|

|

|

|

|

|

|

|

Rates Go Up or Down? |

| By: Dr. Jack Corgel, August 2003

For many in the hotel industry, the ratio of property-level operating income and asset market pricing - the capitalization or �cap� rate - provides an important foundation for rational investing and financing decisions. During periods, such as the recent past, when both the numerator and denominator of the ratio experience different magnitudes of movement, hotel cap rate interpretations become especially difficult for everyone in the industry. The topic addressed in this article is the near-term direction of hotel cap rates. If the rate increases, then the pace of property transaction activity and development will be slower than if rates decline. Based on the conceptual arguments presented below, the probability of hotel cap rates declining in the short run exceeds the probability of rates increasing. Hotel Cap Rates Appear Counter Cyclical Exhibit 1 presents a ten-year history of cap rates for full-service

hotels in the U.S. The information comes from the Real Estate Research

Corporation (RERC). The RERC conducts quarterly surveys of institutional

real estate investors and lenders to assemble consensus estimates of key

market performance indicators. The hotel cap series from RERC dates back

to 1992.

Hotel cap rates appear to move in a counter-cyclical pattern. The highest rate of slightly above 12% occurred at the end of the early-1990s recession. The average rate reached 11.7% during the recent recession, but fell sharply over the past two quarters. Hotel cap rates moved downward and broke through the 10% barrier for several quarters in 1997 and 1998 when the economy was rapidly expanding. In theory, hotel cap rates should conform to the counter-cyclical pattern they followed during the past ten years. Current Spreads Are Wide Another perspective on hotel cap rates comes after examining historical

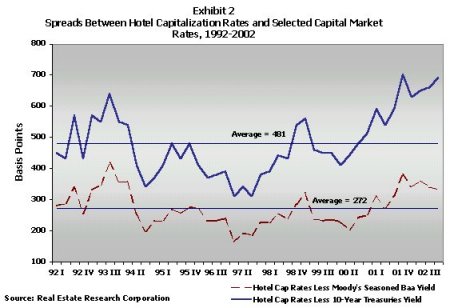

spreads between this rate and other capital market rates. Exhibit 2 shows

hotel cap rates relative to ten-year Treasuries and the Moodys Baa corporate

bond series since 1992. As with rate levels, the spreads appear counter-cyclical.

This means that hotel risk premiums move above the long-run average during

recession and below the average during periods of economic expansion. Average

spreads equal 481 basis points above ten-year Treasuries and 272 basis

points over Moodys Baa bonds. In 2002 IV, hotel cap rate spreads stood

at or near the ten-year historical highs.

Cap rates for full-service hotels declined from a peak of 11.7% in 2002 II to 10.9% by the end of 2002. The current rates almost equal the ten-year average of 10.8%. The wide spreads between hotel cap rates and capital market benchmarks indicates that these rates could fall by more than a few basis points to bring spreads back in line with historical average spreads. Components of Hotel Cap Rates Sophistically Quantitative models can generate in objective ways point estimates of future hotel cap rates. Sometimes only the future direction of market indicators is needed. In these instances, breaking down the performance measure into its component parts may form the basis for conclusions about which way the market is likely to move. Two insights come from the decomposition of hotel cap rates. The hotel cap rate is equal to the discount rate minus the assumed growth rate. The hotel cap rate has moved upward by the same number of basis points as the discount rate during the past few years. This suggests that the assumed growth rate remained stable. The reason for the stability is that the growth rate refers to the change in NOI and not the change in revenues. NOI has been much more stable during this recession than in previous ones because of hotel managements� ability to reduce costs quickly in response to falling revenues. The discount rate for hotel investment, as for other real estate investments, equals an observable risk-free rate (such as the return on Treasury notes) plus an unobservable premium return for risk. While the risk-free rate declined over the past few years, the discount rate for hotel investments has risen somewhat. This indicates that the increase of the discount rate was due to a sizeable increase in the risk premium. Hotel Cap Rate Forecasts As indicated in Exhibit 1, the hotel cap rate now stands slightly above the historical average of 10.8%. As indicated in Exhibit 2, the spreads in 2002 between hotel rates and other capital market rates reached the highest levels recorded since 1992. Both of these observations indicate spreads should narrow. With the growth rate remaining somewhat stable over the last several years, expected income growth rates may not change as much during recovery as some anticipate. Assuming a fairly constant growth rate going forward, the narrowing of spreads can only occur in two ways. First, the risk-free rate may increase because either inflation or real rates go up. Most macroeconomic forecasting firms envision a fairly level near-term inflation rate. The historically stable real rate, however, has experienced downward pressure during this period of recession, catastrophic events, war, and human virus. The prices of Treasury benchmarks have been bid up to a point where yields reflect the current low inflation plus a historically thin real rate. Some economists speculate that once the focus returns to business as usual that a �market correction� in Treasuries will occur as investors move money out of risk-free assets into risky investments. The decline in the prices of Treasuries will raise yields, therefore contributing to a narrowing of spreads. Second, the risk premium may come down as the hotel markets enter a period of renewed stability. The rise in hotel investment risk premiums has been dramatic in recent years. This is likely due to investor perceptions about hotel performance during economic downturns relative to safer investments. In conclusion, the hotel cap rate should experience a modest decline over the next year. Largely, this decline will be due to a falling risk premium as the level returns to the historical average. Even if the risk-free rate increases, the movement should not offset the decline in the risk premium. Changes in the expected growth of hotel NOI are not expected to be a major factor in the near-term determination of cap rates. To purchase a copy of the 2003 edition of Trends in the Hotel Industry, visit the HRG website at www.hrgonline.com. Jack Corgel is the Managing Director of Applied Research for The Hospitality Research Group of PKF Consulting. Alexander Feneck, a Research Coordinator for HRG, assisted with this article. Both are based in the firm�s Atlanta office. |

| Contact:

Jack Corgel, Ph.D. Managing Director Hospitality Research Group 3340 Peachtree Road, Suite 580 Atlanta, GA 30326 (404) 842-1150 x227 |

| Also See: | Will

Hotel NOIs and Property Prices Follow Revenues in Their Downward Spiral?

/

John (Jack) B. Corgel,

Ph.D / Hospitality Research Group of PKF Consulting / June 2002 |

| Hotel

Loan Problems On the Rise Again; Prolonged Hotel Market Weakness Taking

a Toll / PKF / June

2003 |