| Quarterly Trends in

the Hotel Industry

United States |

|

|

Post-Recession, Post-Catastrophic Event, Post-War, Post-SARS First Quarter Results |

For the U.S.lodging industry, 2003 was supposed to be the year of the

turnaround. The anticipation of economic recovery, combined with

a slowdown in new hotel development,was expected to set the course for

improved occupancy levels, followed by increases in average daily room

rates. Unfortunately, sustained economic growth has yet to emerge to the

degree that U.S.businesses will have the confidence to increase their investment

in travel.In addition, the travel industry has taken direct hits from the

war in Iraq, as well as SARS and domestic terrorism alerts.

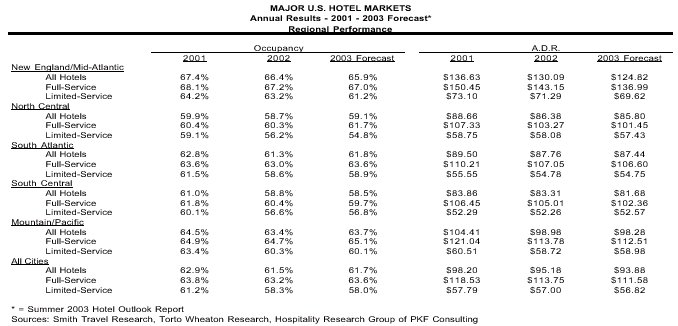

Warm Markets Are Hotter In good times and bad,some markets outperform others. Such was the case during the first quarter of 2003. In general, those markets that experience their �in-season� during the winter months did show some signs of improvement in their first quarter 2003 performance over the first quarter of 2002. Markets such as Fort Lauderdale, Miami, Honolulu, Phoenix,and San Diego all achieved year-to-year growth in RevPAR during the first quarter.The majority of these RevPAR gains were driven by improvement in market occupancy. However, both San Diego and Honolulu hotels enjoyed gains in ADR of 7.1 percent and 3.4 percent, respectively. The relatively strong performance of these warm weather winter destinations is consistent with national trends in lodging demand. Most hotels are reporting that business and convention travel continues to be below the levels experienced in 2000. Leisure travel, by contrast, has held up relatively well.In recent history, we noticed that, during recessions, leisure travel habits may change (destination, cost, mode of travel, duration, etc �), but vacations are not totally eliminated. Business and convention travel, however,does fall off due to cuts in corporate and association budgets. The areas experiencing the greatest declines in RevPAR were the Northeast

and South Central regions. On average, the hotels in the major cities of

these regions experienced declines in both occupancy and ADR. The ability

of hotels in the North Central and South Atlantic regions to achieve slight

improvements in ADR enabled these properties to mitigate the movement of

their RevPARs. Hotels in the Mountain and Pacific region were the only

ones to enjoy an increase in occupancy, which drove the region�s 0.9 percent

growth in RevPAR during the first quarter.

|

| Pace Quickens Somewhat

By year-end 2003, The Hospitality Research Group and Torto Wheaton Research (HRG/TWR) forecast that the hotels in the nation�s largest markets will achieve an occupancy of 61.7 percent and an average daily room rate of $93.88. These measurements represent a 0.3 percent improvement in occupancy compared to 2002, but a 1.4 percent decline in average daily rate. The net result is a 2003 RevPAR of $57.91, a level that is 1.1 percent less than the RevPAR recorded for 2002. What these projections imply is a slight improvement in occupancy during

the last three quarters of 2003 compared to the same period in 2002. Unfortunately

for hoteliers, we estimate that the average room rate paid by guests during

the latter months of 2003 will continue to be less than that paid in 2002.

While sluggish rate growth might be a benefit for travelers, declining

ADRs have historically contributed to declining profitability for hotel

owners and operators.

2002 Recap (vs 2001) |

|

|

>

| Two Different Paths

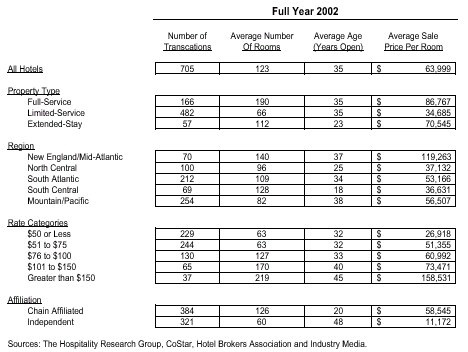

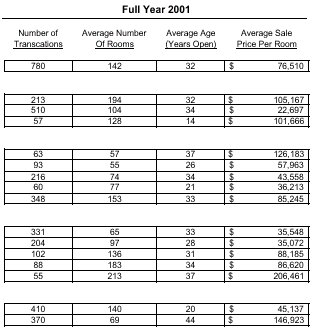

As it has with geography, hotel performance is expected to differ by property type during the remainder of the year. For the rest of 2003,HRG/TWR is forecasting that full-service hotels will experience a moderate increase in occupancy relative to that achieved in 2002. Conversely,ADRs will continue to lag behind 2002 rates by roughly 2.0 per-cent. We attribute this performance pattern to the return of commercial and con-vention travelers who will continue to prefer full-service hotels, but need to be coaxed back to the road (and away from limited-service properties)by discounts. A similar performance scenario is projected for limited-service hotels for the rest of 2003.For the latter part of the year, HRG/TWR forecasts limited-service occupancies and ADRs to improve from their first quarter performance, but still to fall behind the annual occupancy and ADR posted for 2002. Poor Profit Projection Given our 2003 forecast for a slight increase (0.3 percent) in occupancy, combined with a 1.4 percent decline in room rates, HRG estimates that the average U.S. hotel will experience a 2.3 percent decline in operating profits from 2002 to 2003. This estimate is based on the assumption that management will be able to hold their operating costs to 2002 levels,despite inflation and the fact that the increased occupancy will cause a rise in variable costs. Favoring management�s ability to control costs is the prospect of deflation in some cost categories (utilities), rising unemployment, and recent movements to lower insurance costs. Wobbly Legs For the nation �s hotel owners and operators, the encouraging news in 2003 is the projection of improved occupancy. Based on the performance patterns observed during the recessions of the early 1980s and 1990s, growth in occupancy is typically the first sign of industry wide recovery. Significant improvements in ADR have typically followed one to two years later. All the pieces are currently in place for a recovery within the lodging industry: limited increases in supply, economic growth, and no imminent military hostilities. However, as we have observed in the past two years, the state of the economy in general, and the lodging industry in specific, is very fragile. �Adverse selection� is a term used by economists to describe market conditions under which too many trades of low-quality goods or services occur because buyers lack the ability to distinguish high from low quality. The low-quality products and services continue to be offered in the market because reliable information about quality is difficult for buyers to obtain. The hotel real estate market during 2001 and 2002 resembles an adverse selection market, but not due to information about properties being hard to find. This adverse selection market originates from the types of assets that the owners have been willing to offer for sale. High quality assets either do not appear on broker listing sheets or are listed at such high prices that a large spread results between a buyer�s bid and the seller�s asking price (i.e .,a large bid / ask spread). Many less desirable assets have traded over the past two years as the consequence of �portfolio pruning � and seller financial distress. The information about hotel real estate sales during 2001 and 2002,

presented in the accompanying table, provides evidence of declining asset

quality in the U.S. market. Both the number of transactions and the prices

per room dropped from 2001 to 2002 just asthey did during the previous

period. Overall, the price per room fell by over 16 percent,which outdistanced

the decreases in hotel RevPARs for the year. The percent decline, however,is

somewhat misleading because the size of sold properties in 2002

|

Trends in the Hotel Industry

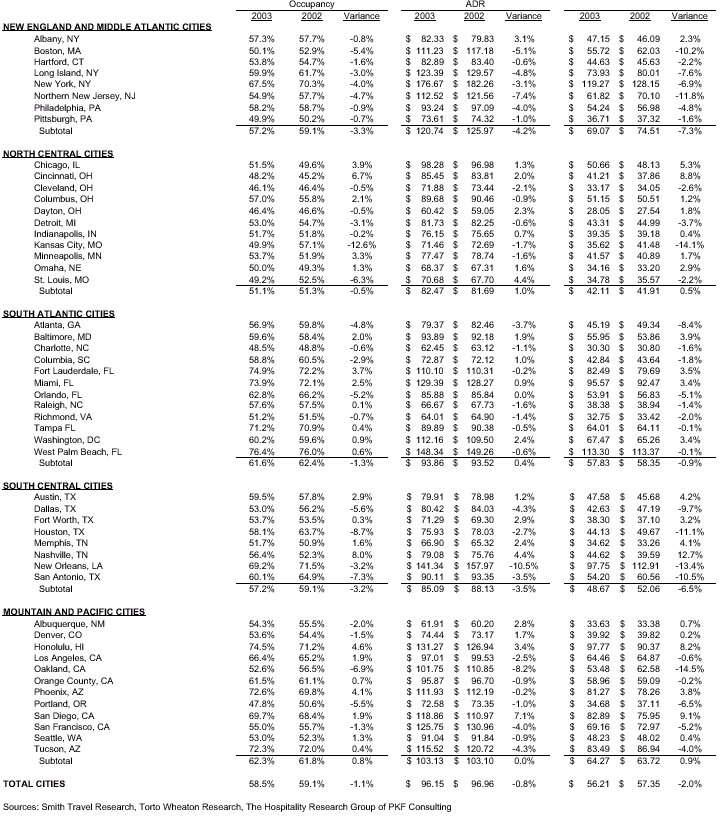

United States Cities - First Quarter Results for 2003

| The hotel real estate sales database maintained by HRG offers many insights about the pricing of hotel properties. Customers may access these data for specific property information by ordering a Price Ranger report (contact Claude Vargo at [email protected] or 404-842-1150 X237. Custom research (e.g .,price indexes for different hotel markets) using these data also can be obtained (contact Jack Corgel at [email protected] or 404-842-1150 X227). |

| Contact:

PKF Consulting 425 California Street Suite 1650 San Francisco,CA 94104 Telephone (415)421-5378 Telefax (415)956-7708 http://www.pkfonline.com |