U. S. Lodging

Industry Analysis

-

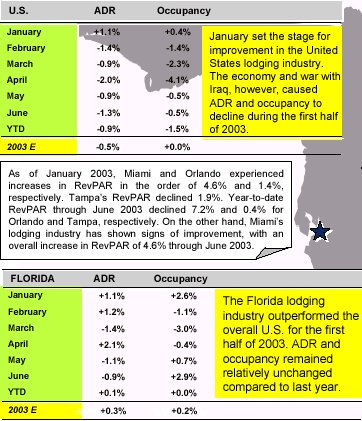

The U.S. lodging market posted its second annual year-over-year decline

and another disappointing year in 2002 as rooms revenue decreased approximately

0.8 percent compared to 2001 levels. The prolonged weakness in the U.S.lodging

market is primarily attributed to travel fears surrounding the war with

Iraq, international travel concerns due to SARS, and the sluggish recovery

of corporate travel. Despite the industry�s prolonged challenges, the lodging

market is poised for recovery in the long-term. Lodging demand is anticipated

to be stagnant throughout the remainder of the year with anticipated sustainable

recovery in the second half of 2004.

-

The airline industry continues to be challenged by adverse market conditions,

as evidenced by the bankruptcy of United Airlines in December of 2002.

Passenger levels on U.S. airlines declined 2.8 percent from year-to-date

2002 levels through May, according to the Air Transport Association of

America. Furthermore, during the first half of 2003, Miami, Orlando, and

Tampa experienced declines in air traffic of 3.9 percent, 1.1 percent,

and 2.7 percent, respectively. Though airline passenger levels are beginning

to exhibit signs of recovery, it is not anticipated to significantly increase

in the short-term due to continued corporate reduction in business travel

and the growing preference of domestic leisure travelers for drive-in vacation

alternatives.

-

Though many airlines are reducing flights and the growth rate for air travel

is at an all-time low, auto travel for April increased 6.7 percent over

2002 according to Travel Statistics & Trends, indicating that Americans

are choosing to stay close to home. In fact, more than half of leisure

trips this summer are anticipated to be four nights or fewer in length.

Domestic summer travel is anticipated to play a key role in the U.S. lodging

market�s performance, with average vacations anticipated to increase in

cost by 9.5 percent from 2002 to $2,378 and 80 percent of U.S. travelers

are anticipated to take a vacation this summer.

Florida Lodging

Industry Overview

-

Florida�s unemployment rate during the month of June was approximately

5.6 percent, 0.9 percentage points lower than that of the United States

and 3.4 percentage points lower than in June 2002. Miami-Dade county�s

unemployment rate in June 2003 was the highest in the state, registering

at 7.7 percent.

-

Florida recorded a banner year during 2002 in the number of visitors coming

to the state,reaching an all-time high of 75.6 million. This was mainly

attributed to an increase in drive-In demand, which represented 52 percent

of all visitors to the state. Additionally, in March 2003, Governor Bush

told the Visit Florida board that $10 to $20 million would be allocated

to tourism from the requested $40 million contingency fund to ease any

war-related slump in the state economy,compared to the $9 million the agency

normally spends annually.

-

During the first quarter of 2003, Florida received an estimated 20.1 million

visitors, a 0.2 percent increase over the same period during the prior

year despite an economic slowdown and the war with Iraq. Florida�s domestic

visitation declined 0.5 percent to 18.1 million, while overseas visitation

was up six percent to 1.2 million. Canadian visitation experienced a gain

of 8.0 percent to approximately 800,000 people.

-

The latest national survey by Travel Industry Association of America (TIA)

indicates domestic travel within the U.S. should increase approximately

2.5 percent this summer. Florida is tied with California as being number

one on these travelers� summer destination �wish list.�

-

Struggling European and Latin American economies contributed to a sharp

downturn in the state�s international visitation in 2001 and 2002. The

weakened U.S. dollar, however, is expected to make visitation to the United

States more attractive to European travelers, positively impacting tourism

in Florida in 2003.

-

The federal government recently passed legislation requiring computer-

friendly passports by October 2003 for foreign visitors from 27 countries

and biometric identifiers by October 2004. Given that Florida�s international

visitors account for approximately 10 percent of the state�s total visitation,

state officials are concerned this legislation could have a negative impact

on visitation to the state.

-

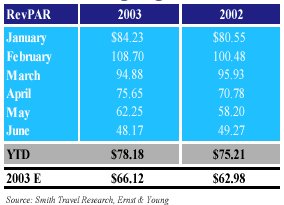

Florida�s lodging market is beginning to perform above 2002 levels. Year-to-date

occupancy as of June 2003 was 65.4 percent, at the same level as 2002.

Year-to-date average daily rate was $97.02, 0.1 percent above the same

period during 2002, resulting in an increase in RevPAR of approximately

0.2 percent. Reductions in corporate and group travel, as a result of a

persistent soft economy, have contributed to the slow improvement of the

Florida market.

-

New supply additions in Orlando (approximately 5,308 rooms over the last

two years) continue to place downward pressure on occupancy, yet should

positively contribute to average rates in the long-term due to their primarily

upscale positioning. Similarly, Miami experienced a 1.4 percent increase

in supply during the first half of 2003, mainly in the luxury segment.

These high- profile additions are anticipated to meet a definitive need

from incentive travel, convention and high- end leisure segments.

Miami Lodging

Market Analysis

-

Preliminary

reports indicate that visitation was lower during the first half of 2003,

according to the Greater Miami Convention & Visitors Bureau. This is

mainly attributed to a 3.9 percent decline in air passenger arrivals through

June 2003 relative to the same period in 2002. Domestic visitation declined

4.5 percent while international visitation declined 3.2 percent over the

same period. Preliminary

reports indicate that visitation was lower during the first half of 2003,

according to the Greater Miami Convention & Visitors Bureau. This is

mainly attributed to a 3.9 percent decline in air passenger arrivals through

June 2003 relative to the same period in 2002. Domestic visitation declined

4.5 percent while international visitation declined 3.2 percent over the

same period.

-

Miami Beach Convention Center attendance for the first half of their fiscal

year (10/02 to 3/03) declined 9.7 percent compared to the same period during

the prior year. According to the Miami Beach Convention Center, an overall

decline of 1.3 percent in attendance is anticipated through September 2003.

-

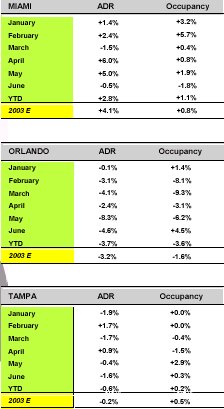

Recently, Miami was ranked first for ADR growth, second for RevPAR growth,

and fourth in occupancy growth among the top 25 lodging markets during

the first half of 2003, according to Smith Travel Research. Year-to-date

occupancy, ADR, and RevPAR increased 1.1 percent, 2.8 percent, and 3.9

percent, respectively, compared to the same period during 2002; however,

operating performance is still below year-to-date June 2001 levels by 9.1

percent, 3.3 percent,and 12.0 percent in terms of occupancy, ADR, and RevPAR,

respectively.

-

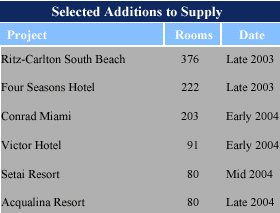

The

Miami luxury hotel market continues to forge ahead with new developments

over the next 12 to 18 months. The 376-room Ritz-Carlton South Beach, originally

scheduled to open in late 2002, will open in late 2003. The Four Seasons

Hotel & Tower will be opening in October 2003. The introduction of

the first Conrad International, Hilton�s luxury brand, to the U.S. is scheduled

for January 2004. ZOM�s redevelopment of the 91-room Victor Hotel, anticipated

to be operated by Hyatt Hotels Corporation, is expected to open on South

Beach in early 2004. The

Miami luxury hotel market continues to forge ahead with new developments

over the next 12 to 18 months. The 376-room Ritz-Carlton South Beach, originally

scheduled to open in late 2002, will open in late 2003. The Four Seasons

Hotel & Tower will be opening in October 2003. The introduction of

the first Conrad International, Hilton�s luxury brand, to the U.S. is scheduled

for January 2004. ZOM�s redevelopment of the 91-room Victor Hotel, anticipated

to be operated by Hyatt Hotels Corporation, is expected to open on South

Beach in early 2004.

-

Rosewood�s 80- unit Acqualina Resort is anticipated to open in Sunny Isles

Beach in late 2004. An 80-unit Regent condominium-hotel on South Beach

is also planned for early 2005.

-

Several new additions to supply remain in the early planning stages. One

Bal Harbour, a mixed-use development on Collins Avenue, is anticipated

to feature a 25-story residential tower with 185 units and a 17-story luxury

hotel with 124 suites. A hotel operator has not been selected yet; however,

negotiations are reportedly underway. A luxury hotel with a fractional

interest component, an upscale hotel, and a mega-yacht marina on Watson

Island is also planned.

-

Occupancy is anticipated to slightly increase in 2004 while ADR is anticipated

to moderately increase. Growth in average rate is anticipated to primarily

be the result of additional luxury supply versus real year-over-year growth

and will be subject to competitive pricing during the off-season.

Orlando Lodging

Market Analysis

-

Year-to-date

figures through June 2003 indicate that airport passenger traffic decreased

1.1 percent relative to the same period during the prior year. Year-to-date

international passenger air traffic through June 2003 continues to improve,

as exhibited by an increase of 3.9 percent compared to the same period

in 2002. Nevertheless, airport representatives indicated that the south

terminal, originally slated for June 2005, has been delayed due to uncertainty

of when demand will support a new terminal coupled with the need to accommodate

new security systems. Year-to-date

figures through June 2003 indicate that airport passenger traffic decreased

1.1 percent relative to the same period during the prior year. Year-to-date

international passenger air traffic through June 2003 continues to improve,

as exhibited by an increase of 3.9 percent compared to the same period

in 2002. Nevertheless, airport representatives indicated that the south

terminal, originally slated for June 2005, has been delayed due to uncertainty

of when demand will support a new terminal coupled with the need to accommodate

new security systems.

-

Convention center events decreased 14.1 percent year- to-date through April

2003 while attendance increased 5.6 percent as compared to the same period

during the prior year, according to the Orlando/ Orange County Convention

& Visitors Bureau (�CVB�). This was driven primarily by strong performance

in January, February, and April. The one million- square foot expansion

of the Orange County Convention Center, to be completed in October 2003,

is anticipated to generate a 27 percent increase in attendance in 2004,

according to the CVB.

-

According to market representatives, Disney�s park attendance declines

have adversely impacted lodging performance in the area. During 2002, attendance

remained 12.8 percent below 2000 levels.

-

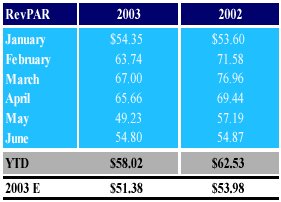

During the first half of 2003, occupancy, ADR and RevPAR declined 3.6 percent,

3.7 percent, and 7.2 percent, respectively, as compared to the same period

during 2002. Orlando�s operating performance is still below 2001 levels

by 9.5 percent, 6.2 percent, and 15.2 percent in terms of occupancy, ADR

and RevPAR, respectively.

-

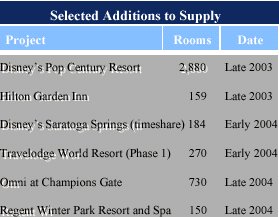

In

terms of new supply, the 1,000 room J.W. Marriott and 584-room Ritz-Carlton

at Grand Lakes recently opened in July 2003. The proposed 1,500- room Hyatt,

the 1,200- room Hilton, and the 1,000-room expansion of The Peabody currently

remain on hold. Other hotel projects are still underway, including the

2, 880- room Disney Pop Century Hotel (Phase I) and the 730-room Omni at

Champions Gate. The 1,500- room Rosen Hotel is anticipated to open in January

2006. The resort, located adjacent to the convention center expansion and

Beeline Expressway, will feature approximately 250,000 square feet of meeting

space, an 18-hole golf course, and full-service spa. In

terms of new supply, the 1,000 room J.W. Marriott and 584-room Ritz-Carlton

at Grand Lakes recently opened in July 2003. The proposed 1,500- room Hyatt,

the 1,200- room Hilton, and the 1,000-room expansion of The Peabody currently

remain on hold. Other hotel projects are still underway, including the

2, 880- room Disney Pop Century Hotel (Phase I) and the 730-room Omni at

Champions Gate. The 1,500- room Rosen Hotel is anticipated to open in January

2006. The resort, located adjacent to the convention center expansion and

Beeline Expressway, will feature approximately 250,000 square feet of meeting

space, an 18-hole golf course, and full-service spa.

-

In order to maintain their competitive posture, both the Marriott Orlando

World Center and the Swan/Dolphin are undergoing significant renovations

of both guestrooms and public areas and adding meeting space.

-

Occupancy is anticipated to slightly increase in 2004, while ADR should

remain unchanged relative to 2003.

Tampa Lodging

Market Analysis

-

Year-to-date

figures through June 2003 indicate that airport passenger traffic declined

2.7 percent relative to the same period last year. Domestic visitation

declined 2.8 percent while international visitation declined 0.5 percent

over the same period. Year-to-date

figures through June 2003 indicate that airport passenger traffic declined

2.7 percent relative to the same period last year. Domestic visitation

declined 2.8 percent while international visitation declined 0.5 percent

over the same period.

-

The Tampa Bay Convention & Visitors Bureau is initiating an innovative

marketing campaign that offers meeting planners an opportunity to write

and submit their own version of an ideal contract for later discussion

to boost meeting group demand. The campaign opens the door for the meeting

planner to submit a proposal with a �zero� rooms attrition clause, or a

Food & Beverage attrition �waived� clause that is not guaranteed, but

subject to a �serious� discussion. The Tampa Bay Convention & Visitor

Bureau also commissioned an extensive study that justified doubling the

current space of 279,000 square feet at the Tampa Bay Convention Center.

In 2003, the convention center is anticipated to slightly exceed the 175,000

room nights its events generated in 2002. The convention center expects

to generate 200,000 room nights in 2004 and 210,000 in 2005.

-

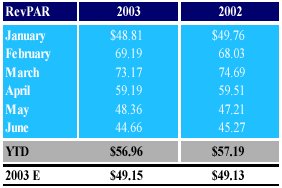

Year-to-date occupancy in the Tampa area improved slightly relative to

2002 levels. Occupancy through June 2003 reached 66.1 percent, only 0.2

percent above 2002 levels during the same period. ADR and RevPAR declined

0.6 percent and 0.4 percent, respectively. Furthermore, Tampa remains below

2001 operating performance levels by 6.5 percent, 8.2 percent, and 14.2

percent in terms of occupancy, ADR and RevPAR, respectively.

-

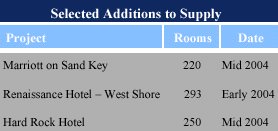

In

terms of new supply, the West Shore lodging market will receive its first

new upscale hotel property in mid 2004. A 293-room Renaissance Hotel is

currently under development by CNL Financial Group, Inc. The hotel is also

CNL�s first property in the Tampa Bay area and will be located at the International

Plaza shopping center, within one mile of Tampa International Airport.

Additionally, Marriott International is converting the Radisson Suites

on Sand Key into the first full-service Marriott in Pinellas County in

January 2004. In

terms of new supply, the West Shore lodging market will receive its first

new upscale hotel property in mid 2004. A 293-room Renaissance Hotel is

currently under development by CNL Financial Group, Inc. The hotel is also

CNL�s first property in the Tampa Bay area and will be located at the International

Plaza shopping center, within one mile of Tampa International Airport.

Additionally, Marriott International is converting the Radisson Suites

on Sand Key into the first full-service Marriott in Pinellas County in

January 2004.

-

Construction for the Hard Rock Hotel & Casino Resort is also underway.

The hotel, scheduled to open in March 2004 and located in the Seminole

Indian Nation reservation, represents an economic generator that will add

1,500 jobs. The proposed resort will feature 250 rooms, ten restaurants,

and 10,000 square feet of meeting space. The first phase of the 90,000-

square foot casino operation opened in June 2003.

-

Additionally, negotiations are underway between an Indiana hotel developer

and city officials to build a 400-unit Embassy Suites hotel across Franklin

Street from the Tampa Convention Center.

-

Both occupancy and ADR are anticipated to slightly increase in 2004.

|