|

Lodging Report |

|

|

|

Lodging Report |

| August 2003

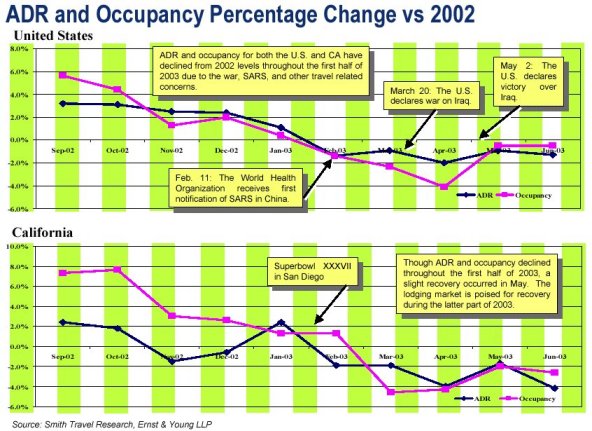

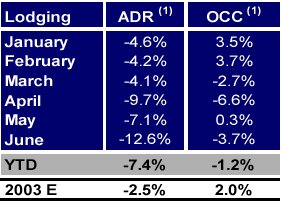

Macroeconomic Observations The U.S. economy continued to be challenged in the first half of 2003; however, recovery is within sight due in part to aggressive fiscal and monetary policies that are anticipated to stimulate the economy with above recent average annualized growth rates during the second half of 2003 and 2004. The Federal Reserve�s proactive monetary policy resulted in an additional quarter percent reduction in short-term interest rates in June to the lowest level since 1958. The federal government�s proposed tax reductions are, coupled with the recent surge in the U.S. equity markets, anticipated to revive consumer spending well beyond the summer months and into 2004. GDP growth during the first quarter was a modest 2.2 percent and declined

to 1.9 percent for the second quarter of 2003. Economists anticipate a

3.0 to 3.5 percent annualized GDP growth during the second half of 2003

and approximately 4.0 percent annualized growth in 2004.

The national unemployment rate was 5.7 percent in January and increased to 6.4 percent in June, its highest level in nine years. With the high unemployment rate, the Consumer Confidence Index decreased to 76.6 in July, dropping seven points from June, indicating that consumers are still not confident about the prospect for an economic recovery occurring throughout the remainder of 2003. The Consumer Confidence Index is, however, anticipated to increase as employment levels increase and the economy stabilizes towards the end of the year and into 2004. U.S. Lodging Industry Analysis

The airline industry continues to be challenged by adverse market conditions, as evidenced by the bankruptcy of United Airlines in December of 2002 and the bankruptcy of Hawaiian Airlines in March of 2003. Passenger levels on U.S. airlines declined 2.8 percent from year-to-date 2002 levels through May, according to the Air Transport Association of America. Though airline passenger levels are beginning to exhibit signs of recovery, it is not anticipated to significantly increase in the short-term due to continued corporate reduction in business travel and the growing preference of domestic leisure travelers for drive-in vacation alternatives. Though many airlines are reducing the number of flights and the growth

rate for air travel is at an all- time low, auto travel for April increased

6.7 percent over 2002 according to Travel Statistics & Trends, further

indicating that Americans are choosing to stay close to home. In fact,

more than half of leisure trips this summer are anticipated to be four

nights or fewer in length. Domestic summer travel is anticipated to play

a key role in the U.S. lodging market�s performance, with average vacations

anticipated to increase in cost by 9.5 percent from 2002 to $2,378 and

80 percent of the U.S. traveler anticipated to take a vacation this summer.

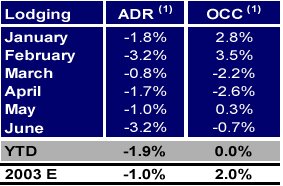

California�s increasing budget deficit (approximately $38 billion), the lackluster technology sector and reduced international travel are threatening to affect California tourism throughout the remainder of 2003. Some optimism exists with respect to favorable expectations for summer travel, most notably as it relates to continued strong drive-in demand. The continuation of the weak dollar is anticipated to encourage domestic travelers to stay local and potentially motivate international travelers to travel to the United States and specifically California. California�s lodging market continues to outperform the U.S. in terms of RevPAR. Through June, RevPAR for California was $58.59, while RevPAR for the U.S. was $48.70, approximately 16.9 percent lower. The California lodging industry, however, continues to perform below 2002 levels with RevPAR through June approximately four percent below the prior year period. Although well below 9/11/01 levels, both leisure and business travel are anticipated to recover somewhat in the second half of the year. Leisure travel is anticipated to increase 4.0 percent over last summer, according to the California Division of Tourism, and business travel is anticipated to rebound slightly with an expected 1.4 percent increase versus summer 2002. Governor Davis�s most recent budget proposal includes a $2.5 million budget for the State Division of Tourism, less than half of the original $7 million budget. California Mid- Year Top 10 Thoughts 1. The Decline in Corporate Travel � Though it is anticipated that corporate travel budgets will increase 6.5 percent in 2004, corporate travel is not anticipated to recover to pre- 2001 levels in the near- term. The new-reality imposed by geopolitical events, economic downturn and, more recently, the numerous corporate SARS- related travel restrictions, have forced companies to re- evaluate travel spending and many are realizing that time and money can be saved by investing in technology, such as videoconferencing, rather than travel. Many companies are citing reduced travel expenses as a reason their corporate earnings have increased. Due to the fact that corporate travelers historically paid premium room rates, the continued lack of corporate travel is anticipated to further dampen ADR and occupancy conditions throughout the United States and California, particularly in areas traditionally dependent upon corporate travel. Primary Impact: Average Daily Room Rate 2. Drive- in Demand � The California Division of Tourism estimates that 98.5 million tourists will travel to or through California this summer, indicating an overall increase of approximately 3.4 percent over Summer 2002. Additionally, an increasing number of business travelers are choosing to travel by car, due to the long waits and frustrations surrounding security measures at airports. Californians, who represent approximately 87 percent of in- state domestic travel, are anticipated to travel approximately four percent more throughout the state this summer than last, while non- resident travel is anticipated to experience a slight decrease of approximately 0.2 percent. With its myriad of recreation alternatives and attractions, the State of California is well positioned to attract increased car travel this summer as many drive- in demand locations, such as San Diego, continue to perform well, and as Northern California enhances its marketing focus to drive- in travelers from California and Nevada. Primary Impact: Room Demand 3. International Travel Status Quo � International travel to and from California continues to be challenged due to the effects of fears surrounding SARS and terrorism. Year- to- date May 2003, international travel at Los Angeles International Airport (� LAX�) declined approximately 3.1 percent. As international travelers historically comprise approximately three percent of total visitors while contributing approximately 15 percent of total spending, this slump in international travel is anticipated to dampen traveler spending and overall hotel revenues based upon international tourists� longer average lengths of stay. Given that California is the largest gateway to Asia from the United States, the travel concern trend is anticipated to especially impact international travel to and from major California airports as travelers remain fearful of travel to Asian countries, though many travel advisories have been lifted. Creating forecasts for travel and tourism to California cities heavily dependent upon international travel will be particularly difficult as hotels and airlines approach 2004. Barring any further unforeseen political events or the continuation of the SARS outbreak, international travel is anticipated to begin to modestly recover in 2004, but little to no recovery is anticipated for the remainder of 2003. Primary Impact: Profitability 4. Indian Gaming Developments � Since Proposition 1A was passed in 1999, Indian gaming has experienced solid growth, accounting for approximately 19 percent of total industry winnings in 2002. California tribal casino revenues increased 17 percent in 2002 to $3. 4 billion, making California the largest market among the 30 states that allow Indian gaming. This growth is demonstrated by the fact that as of May 2003, 61 tribes have compacts with the State of California for casinos, and 37 more are in negotiation. Tribal casinos continue to become more comparable to the Las Vegas experience as development continues to take place throughout the state and as tribal casinos continue to compete directly with major casino markets, such as Las Vegas and Reno, in an attempt to capture greater market share. Major developments include a Las Vegas- style casino in Barstow, CA, by the Los Coyotes Band of the Cahuilla American Indian tribe, which is estimated to cost $150 million and to create approximately 2,600 jobs in the area, and the 44- acre, $250 million casino resort by the Morongo Band of Mission Indians which is anticipated to open in 2008 twenty minutes east of Palm Springs. As tribal casinos continue to become increasingly popular, hotel markets in areas such as Palm Springs, with significant gaming developments both existing and in the pipeline, will benefit from the increased traffic to the area. Primary Impact: Lodging Demand and Local Economies 5. The State Budget Deficit � The State of California continues to be hampered with a budget deficit, currently estimated at $38 billion. The state continues to have political and economic hardship, as evidenced by the governor recall and by the after- effects of the $9 billion energy crisis and the decline of the technology sector. Governor Davis�s latest budget proposal includes a budget reduction for the State Department of Tourism, and government jobs are anticipated to be eliminated in an effort to reduce government spending. This is anticipated to negatively impact California tourism as the new state budget may eliminate most, if not all, state government spending on tourism and travel to the state. This reduction in tourism spending is being partially offset by hotel taxes, as evidenced by the fact that the Agua Caliente Band of Cahuilla Indians will pay the city of Palm Springs $700,000 annually in hotel taxes for the next 20 years for tourism promotion. Primary Impact: Lodging Demand 6. The Emphasis on the Bottom Line � Faced with reduced revenues and lower occupancies, California hotels will continue to be challenged to improve their bottom line. Given California�s high cost of business, operating costs are anticipated to remain at their current levels and possibly increase throughout the remainder of 2003. Hotel operators have been particularly effected since the events of September 11, 2001, due to the rising costs of terrorism insurance, particularly in high- traffic tourism areas, such as Anaheim. Furthermore, workers� compensation expenses for California business owners have more than doubled in the past five years to approximately $15 billion in 2003, compared to approximately $6.6 billion in 1998. Workers� compensation is anticipated to increase a further 12 percent in July of 2003. A savvy operator�s focus should continue to be on improving and streamlining internal operations by cross- utilization and continued management of online distribution channels. Primary Impact: Profitability 7. Last Minute Booking Patterns � As of May 2003, approximately 41 percent of travelers who intend to travel this summer had not booked their travel plans. Due to the repercussions of the war with Iraq and the travel concern surrounding SARS, many travelers are waiting until the last minute to make their travel arrangements in an attempt to wait and see if further geopolitical issues arise. Furthermore, travelers continue to demonstrate the trend to postpone their reservations looking for last- minute bargains on room rates. Due to this trend, it has become increasingly difficult for hotel companies and airlines to forecast travel, particularly during busy summer months when most vacations occur. Primary Impact: Average Daily Room Rate 8. Internet Distribution � As the Internet continues to become a more convenient and powerful distribution channel, many hotel managers and companies are hoping to decrease their labor costs by further utilizing their websites as reservation tools and decreasing staffing levels in central reservations offices. Online booking is becoming the preferred method of corporations for making travel arrangements due to the ease of execution and the savings involved in making arrangements online. Currently, approximately 38 percent of business travelers are making reservation- related visits to hotel and airline websites, an increase of five percent from last year, with many companies claiming online airfares to be 15 percent lower than airfares made via telephone. 2002 represented the third consecutive year that companies reported significant savings by making travel arrangements online. Many discount travel websites have also begun to create discount travel packages, including air, hotel, and activities, to save customers time and money. In an attempt to combat the discount travel websites, five hotel companies (Hilton Hotels Corporation, Hyatt Corporation, Marriott International, Intercontinental Hotels Group, and Starwood Hotels and Resorts) have teamed up with Priceline. com and Pegasus Solutions Inc. to create Travelweb LLC, an online reservations system linking visitors directly to each hotel company�s central reservations system, leaving less room for reservation errors. Primary Impact: Profitability and Average Daily Room Rate 9. The Cruise Industry � The cruise industry continues to expand within California, evidenced by the new 120,000 square feet, $40 million new terminal for Carnival Cruise Lines which was opened in April in Long Beach. This terminalis anticipated to bring 300,000 passengers to the City of Long Beach each year. Carnival, along with Royal Caribbean, are hoping to attract nearby residents to the area harbors with the prospect of a short luxury trip to Mexico. Also, the Port of San Francisco plans to develop a $42.1 million cruise terminal, along with a 22- story condominium tower and 565,000 of commercial office and retail space, on 27 acres of waterfront property. Construction is anticipated to begin in 2005. Primary Impact: Lodging Demand and Increased Tourism 10. Time to Build/ Renovate/ Buy/ Sell? Build/ Renovate: The new tax- cut package created a new accelerated depreciation schedule for new investments, which is anticipated to provide developers with further incentive to build and/ or renovate. Buy/ Sell: Investors are showing a general increase in confidence in the hospitality industry. This trend should help to increase the values of hotels and an increase in hotel trades is anticipated throughout the next year and a half. The current low interest rates and a number of motivated sellers indicates that transaction activity should increase. This is evidenced by the fact that Vivendi Universal�s entertainment division recently sold the 436- room Sheraton Universal Hotel in Universal City to Walton Street Capital for $49 million, and The Jack Parker Corporation purchased the 107- room Givenchy Resort and Spa in Palm Springs in June 2003, and will become the new Le Parker Meridien Palm Springs. Other notable hotels for sale include the 637- room Hollywood Renaissance Hotel and the 485- room Hyatt Regency Los Angeles. Also, it has been reported that the Beverly Hilton in Beverly Hills is being marketing for sale. Primary Impact: Sales Transactions and Hotel Values San Francisco Lodging Market Analysis

According to the San Francisco Convention and Visitors Bureau, 13.7 million people visited the San Francisco area in 2002, reflecting a 12.5 percent decline in visitors and a 9.2 percent decline in visitor spending from 2001 levels. This decline in visitor spending is anticipated to continue due to decreased international travel and numerous corporate travel reductions. The Moscone Convention Center opened its new expansion project, �Moscone West,� in June. This expansion provides an additional 300,000 square feet to bring the total function space to more than 900,000 square feet. The additional space will help to attract larger conventions to the area. Currently, 89 pre-opening bookings are already scheduled through 2012, representing 1.18 million room nights, and are estimated to bring $958 million in conventioneer spending to the San Francisco area. Through the end of June, 22 conventions have taken place at the Moscone, and 25 more are scheduled throughout the remainder of the year, with a total number of expected visitors to be 1,011,080, up nine percent from 2002. The San Francisco travel market continues to be hampered by recent events

as traffic at the San Francisco International Airport declined nine percent

from last year through April. Domestic travel was down 7.9 percent, while

international travel, largely impacted by the lack of Asian travel due

to SARS, declined 11.1 percent. The expansion of the San Francisco International

Airport, which many business leaders view as critical to the region�s economic

future, is currently on hold indefinitely due to poor economic conditions.

Los Angeles Lodging Market Analysis

Real estate development in Downtown LA continues to generate a significant

level of interest as city officials and private developers alike are seeking

to revitalize the area, as 16 current residential projects are in the planning

and/ or development stage. Additionally, LA continues to be challenged

as a convention destination, due to the absence of a major convention center

hotel. However, a $1 billion hotel/ retail complex, to be developed by

AEG near the Staples Center, is in the planning stage. This complex would

include a 7,000 seat theater, the future home of The Academy of Television

Arts and Sciences� Emmy Awards.

The new 120,000 square feet, $40 million new terminal for Carnival Cruise Lines, which opened in April, should bode well for the Long Beach area. The Carnival Cruise Lines terminal is anticipated to bring approximately 300,000 passengers to Long Beach each year. Anaheim/Orange County Lodging Market Analysis

Many large hotels in Orange County are becoming increasingly dependent upon conventions and groups to boost their occupancy during the low demand periods. The importance of conventions is demonstrated by the fact that 900,000 conventioneers visited the Anaheim Convention Center in 2002, and conventions are anticipated to bring an estimated $4 billion in economic impact during the next ten years to the area. In anticipation of these visitors, the Anaheim Convention Center completed a $180 million expansion project in April of this year, now offering 40% more function space (1.6 million square feet total). The project represents the cornerstone of a new 1,100 acre district called Anaheim Resort, which includes Disney�s $1.4 billion California Adventure, Downtown Disney, walkways, and will also include the new Anaheim Garden Walk. In a continuing effort to attract more visitors to Orange County, the Anaheim Resort District underwent a five billion dollar renovation in 2001, and construction commenced once again in May 2003 on the Anaheim Garden Walk, an open-air plaza of shops and restaurants. This new development will become part of the Resort District with four onsite hotels, adding more than 1,600 rooms to the Anaheim market. Construction of the Garden Walk has begun with the anchors: a 96,000 square foot aquarium and a new commercial center, both of which are anticipated to be completed in 2004, with all construction slated to be completed by 2010. San Diego Lodging Market Analysis

The biotechnology industry continues to thrive in San Diego and expansion is prevalent. Pfizer, in the wake of its $60 billion acquisition of Pharmacia Corporation, will be expanding its La Jolla campus by adding four new buildings and a number of new employees, although the exact number has not been disclosed. Biogen of Massachusetts recently joined with Idec Pharmaceuticals of San Diego in a $6.4 billion merger, making the company the third largest biotechnology company in the world. However, their new headquarters will be located in Massachusetts, directing their corporate travel away from San Diego. Still, numerous large biotechnology companies have established branches or headquarters in San Diego in recent years, including Novartis, Johnson & Johnson, Merck and Elan. Only months after the completion of the San Diego Convention Center�s $216 million expansion, in an effort to make the center more attractive to national and international meeting planners, plans for further expansion is taking place. The expansion is still in its early planning stages, but would include a $300 million 400,000-500,000 square foot addition to be completed by 2008. The competition from Las Vegas and San Francisco, the increase in Though lodging supply growth throughout California is decreasing, the San Diego lodging market has continued to add supply due to the strong lodging market fundamentals. New hotel development includes the 750- room addition to the Manchester Grand Hyatt San Diego; a 1,100 room hotel adjacent to the San Diego Convention Center, which would include retail, restaurants, 107,000 square feet of function space, and a public park; and a $110 million, 300- room luxury hotel adjacent to Meadows Del Mar Golf Club. With the redesign of the San Diego Art + Sol magazine and website, San Diego hopes to promote itself as a world- class international cultural destination in an attempt to enhance international travel to the area. The Ernst & Young 2003 The California Mid-Year Lodging Report contains an analysis of data compiled from many source inculding Smith Travel Research. The contents of this forecast are for reference only, not to be used as business advisement or to set standards on policies or actions. © 2003 Ernst & Young |

Contact:

| Michael Fishbin

National Director, Hospitality Advisory Services (212) 773- 4906 [email protected] Troy Jones

|

Nir Liebling

Senior Analyst, Los Angeles (213) 977- 3792 [email protected] Mathew Schuster

Candace Chao

|

| Also See: | San Francisco Report / 2002 National Lodging Forecast / Ernst & Young LLP / Feb 2002 |

| San Diego Report / 2002 National Lodging Forecast / Ernst & Young LLP / Feb 2002 | |

| Los Angeles Report / 2002 National Lodging Forecast / Ernst & Young LLP / Feb 2002 | |

| 2002 California Lodging Forecast / Ernst & Young LLP / Feb 2002 |