|

|

|

|

|

|

|

|

|

Quarterly Perspectives 2nd Quarter 2001 |

| Quarterly Perspectives is a strategic planning publication prepared by the industry analysts and market specialists at Lodging Econometrics and National Hotel Realty. |

| 2001: A Mid-Year Forecast

Revision

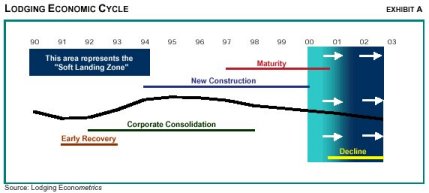

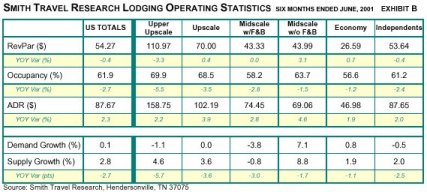

It was not the smooth descent from the top of the Lodging Growth Cycle that we hoped for, but a sharp, precipitous fall that caught nearly all by surprise and is still gathering steam. The underlying assumption in Lodging Econometrics� (LE�s) original forecast for 2001 was that the broader economy would start to recover in late 2001 and the lodging industry would follow suit six to nine months later. This would be followed by a slow, incremental recovery of at least two years in duration. While this recovery profile is proving correct, there are two new variables: the initial economic declines are deeper than expected and we have fallen at least six months, maybe even longer, behind the start of the scheduled lodging recovery. (See Exhibit A) As unit management teams and home office staffs revise second half pro formas and begin the budgetary process for next year, they enter the planning cycle with more uncertainty about macro economic forces at play than at any other time since the early �90s. Year-to-Date Operating Results 2000 was the peak year in the lodging cycle. According to Smith Travel Research, nationwide occupancy finished at 63.5%, ADR at $85.24, and RevPAR at $54.13. Importantly, year over year demand growth was 3.7%, compared to declining supply growth at 3.1%, a favorable variance of 0.6 percentage points.

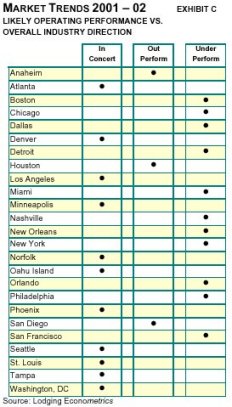

It was the first favorable variance in four years, and at the time, was thought to be a harbinger of positive things to come. Industry-wide occupancy declines were first noticeable in mid-January of this year and have been falling steadily. Through June, occupancy is down 2.7%, compared to the same period last year. ADR is up 2.3%, making for a decline in RevPAR of 0.4%. (See Exhibit B) Occupancy declines have occurred across all Chain Scales, but are the heaviest in the Upper Upscale and Upscale segments, down 5.5% and 3.5%, respectively. Room rates are still holding but at a lower growth rate than last year, as is typical for the early months of a downturn. Year over year occupancies have fallen in 20 of the Top 25 Largest Markets. Declines are deepest in gateway cities like Boston, New York, Chicago, San Francisco, and Dallas. Corporate layoffs and restrictive travel policy changes have caused serious declines in high-rated transient and meeting business. Companies are trading down to lower-rated, Mid-Market hotels as part of savage cost-cutting programs. Corporate meetings have been cancelled and attendance figures are down across the board. The strong dollar has produced declines in international visitors as well.

Most lodging companies entered the slowdown with a variety of programs and promotions geared to maintaining RevPAR premiums and operating margins. To bolster revenues, room rates were increased. The ubiquitous energy surcharge, now being widely challenged in class action suits, was a popular strategy to offset rising energy costs, and by June was being applied in 21 states. Cross training to increase employee efficiency, a mix of layoffs and a variety of other cost control measures were important strategies. These efficiencies have worked through the units and, by now, corporate P & L�s and most opportunities are captured. A major problem looms ahead that will put additional downward pressure on lodging profits in �01 and �02�room rates. As occupancies continue to decline, hotels must compete more aggressively for business on the basis of price. It is now a buyer�s market. This summer and fall, domestic and international tourists, happy to just find a room last year, are now shoppers in a new, more competitive price environment. Many hotels have already won new transient, meeting and tour accounts at rates lower than they would have considered just a year ago. Room rates for contracted corporate transient and meeting accounts will be coming up for renewal this fall and are likely to be negotiated lower. These lower rates will soon be reflected in monthly operating statistics. As the downturn continues, the pressure to lower rates will greatly increase, and, combined with already declining occupancies, there will be a "double whammy" effect on both RevPAR and Profitability. Forecasting Corporate Demand To determine when lodging demand growth ceases to decline, how long it remains in a bottoming pattern and when a recovery commences, one needs first to access broader economic fundamentals. GDP growth is the key variable. After considering a 3-month lag, it plots near perfectly with occupancy. GDP growth, made up of about one-third corporate and two-thirds consumer inputs, is expected to receive a boost from recent Fed rate reductions: six adjustments downward, amounting to 2 3/4 points over six months � the most concentrated Fed activity in nearly twenty years. The hoped-for outcomes are:

In the last three years of the 1990s, capital investment ran at twice the normal pace. As a result, excess capacity in American industry is at the highest level since 1983. No matter how low interest rates are, it is hard to imagine seeing any step-up in capital spending in the foreseeable future. The record inventory overhang from last year is taking longer than anticipated to work down. It will be well into the fall before any appreciable uptrend in manufacturing is seen. Unemployment, which bottomed at 3.9% in �00, is now up to 4.5% in June, still the best labor market in thirty years. But there are further declines ahead as already announced layoffs work through the system and perhaps another round of layoffs follows. Some economists feel that unemployment, a lagging economic indicator, could peak over 5%. The airline industry is also telling for the lodging industry, as passenger traffic counts closely parallel occupancy. In May, traffic fell simultaneously in both the U.S. and Europe for the first time in a decade. Forecasting Consumer Demand Consumers account for two-thirds of GDP growth. Last fall, the torch was officially passed to the consumer to carry the economy until the corporate community could sufficiently recover. But success appears problematic at best as the consumer is looking more weary. Big ticket consumer purchases�autos, housing, and retail sales�were surprisingly strong in the first half�particularly in the face of declining consumer confidence, growing layoffs, falling net worth, and increased debt loads, but the tide could change. Declining interest rates tripled the pace of residential refinancing this spring, but proceeds seem to have been used for consumption rather than debt reduction. Credit card debt is at a record high. Delinquency rates and defaults are growing and are near levels reminiscent of the early �90s. To date, standards of living have been maintained by loading up on debt, but the consumer now appears maxed out. On the other hand, a new wave of dollars for the consumer is about to arrive. Lower interest rates mean that debt servicing costs will decline and that residential refinancings will continue, albeit at a slower pace. Energy costs declined just in time for the summer tourist season and the tax rebate checks are "in the mail." A summertime rally in the Dow, stimulated by lower rates, if it occurs, could encourage consumers. Lodging observers are hoping this stimulus will maintain levels of consumer spending through early 4Q01, making for an acceptable, not great, summer and fall tourist season. Forecasting Supply Growth For LE�s Soft Landing scenario, the forecast for new supply was a 2.6% to 2.7% growth rate for 2001 and a decline below 2.5% in 2002. Supply additions were expected to be heaviest in many of the major urban centers, a typical pattern late in every real estate development cycle, as larger full service properties seeded long ago come on line. Tightening credit conditions and a slowing economy would cause both cancellation rates to be high and the volume of new project announcements to decline. At the end of 2000, 21 markets of the top 25 had occupancies in excess of 63.5%, the industry average. These were the targeted markets of great opportunity for developers. The markets were very strong and were expected to absorb new supply growth of between 3% and 5% in 2001 and 2002 even in the face of moderate declines in occupancy. Accounting for the Top 25 Markets is important because they play a disproportionate role in industry-wide operating statistics, revenue and profitability. Just as they overemphasize the industry�s success during business expansions, so do they exaggerate downward trends during periods of decline. These markets contain 32% of the nation�s guestrooms, but generate 43% of the industry�s revenue and perhaps more in profits. In 1H01, occupancies in the top markets did not decline moderately, as anticipated, but precipitously, much deeper and faster than any of the forecasting models anticipated. Results for six months year-to-date are revealing:

Decreasing interest rates have changed the expectations of developers in two contrasting ways. In the first instance, a significant number of projects moved forward from Early Planning into In Permitting, as developers who feel they have attractive projects rushed to get underway before the economy worsens or the already very difficult financing terms and conditions tighten further. LE expects there will be more project delays and considerable hesitancy about go/no go decisions as the industry continues to soften more deeply and for a more prolonged period. As a consequence, LE is expecting project delays and a high number of cancellations for hotels In Permitting. On the other hand, there has been a significant rise in cancellations as other developers, increasingly concerned with declining business conditions and fears of recession, have already pulled projects from the Pipeline. Over the next two quarters, further project cancellations and a slowing

pace of new additions to the Pipeline will help identify when supply could

A Changing Set of Assumptions With each passing day, it is becoming less likely that an economic recovery will begin this year. In fact, some tech companies are now forecasting 3Q02 as their most likely turnaround date. That is ominous and has serious ramifications for the broader economy and the lodging industry as well. The slowdown is like none other in memory. Usually, slowdowns are initiated by consumers who stop spending when the Fed increases rates. That, in turn, decreases productivity, reduces capital investment and leads to layoffs. This time business started the downturn. A glut of produced goods caused a slowdown in investment, which was running as high as 13% per year in the late �90s. This excess inventory and capacity in manufacturing led to the layoffs, but fortunately from high rates of employment. The "inverted" slowdown is a new experience for lodging industry analysts, economists and for the Fed as well. Everyone is waiting to see if the Fed�s traditional remedies will work as in the past. LE�s thesis, moving forward, is that the consumer cannot continue to take on debt and spend at rates in excess of income. With a growing flow of layoffs, confidence will fall and spending will decline. Tax rebates, some of which will go to debt retirement or into savings, will boost consumer spending, but not a lot and certainly not beyond the fall. The corporate world is prepared. Revenues and earnings are falling. It doesn�t seem likely that corporate growth will pick up before the first or second quarter next year. Ominously that may lead to a time gap�late this year through early summer

next year�where consumer spending could stall before business is capable

of assuming economic leadership. Such a gap could mean further economic

declines ahead, a more prolonged bottoming and a milder recovery for lodging.

New supply openings will drift to and below 2.5%, but will average closer to 3.5% in many of the Top 25 Markets in �01 and closer to 3.0% in �02. For existing property owners, conditions will feel as if there were a supply problem, when an unanticipated dramatic decline in demand is the real problem. Demand/Supply imbalances in major markets will negatively exaggerate industry-wide operating statistics. We are in for two years of declining profits, fortunately from record-high levels, before bottoming out. The enclosed research information is intellectual property,

is copyrighted and remains the property of Lodging Econometrics with all

rights reserved. The nature of our relationship is that of a site licensee

with specific rights granted for the use of the research solely by the

subscribing client. Specifically, there are no republication or electronic

transmission storage rights granted, nor can the research be duplicated

or transmitted electronically outside the organization nor can it be shared

with or disclosed to other hotels, companies, developers, investors, franchisees,

joint venture partners, lenders, vendors or other parties, without the

expressed written consent of Lodging Econometrics.

Quarterly Perspectives is a strategic planning publication prepared by the industry analysts and market specialists at Lodging Econometrics and National Hotel Realty.

Quarterly Perspectives is published by Lodging Econometrics four times annually.

|

Patrick H. Ford, Publisher (603) 431-8740 ext. 13 [email protected] |