|

|

|

|

| by: David J. Sangree, MAI, CPA, ISHC

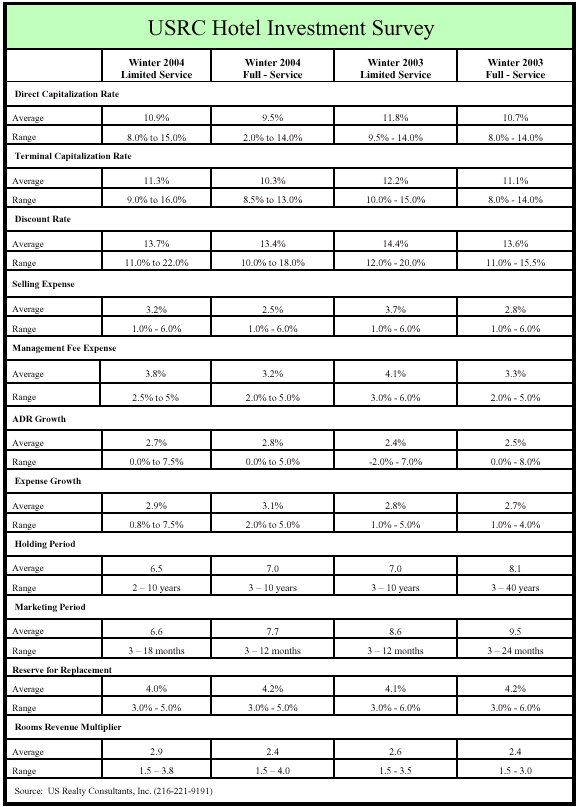

February 2004 The Winter 2004 USRC Hotel Investment Survey of hotel investors indicates that discount rates and capitalization rates for both limited service and full service hotels have decreased since our Winter 2003 survey. The author has completed this hotel investment survey annually since 1995. The drop in both types of rates is due to increased confidence in the overall hotel market, as most markets are projected to achieve increases in occupancy and ADR in 2004, which will increase overall revenue and net operating incomes. In addition, new hotel development maintained its slow pace during 2003, while interest rates remained low. Full-service hotels recorded a larger decrease in direct capitalization rates as compared to limited service hotels. The decreases have occurred as the risk associated with hotel investments has returned closer to normal levels following the impact from the recession and pending war with Iraq on last year�s survey. The lower rates also reflect the poor performance of many hotels in 2003 which investors have purchased at lower capitalization rates. Capitalization Rates Our 2004 survey indicates that investors continue the trend of requiring higher capitalization rates for limited-service hotels as compared to full-service hotels. The direct capitalization rate for full-service hotels of 9.5% is 120 basis points lower than the average for 2003, and 210 basis points lower than the 2002 survey average. The average direct capitalization rate for limited service hotels of 10.9% is 90 basis points lower than the average for 2003, and 130 basis points lower than the 2002 survey average. |

| The range of capitalization rates for each category was wide and depended

upon the quality of product and its location. Upper-end, luxury, full-service

hotels in locations with strong barriers to entry had capitalization rates

of 5% to 9%. Terminal capitalization rates for both categories were slightly

higher than the direct capitalization rates as these are utilized five

to ten years in the future.

Discount Rates Higher for Limited Service Hotels Discount rates for limited-service hotels averaged 13.7% and for full-service hotels averaged 13.4%. Discount rates for full-service hotels showed a 20 basis point decrease from the average for 2003 and a 120 basis point decrease from our 2002 survey average. The decrease indicates increased confidence in the hotel market and reflects the lower interest rates and slow pace of new development. The range is wide for discount rates with respondents indicating from 10% to 22%. The average holding period for users utilizing a discounted cash flow analysis for both limited service and full-service hotels ranged from 6.5 years to 7.0 years. ADR Growth Limited The investors surveyed indicated that they project ADR growth rates to be similar to operating expense growth rates for limited service hotels and lower than operating expense growth rates for full service hotels. All investors project ADR growth rates to be positive in 2004. The overall averages were 2.7% and 2.8% for limited service and full service hotels respectively. The ADR and expense growth rates for full service properties were slightly higher than last year�s survey. Management Fee Expense Range Management fee expenses averaged 3.8% of total hotel revenues for limited-service

hotels and 3.2% for full-service hotels. Management fees are typically

higher on a percentage basis for limited service hotels due to the disparity

in total revenues versus full-service hotels. The selling expense ranged

from 1% to 6% for both categories of

Marketing Period Decreasing as Economy Improves The marketing period was 7.7 months for full-service hotels and 6.6 months for limited-service hotels down from 9.5 months for full service and 8.6 months for limited service hotels as indicated in our 2003 survey. The investors indicated that the marketing periods have decreased since last year�s survey which is reflected by the increase in the number of sale transactions in 2003 and 2004 to date. The reserve for replacement as a percentage of total revenue for limited service hotels was 4.0% while for full-service hotels was 4.2%. The higher rate for full-service hotels is due to the larger size of the structures and increased amount of amenities as compared to limited service properties. The room revenue multiplier was typically used by limited-service hotel buyers and averaged 2.9 with a range of 1.5 to 3.8 times room revenue. Only a few of the investors utilized a room revenue multiplier for full-service hotels, which averaged 2.4 with a range of 1.5 to 4.0. Hotel Interest Rates

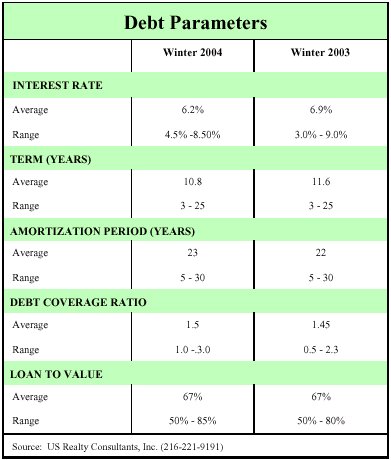

The average interest rate of 6.2% for the Winter 2004 survey decreased from 6.9% as illustrated in Winter 2003 survey. The average rate declined 70 basis points from last year�s survey. The decline is due to the slight decline in the LIBOR rate from 1.477% on January 1, 2003 to 1.461% on January 1, 2004, and increased competition from lending institutions for hotel loans. The average term was 10.8 years which is 0.8 years lower than our 2003 survey. The years amortized was 23 years with the range from 5-30 years which was similar to the previous year�s range. The debt coverage ratio averaged 1.5 with a range from 1.0 to 3.0. The loan-to-value ratio was 67% with a range from 50% to 85%. Investors indicate that financing is still difficult for most new development projects around the nation. Major Concerns The possibility of additional terrorist attacks on US soil, interest rate increases, and higher oil prices are the major concerns of the investors in the survey. The end of the economic recession is projected to help most hotels record increases in RevPAR, which in turn should increase net operating incomes. Increases in NOI are expected to translate into increases in value for most hotels, as investors typically look most closely at the trailing 12 months of performance. Higher oil prices were a concern mentioned by some investors as gasoline prices are expected to reach record highs during the summer 2004 travel season, which may negatively impact hotels in �drive-to� markets as well as result in higher utility and energy costs at hotels. Increasing the supply of hotel rooms too aggressively is a concern also mentioned by some survey respondents. Respondents to the survey include:

David J. Sangree, MAI, CPA, ISHC is President of Hotel & Leisure Advisors, a national hospitality consulting firm specializing in appraisals, feasibility studies, and impact analysis for hotels, resorts, waterparks, and other leisure real estate. When this article was published, David Sangree was Director of Hospitality Consulting with US Realty Consultants and a Principal in the Cleveland office. |

| Contact:

David J. Sangree, MAI, CPA, ISHC

US Realty Consultants

|

| Also See: | Hotel Capitalization Rates Drop Further / May 2005 |

| Cleveland�s Lodging Market: A Slow Climb Back / David J. Sangree & Joseph Pierce/ February 2005 | |

| Indoor Waterpark Resorts Continue Impressive Growth in �05; a Viable Segment of the Travel / David J. Sangree / January 2005 | |

| Indoor Waterpark Resorts Expand Nationwide / David J. Sangree / April 2004 | |

| Cleveland Lodging Market at Bottom with Improvement Predicted / US Realty Consultants, Inc. / January 2004 | |

| Hotel Capitalization Rates Drop Again / David J. Sangree, MAI, CPA, ISHC / April 2004 | |

| Appraisal and Financing of Indoor Waterpark Resorts / David J. Sangree / October 2003 | |

| Hotel Capitalization Rates Drop / David J. Sangree, MAI, CPA, ISHC / February 2003 |