|

|

|

|

|

|

|

2002 National Lodging Forecast Ernst & Young LLP Lodging Trends Lodging Industry Outlook Lodging Industry Segment Reports |

|

| Introduction

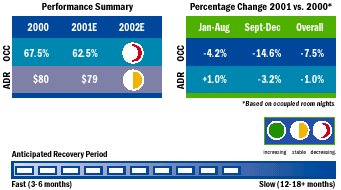

Denver�s 2001 lodging industry performed below prior expectations due to a slowing economy and the ongoing technology shakeout. Relative to the year 2000, occupancy rates during 2001 continued to decline as the year progressed while ADR growth began to moderate during the first half of the year, resulting in little to no growth as compared to the prior year. Cancellation and postponement of several major conventions and group events after September 11 resulted in metropolitan area occupancies of 50 percent to 55 percent during the month of September, as compared to typical occupancies in the range of 70 percent to 75 percent for this period. Many events were rescheduled for October, November and December, mitigating the negative impact of September�s performance on year-end results. Denver Report

Year-end 2001 RevPAR is anticipated to be approximately 7.5 percent below 2000. October year-to-date figures indicate a year-end occupancy of approximately 62.5 percent, six points below the previously anticipated occupancy. Relatively steady ADR�s are anticipated to be approximately $79 by year-end 2001, also slightly below previous expectations. Continued volatility in the technology market and increases in supply throughout the metropolitan area, are anticipated to result in slightly lower occupancies and stable ADR�s in 2002. Major Demand Changes The $268-million expansion of the Colorado Convention Center (�Center�),

doubling its capacity to 600,000 square feet, is anticipated to have the

largest positive impact on lodging demand. Local politics have pushed back

the Center�s opening date to late 2004 or early 2005, relative to the original

target of 2003. As such, short-term demand is anticipated to decrease while

the Center is under construction and major conventions take place elsewhere

through 2005. The new Invesco Field at Mile High opened in August 2001

attracting additional tourist demand to the downtown market. The stadium

will host the Denver Broncos, the Colorado Rapids, and numerous special

events.

The Denver International Airport (DIA) stepped up security measures in response to the attacks on September 11, leading to extreme delays. The general public�s reluctance to fly combined with major delays has resulted in passenger traffic declines. Furthermore, DIA�s largest tenant, United Airlines, reduced flight capacity by 32 percent following September 11. The ultimate impact of this reduction will impact demand throughout the metropolitan area. Major Supply Changes In the wake of a weak economy, political setbacks, and the events of

September 11, several significant projects have been postponed indefinitely.

The Colorado Convention Center�s 1,100-room Hyatt has been delayed due

to union protests led by the Hotel Employees and Restaurant Employees upon

approval of a $55.35 million subsidy for the project. The $220 million

hotel is now rescheduled for completion by 2005. Other planned hotel projects

in the downtown market include a $110 million renovation of the 337-room

Executive Tower and a $6 million renovation of the 430-room Westin Tabor

Center.

Additional proposed projects throughout the Denver metropolitan area include:

After overcoming numerous political and financial setbacks, the ability to complete the Colorado Convention Center expansion project in a timely manner will contribute to Denver�s competitiveness as a group destination. The Center�s postponement thus far has resulted in several lost opportunities for major conventions. In addition, the expediency with which the delays at DIA are resolved will also greatly impact Denver�s lodging industry demand. Increased security measures and insufficient airport resources continue to result in extreme delays, discouraging travel in and out of Denver. While corporate travel is slowly returning to pre-September 11 levels, near to mid-term prospects for leisure travel continue to experience uncertainty. Jeff Dallas, Los Angeles

|

###

| M. CHASE BURRITT

National Director, Hospitality Services (305) 358-4111 BOSTON

DALLAS

LOS ANGELES

|

MIAMI

Mark Lunt (305) 358-4111 NEW YORK

PHILADELPHIA

PHOENIX

|

| Also See | 2002 National Lodging Forecast / Trends, Outlook, Market Segment Reports / Ernst & Young LLP / Feb 2002 |

| 2002 California Lodging Forecast / Ernst & Young LLP / Feb 2002 | |

| 2002 Manhattan Lodging Forecast / Top 10 Thoughts for 2002 and Beyond / Ernst & Young LLP / Feb 2002 | |

| Canadian Hotel Investment Report 2002 / Colliers International Hotels / Feb 2002 |