asset managed by the Public REIT for a $5 million annual fee. Within this structural division lie some fundamental questions for prospective investors:

We also question whether prospective shareholders should buy the best

part of Historical SHC�s portfolio now, as lodging stock prices approach

historical highs, without gaining the benefit of improved operating results

at the privately-held properties their company will continue to manage.

These assets currently show poorer operating results than the ones Strategic

Hotel Capital has offered to investors in this IPO, but have considerable

�upside� potential. If public investors are to provide the asset management

that potentially repositions these assets for sale at a future date,

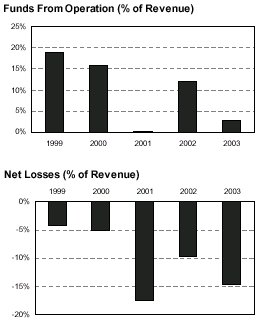

If prospective investors conclude that they would obtain a better price for the entire Historical SHC portfolio, then we believe that the potential conflicts of interest among the ownership and management of the proposed Public REIT and the Private LLC may have financial consequences for these investors. Accordingly, we argue below that investors should consider demanding either: 1) that SHC include its entire portfolio in the IPO; or 2) that the newly-formed Public REIT have no asset management relationship with SHC�s remaining private assets. While changes such as these might not address all potential conflicts in this offering, we believe they would create a better value for investors who buy in now. Underwriters� Interests Goldman, Sachs & Co. has many potentially conflicting roles in SHC�s stock offering. Acting as a major shareholder in the Private LLC, as a major shareholder in the Public REIT, and as underwriter, the investment bank stands to gain from several possible aspects of the IPO. We question whether prospective investors are disadvantaged by Goldman�s competing roles in this offering, and whether the Public REIT should indemnify Goldman against offering-related risks. Two of Historical SHC�s principal shareholders, Whitehall Funds VII and IX, are controlled by Goldman Sachs related companies, and senior managers with Goldman have held several board seats at Historical SHC. Whitehall will remain a major stakeholder in the Private LLC, as well as in the Public REIT. Goldman Sachs has also played a major role in organizing debt financing for Historical SHC, and could continue to play such a role in future. But perhaps the most important of Goldman�s potential conflicts lies in its dual role as existing owner and as underwriter of this offering. As underwriter, Goldman Sachs is partially responsible for setting the initial share price paid by investors and for disclosing material information about the company for investors to consider evaluating that share price. The investment community should in this context scrutinize the following aspects of this IPO: Pricing shares: Goldman Sachs, as underwriter, will play a central role in determining the initial pricing of the Public REIT�s shares. Since Goldman is also a major equity holder, the pricing of these shares will have a direct financial impact on Goldman Sachs�s investment in Strategic. By virtue of its ownership, Goldman is not an independent party in the negotiation of share price between seller and buyer. Prospective investors may want to examine whether their interests would be better served if the final price of the REIT�s shares were established by a strictly independent party. Indemnified from responsibility: Goldman Sachs is also responsible for overseeing disclosures related to this filing � disclosures by a company in which it has an ownership interest. Yet the Public REIT has agreed to indemnify Goldman Sachs against liabilities under the Securities Act of 1933. i Investors should question why public shareholders ought to indemnify an underwriter who is also an owner in the company, and who, by virtue of that ownership position, is privy to inside information. As can be seen in recent regulatory actions, conflicting roles in investment banking can pose financial liability. Public investors may be inadequately protected when the underwriter who represents the condition of this company also has a financial stake in the outcome of this offering, in the form of an equity stake that is much larger than offering-related fees. With potential conflicts of interest throughout this offering, the indemnification agreement may well represent a significant financial risk to investors in the public offering. We also point out that Goldman Sachs� Whitehall Funds and certain other existing investors maintain the right to request that the Public REIT register an offering of their shares on two occasions within the first year following the IPO. The Public REIT is also required to maintain a shelf offering for resale of those investors� shares following the first anniversary of the IPO. During the first year, the Public REIT will have the option to repurchase shares of owners requesting registration, at fair market value as determined by the Board. These rights give existing shareholders, including Goldman�s Whitehall Funds, an option to exit some portion of their investment in the company in the months following the IPO. The Public REIT may be in a position to have to choose whether to allow additional shares to trade in the market, potentially affecting the market price, or to use funds from the IPO to buy out Goldman�s Whitehall and other original shareholders within the first year after the offering. The REIT�s Board of Directors will be the nexus for these potential conflicts of interest going forward, suggesting that prospective investors may want to evaluate how truly independent the Board will be. Management Interests Strategic Hotel Capital has proposed that the Public REIT continue to asset manage the properties held by the Private LLC, for an annual fee. However, the Private LLC assets have performed worse as a pool than the assets of the Public REIT, and could therefore require a disproportionate level of attention on the part of management to reposition. This problem may be exacerbated by the fact that management could be incentivized to focus their efforts on the Private LLC�s properties, possibly at the expense of the assets owned by the Public REIT. Moreover, because this asset management fee will not grow proportionately as operating results improve, we believe investors should discount this fee when evaluating the REIT�s share price as a multiple of FFO. Alternatively, we believe that public investors would benefit substantially if Strategic Hotel Capital were to maintain a rigid separation between the Public REIT and any assets withheld from this IPO. The seven properties withheld from this IPO (making up more than 40% of Historical SHC�s room count) have, as a group, performed worse than the portfolio offered to investors. As such, they may require more managerial focus than the better performing properties in the Public REIT. According to the company�s Pro Forma Consolidated Statements of Operations for 2003, the properties included in the Public REIT generated an $8 million net loss, or 2% of those properties� revenues. By contrast, the properties that will remain in the Private LLC generated a $59 million net loss, or 25% of those properties� revenues. While it is the owners of the privately-held hotels who stand to benefit as those properties improve during this recovery, it will be the public company�s management which will work to create that new value even as it manages the Public REIT�s assets. Public investors will miss out on that �upside� under the proposed structure. As major voting shareholders in the Public REIT, Goldman Sachs�s Whitehall Funds and Prudential Financial will both influence the REIT�s Board of Directors ii (the registration statement states that they also will have the right to observe the Public REIT�s Board meetings iii ). Yet both these entities will remain the largest owners of the Private LLC iv . As a result, management will report to a Board elected in part by entities with an interest in the financial performance of the Private LLC. Moreover, the Public REIT�s Chairman and CEO has held an ownership interest in Historical SHC v , and he and other managers have had an option to exercise unit appreciation rights in that entity vi . The Public REIT has not disclosed either the equity ownership by management and related parties, or the governance structure of this Private LLC in its registration statement. Since public investors, through the Public REIT, will bear corporate expenses for managing the seven withheld assets, prospective investors should question whether the REIT�s asset management of those seven properties creates a conflict of interest that undermines their investment. Given the fact that the REIT�s management will oversee both pools of hotels, there is also a possibility that the Private LLC could propose to sell one or more of its hotels to the Public REIT at a time when the private investors have realized some of the �upside� potential. Again, it will be the REIT�s Board of Directors (elected in part by owners of the Private LLC) who will be in a position of arbitrating these potential conflicts of interest. Even at a fair market value, the potential purchase of these private assets sometime after this IPO takes the valuation process out of the hands of prospective investors (who will not have the opportunity to factor those assets into their purchase price) and puts it into the hands of a Board and management with possible conflicts of interest. The company does acknowledge that, because Whitehall and Prudential are the largest beneficial owners of the Private LLC, the Public REIT �may experience conflicts of interest in connection with� our acquisition of hotels from SHC LLC� vii . Additionally, even though $5 million per year may represent a reasonable asset management fee for these assets in an arms� length transaction, we believe investors should closely scrutinize this related-party fee from two perspectives. First, prospective investors should note that the $5 million annual fee only offsets a portion of the corporate expenses that accrue to the 7 privately owned hotels, while the Public REIT funds all of the corporate expenses for the public and private hotels. The properties allocated to the Private LLC generated $240m revenues in 2003, or 42% of the combined $566m revenues from the Private LLC and the Public REIT viii . This $5 million annual asset management fee would therefore account for just 23% of Historical SHC�s corporate expenses for 2003. Second, the Public REIT has computed the REIT�s pro forma FFO to include revenues from this asset management fee. If investors are considering paying similar multiples of FFO for this offering as investors are paying for other public hotel REITs (see next section), we urge them to carefully assess the future value of this revenue stream. As we discuss below, share prices are trading at high multiples of FFO in anticipation of a recovery in operating results (which would cause FFO to improve more rapidly). As the REIT�s filing states, this asset management fee �will decline as SHC LLC [the Private LLC] sells its hotel properties� (p. 16). This revenue stream may not have the same future growth potential as the Public REIT�s hotel-generated FFO. While Public REIT describes its intention to secure asset management contracts for unrelated hotel owners in the future, no such contracts currently exist. By eliminating this asset management relationship with Private SHC, investors in this offering would remove one significant potential conflict of interest, would secure the benefit of 100% of their management�s talents and focus, and could limit corporate expenses to those reasonable for the Public REIT�s assets. Although somewhat counterintuitive, investors may do better if they were to assess the offering on the basis of a lower FFO, but one that would be more responsive to the economic recovery. A Better Deal for Shareholders? Now approaching historical highs, share prices are currently anticipating

a recovery in the lodging industry, even while operating results remain

relatively poor. The Strategic Hotel Capital offering takes advantage of

this asynchrony, which benefits the company�s present ownership. Potential

shareholders might obtain a better investment were they to purchase Historical

SHC�s entire portfolio, rather than the partial portfolio presented in

this IPO.

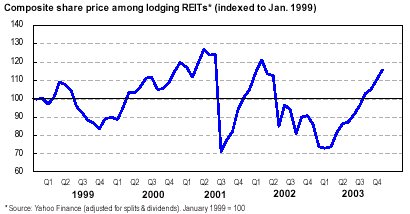

Source:Yahoo Finance (adjusted for splits ÷nds). January 1999 = 100 Even as operating results are expected to remain at below-peak levels well beyond 2004, investors have boosted the share prices of hospitality REITs in anticipation of an operating recovery. The average composite share price of seven major publicly-traded lodging REITs ix is presently trading 60% over its recent lows in early 2003, and 9% below its peak in early 2001 (see chart). In effect, current share prices have already �priced in� dramatically improved operating results. This is in line with Bear, Stearns� analysis that even in the 3 rd Quarter of 2003, the bull market in lodging shares had already anticipated 18 months� worth of �robust recovery�x . As a result, ratios of current share prices to forward FFO are reaching

historical highs, as anticipatory demand for lodging shares outpaces the

industry�s recovery. Smith Barney Global estimates that current share prices

among lodging REITs are running an average of more than 17 times their

expected 2004 FFO-per-share estimates, and more than 12 times their 2005

FFO estimates. This is far above the sector�s mid-cycle norm of 9 times

xi

. Analysts such as the National Association of Real Estate Investment Trusts

(NAREIT) and Smith Barney Global estimate that price-to-FFO ratios among

lodging REITs will fall by an average of 16% or more in the coming year

xii . Hence, if the amount of the asset management fee from the Private

LLC may decline, as the company discloses, and the multiple of FFO that

shareholders are willing to pay is anticipated to decline in the coming

year, the future value of the asset management fee may be proportionately

less than that of the company�s FFO from its owned hotels.

Historical SHC has performed poorly since its inception in 1997, even during the lodging industry boom of the late 1990s. To date, the company as a whole has not yet generated a net profit, and even at the height of the market in 2000, produced a net loss of 4% of revenues. FFO has also declined during this period � and while this would be expected under the difficult economic conditions of the past three years, they also declined in 1999 and 2000, a period during which most of the industry experienced higher RevPAR. As discussed above, Strategic Hotel Capital is taking public an asset pool that has performed somewhat better than this historical company-wide record. The properties in this pool posted a net loss representing 2% of revenues during the first nine months of 2003 � compared to a net loss equivalent to 25% of revenues among the properties proposed for the Private LLC. Measured as a percent of revenue, FFO in the Public REIT�s pro forma is more than twice the FFO of Historical SHC�s entire portfolio. We postulate that these better performing assets may generate a higher initial share price from future investors than would the full Historical SHC portfolio. The proposed restructuring of Historical SHC into the Public REIT and the Private LLC may potentially result in substantial �upside� value being retained for Private SHC�s owners. For example, one of the Private LLC�s major markets, Northern California, is expected to be among the most- improved operating environments during 2004 xiii . Moreover, we believe that investors may actually stand to benefit significantly more from an offering that includes Historical SHC�s entire asset pool, including the poorer performing hotels that have been left in the private LLC. If all the assets are brought into the public offering, investors would apply a multiple to forward FFO based on a larger cash flow, but that FFO might be likely to grow at a faster rate, as the currently less profitable properties are successfully repositioned. Summary Analysts expect the lodging market to see a number of public offerings emerge over the coming months xiv . As a result, investors in the lodging industry can be selective about the companies in which they choose to place their capital. We believe that Strategic Hotel Capital�s current offering poses a number of risks to investors, and that prospective investors have an opportunity at the present time to create a better deal for themselves by encouraging SHC to restructure this offering. What might have been a simple public offering of Historical SHC�s entire portfolio has instead presented an array of potential conflicts of interest, and structural complications that may disadvantage prospective investors. In response, investors might consider demanding: 1. That Strategic Hotel Capital retain for this offering an underwriter with no pre-established financial relationship with this company. This would provide greater confidence that prospective investors� interests will be adequately protected, especially with respect to documents issued in connection with this offering. 2. That Strategic Hotel Capital offer its entire portfolio in the planned IPO. Investors might thereby not only obtain a better share price for the Public REIT�s assets, but also might derive the benefit of any turn-around in the operating results of the Private LLC�s assets. 3. That Strategic Hotel Capital abandon plans for its Public REIT to asset manage properties withheld from this offering. Strict separation of the Public REIT from any properties Private SHC withholds would eliminate at least one potential conflict of interest among managers employed by public investors, and could also produce a better share price for prospective investors. This analysis urges prospective shareholders to consider either 1) eliminating the asset management relationship to the privately held SHC (to reduce the potential conflicts and lower the share price paid by investors), or 2) seeking a restructuring of the offering so they have the opportunity to buy the entire company at current multiples (thereby securing for public stockholders any upside value in the lagging properties). With an offering as fraught with potential conflicts as this one, we also urge investors at a minimum to require unusually stringent corporate governance policies to guard against the potential financial implications of this corporate structure. As private companies such as Strategic Hotel Capital submit offerings

to meet growing demand in the lodging market, investors will have a wide

range of choices for investing in this industry. Because share prices already

reflect anticipated improvement in operating results, however, investors

should exercise particular caution in evaluating new offerings. This particular

offering raises a number of questions about the structure of IPOs in the

lodging industry, especially with respect to potential conflicts of interest.

In light of these questions, we urge the public to evaluate Strategic Hotel

Capital carefully before subscribing to this or other offerings.

Hotel Employees & Restaurant Employees Union, Local 2 |

| Contact:

Ian Lewis Research Analyst Hotel Employees & Restaurant Employees Union, Local 2 (HERE) Local 2 209 Golden Gate Avenue San Francisco, CA 94102 tel: 415-864-8770 ext. 760 email: [email protected] |