|

Investment Report 2002 Colliers International Hotels |

|

| INTRODUCTION:

In order to properly assess today�s hotel investment market, it is important to look back when the market peaked four years ago. After a six year runup in values and transaction activity, the Canadian lodging industry slowed by mid-1998 when the capital markets collapsed and there was speculation of a North American economic recession. While a nervous Wall Street brought hotel investment to a near standstill, Canadian hotels continued to prosper and most major markets witnessed RevPAR growth in 1999 and 2000, albeit at a slower pace than in 1998. The Canadian economy continued to expand, realizing Real GDP growth of approximately 5.1% and 4.4% in 1999 and 2000, respectively. However, with new room supply outpacing demand growth and predictions of a slowing economy in 2001, the market began to experience downward pressures on occupancies. According to Pannell Kerr Forster Consulting Inc. (�PKF�), the national occupancy declined from a high of 67.4% in 1998 to 65.0% in 2000, and from 66.1% year-to-date August 2000 to 65.3% for the same period in 2001. Yet, as late as August 2001, economists were optimistic that the second half of 2001 would show improved economic conditions, which in turn would enhance Canadian hotel operations. The tragic events of September 11th then occurred causing the North American economy to retract and uncertainty to reign. Owners and operators are now faced with the difficult task of understanding

the implications the events of the past few months and the current economic

climate will pose as budgets and strategic plans are developed and modified

for 2002. In light of this, Colliers International Hotels hosted the Hotel

Investment Forum in late November and early December 2001, which consisted

of a series of Town Hall meetings held in Vancouver, Calgary, Toronto and

Niagara Falls. Panels of hotel owners, operators, developers, consultants

and lenders provided their perspective on how the industry is coping and

how best to move forward in 2002. This document replaces our traditional

annual report which provided an analysis of historical and forecasted operating

and investment trends for the major Canadian hotel markets. In this report,

we have capsulized the pulse of the industry by supplementing key quantitative

trend data with the qualitative insight gleaned from the Hotel Investment

SETTING THE STAGE: Economic indicators for Q3 2001 confirmed the Canadian economy had contracted

for the first time since 1992, the result of declining exports and reduced

inventories. According to the Bank of Montreal, real GDP was predicted

to have further declined in Q4 by an

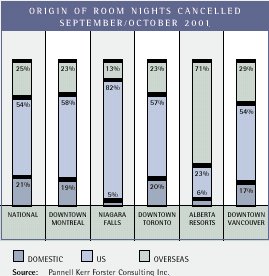

LOSS OF ROOM-NIGHT DEMAND DUE TO 9/11:

Of the 17 markets surveyed, approximately 75% of the impact took place in seven of the major centers, including Montreal Downtown, Ottawa, Toronto Downtown, Niagara Falls, Calgary, Alberta Resorts and Vancouver Downtown. Niagara Falls suffered the greatest number of room cancellations of pre-booked business in September and October, at 144,500 room-nights. Toronto Downtown lost approximately 104,200 room-nights, while the downtown markets of Montreal and Vancouver reported cancellations of 86,400 room-nights each, followed by Alberta Resorts with 66,100 room-nights lost. These room-nights effectively translate into occupancy losses ranging between 10.5 and 19 points for the markets noted above. DROP-OFF IN GROUP AND TOUR DEMAND: The decline in room-night demand cannot solely be attributed to 9/11, although these events certainly contributed to the softening of Canada�s lodging operating fundamentals. Consistent with general market trends, KPMG, Hospitality, Leisure & Tourism (�KPMG�) identified a drop-off in Group and Tour demand as early as Q2 2001. While the number of room-nights occupied in the Toronto Downtown market during September 2001 were approximately 35% lower than September 1999 and 40% lower than September 2000, the real story was the timing of the decline. The number of definite room-nights booked for Q3 2001, as of June 30th, 2001, was 20% or 13,513 room-nights less than at March 31, 2001. Anecdotal evidence suggests a similar pattern in Montreal, Vancouver and Calgary although the declines were not as pronounced. KPMG�s view is that although safety was an issue post 9/11 and resulted in a direct decline in both leisure and corporate travel, the timing of the decrease in group and tour demand speaks to receding economic conditions pre 9/11. THE IMPACT OF DECLINING DEMAND ON ROOM RATES: As discussed earlier, occupancy declined at a national level by 3.6%,

from its high of 67.4% in 1998 to 65.0% in 2000. Rates during this time

grew at a compound annual rate of 5.6%, from $99.59 to $111.14, resulting

in RevPAR growth of 3.7% (compounded annually). Occupancy further declined

as of year-to-date November 2001 by 3.7%, from 66.8% last year to 64.3%

while average room rates increased 2.7%, from $111.70 to $114.72 over the

same period. This moderate rate growth mitigated the decline in RevPAR

to only 1.2%, from $74.64 to $73.71. PKF reports that as of year-to-date

November 2001, the majority of Canada�s major markets had not experienced

rate declines, with the exception of GTA West, Calgary, Vancouver and Greater

Victoria, while occupancy had declined in virtually all major markets excluding

Edmonton, St John�s and Ottawa East. Although the effects of decreased

travel and reduced consumer confidence following 9/11 resulted in RevPAR

declines of 16.8% and 8.9% in the months of September and October compared

to the prior year, respectively, one cannot ignore the noticeable decline

in occupancy and slowing rate growth of the past three years.

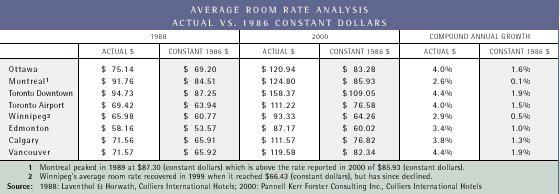

Colliers International Hotels Lessons learned from the recession of the early 1990s emphasize the

importance of maintaining average room rates in a softening lodging market

to facilitate a faster recovery. We surveyed eight Canadian markets, including

Ottawa, Montreal, Toronto Downtown, Toronto Airport, Winnipeg, Edmonton,

Calgary and Vancouver. In our analysis, we compared each market�s average

room rates (calculated in 1986 constant dollars) and found that rates reached

their highest point in 1988 and 1989 with the exception of Vancouver which

peaked in 1991. With the onset of the recession in the early 1990s, hotels

began discounting room rates. Our analysis shows that six of the eight

markets took between nine and eleven years before recovering to the same

levels experienced in the late 1980s. Vancouver, however, only took four

years to recover as the market experienced less severe rate discounting,

dropping only $6.00 (constant dollars) from its rate peak. In contrast,

Montreal, has not yet recovered as a result of rates declining by almost

$28.00 (constant dollars) from a high of $87.30 in 1989.

|

| NEW ROOM SUPPLY:

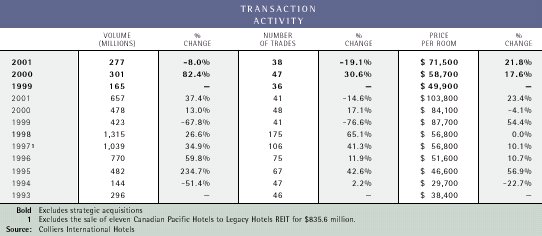

On the positive side, supply growth in Canada is decelerating. With declining occupancies and a difficult borrowing environment, a number of proposed hotel development projects have been cancelled or postponed as companies re-evaluate their expansion plans. Approximately 5,800 new rooms were built in 2001, representing a 26.1% decrease in construction activity over 2000, when an estimated 7,850 rooms were built. A further slowing of hotel development is occurring, with only 5,100 rooms currently under construction and anticipated to open in 2002. The majority of development activity has shifted to the central Canadian provinces of Ontario and Quebec which account for approximately 59% of activity in 2001 and 2002; this is in contrast to 1999 when over 60% of the new supply occurred in Western Canada. With respect to major markets, Ottawa will see the most growth (+14.0%), followed by Toronto Airport/West (+10.4%), Toronto North/ East (+9.8%) and Niagara Falls (+6.9%). Over one-third of the new supply has been built in a number of major suburban markets, where there is an abundance of land which has provided strong development opportunities. As these markets typically have older hotel supply, these newer properties are able to capture premiums in market share and higher rate penetrations. Approximately 26% of the new hotel supply is comprised of limited service product in secondary and tertiary markets such as Guelph, Ontario and Langley, British Columbia. Conversely, hotels developed in the urban markets are typically extended-stay, full-service or boutique. The addition of residential condominium units in major markets like Toronto, Montreal, Ottawa and Vancouver, which are marketed as corporate or extended stay apartments, have also impacted supply. These units are generally easier to develop, finance and operate, and are free from transient occupancy and related taxes collected from traditional hotels. This gives the �residential hotel units� a significant and unfair cost advantage over hotels. TRANSACTION ACTIVITY: The hotel investment market is strengthening, despite the mixed economic signals of the past year. Transaction activity increased by 37.4% over 2000 levels, with an estimated 41 hotels sold in 2001, at an aggregate volume of approximately $657 million. Similar to the previous two years, when strategic acquisitions represented 61% and 37% of total transaction volume, respectively, strategic buyers dominated the investment market in 2001. The acquisition of The Fairmont Empress in Victoria and the Fairmont Le Chateau Frontenac in Quebec City at a combined price of $305 million in February, together with the purchase of the 50% interest in the Sheraton Centre Toronto Hotel for $75 million in April, comprised approximately 58% of the total transaction volume. These trades resulted in the average price per room increasing 23.4%, from $84,100 in 2000 to $103,800. However, when these strategic trades are excluded, the average price per room still increased over last year by 21.8%, from $58,700 to $71,500 with much of the activity occurring in British Columbia, Ontario and Quebec. Approximately 75% of the 41 transactions were valued at $10 million or less, signifying this segment of the market as having the most liquidity. As well, looking at the profile of buyers, when the three strategic acquisitions are excluded, the majority of the transactions were completed by private investors and investment companies. Although investors took a deep breath following 9/11, there were eleven

hotel sales between September and December amounting to $92.5 million.

While this is below the $297.3 million of transaction volume reported for

the same period in 2000, it does surpass the $71.1 million reported in

the comparable period for 1999.

|

| CAP RATES:

Cap rates have been trending upwards for the past decade, increasing for a typical transaction from below five percent in 1992/1993, to between 10% and 12% from 1999 to 2001. In the early 1990s, low cap rates reflected the turn-around and repositioning upside of the hotels being acquired during a post recession environment. During the mid-1990s, as the industry recovered and prospered, cap rates rose in response to improving operating fundamentals and investor yield expectations. By early 1998, cap rates fell slightly in response to the market frenzy created by the REITs and public companies as they rushed to establish national presence. However, the shut down of capital markets for real estate financing in mid-1998 halted public com-pany expansion, and accompanied with substantial increases in the cost of borrowing and limited repositioning opportunities, cap rates rose to the 10% to 12% range. Uncertainty in the market following the events of September 11th and the general economic slowdown in North America, suggest cap rates for typical hotel transactions will continue to climb in the near term, to the 12% to 14% range, although strategic hotel trades will be significantly lower due to their prominent locations and high barriers to entry. Lower cap rates are likely on the horizon, but will be dependent on how quickly a property can return to 2000 income levels and will need to be assessed on a property-by-property basis. FINANCING: Debt financing continues to be limited with loan-to-value ratios remaining

in the 50% to 60% range. Relationship lending is expected to play a larger

role in financing in the near term. Due to the current unpredictable

and somewhat volatile cash flow period, conduit lenders who brought liquidity

to the market in recent years are likely to be more constrained as their

underwriting criteria is largely based on consistent cash flow. On a positive

note, we are seeing U.S. and European lenders finance large institutional

quality single assets or portfolios for sponsors with strong covenants.

OUTLOOK FOR 2002: Due to the lack of oversupply issues, less severe occupancy declines, and conservative lending practices, we do not anticipate seeing the same number of loan defaults compared to the United States. Lending institutions surveyed have not yet seen any technical default situations, attributing this to strong balance sheets and prudent expansion practices by hoteliers. To continue building healthy operating businesses and maintain low debt to equity levels, hotel owners and operators have made necessary changes to their day-to-day operations. Generally, these have included reducing labour costs and service levels to account for the temporary decrease in demand. In addition, some franchisors have loosened specific franchise guidelines to help franchisees better deal with the circumstances post 9/11. We anticipate that hoteliers will continue to focus on expense reductions until they see increased demand and an economic recovery which is expected by mid to late 2002. On the hotel investment side, there will be opportunities over the next

12 months, especially for counter-cyclical investors who are willing to

accept lower short-term cash flows. Market uncertainty will be priced into

transactions, with the dominant players in the near term being those with

substantial equity and debt sources. Any significant activity will be dependent

on the gap narrowing between bid and ask as owners realize that the peak

in hotel values was in 2000. Although we will continue to see clusters

of strategic acquisitions in 2002, most hotel investment will occur in

the less than $15 million range. We anticipate markets across Canada will

continue to show their resiliency, with either flattened or modest increases

in operating performance in 2002. While operational and marketing skills

are being tested at every level, there is a general sense of recovery by

Q3 and Q4 2002. There will be increased domestic travel and inbound travel

from Americans due to both security issues and the low Canadian dollar,

which should help improve occupancies and in turn lead to increased interest

in the hotel sector.

Colliers International

|

###

|

Colliers International Hotels Hotel Investment Advisory Services Bill Stone Alam Pirani Deborah Borotsik Stephanie Howell [email protected] One Queen Street East Suite 2200 Toronto, Ontario M5C 2Z2 Phone: (416) 777-2200 Fax: (416) 777-9232 http://www.colliers.com |